Fintechs are setting the pace for retail and digital experiences while traditional banks trail, constrained by rigid operating structures and slower innovation cycles.

According to KPMG West Africa Banking Industry Customer Experience Surveys from 2023 to 2025, the shift emerged prominently in 2023 during the naira redesign-induced cash crunch, which highlighted weaknesses in traditional infrastructure and drove users to digital options.

That year, fintechs stood out on Integrity and Time & Effort pillars, led by Opay (81.2), PiggyVest (80.0), Moniepoint (79.5), PalmPay (79.3), and Kuda MFB (78.9).

Customers appreciated low fees, dependable digital services, and easy onboarding, though fintechs needed improvements in security and issue resolution.

Read also:┬ĀTraditional banks trail as fintechs set new customer experience benchmarks

In 2024, fintechs strengthened their position with higher ratings, outperforming traditional banks in the customer journey, especially retail stages.

PiggyVest and Opay tied at 82.0, followed by PalmPay (81.6), Kuda (80.6), and Moniepoint (80.2).

The report emphasized fintechsŌĆÖ contribution to inclusion, including streamlined loans (26 percent of successful applications) and added services like insurance and investments.

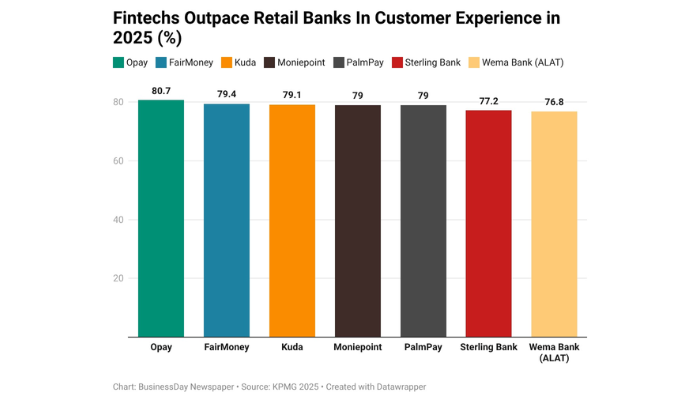

The 2025 survey confirms the pattern as fintechs lead in Time & Effort (low-friction interactions) and Expectations (reliable uptime), raising benchmarks that traditional banks find hard to meet in mass retail.┬Ā Traditional banks made modest progress but face legacy constraints.

In 2024 retail rankings, Stanbic IBTC topped at 75.5, yet the segment lagged overall. SME banking grew fastest, with Stanbic IBTC leading, while corporate achieved the highest scores: GTBank at 82.5, followed by Zenith and Access (tied at 82.2), thanks to strong relationship management, personalisation, and proactive support.

Persistent industry weaknesses include Resolution (lowest pillar for five years) and Personalisation, with complaints about delayed resolutions and generic services.

The five to seven point gap in retail/digital experiences signals a key change: Tech-savvy Nigerians now judge providers by fintech-like agility and innovation, not just physical branches.

The 2023 cash crunch sparked the shift, but fintechsŌĆÖ mobile-first design, real-time tools, and trust features have deepened their role in everyday finance.

Fintechs grapple with fraud concerns, privacy issues, and marketing practices, yet they reshape the market.

As the 2025 KPMG report states, competition goes beyond the basics, adding that in open banking, recapitalisation, and AI eras, winners will provide seamless, proactive experiences.

The report however advised that legacy banks must adopt fintech standards or face losing loyalty in NigeriaŌĆÖs mobile-first future.

┬Ā