Dangote Cement Nigeria has produced more income from the use of assets than peers as industry capacity utilization remains low due to slow economic growth.

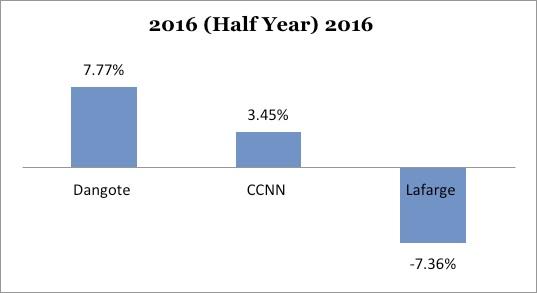

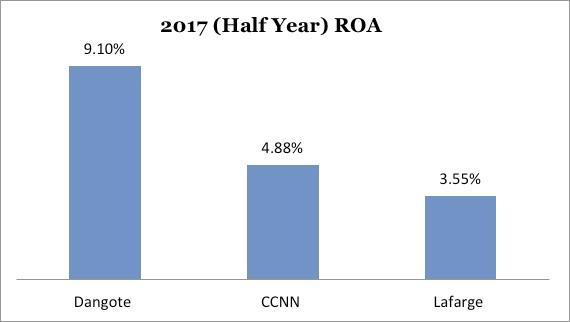

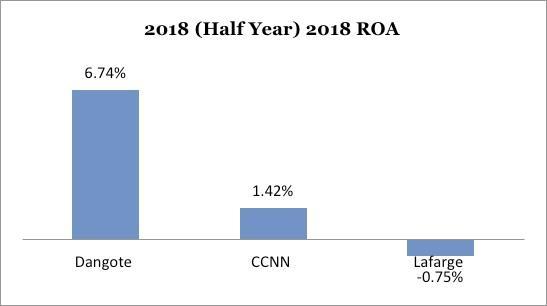

For every Naira of assets the largest producer of the building material invests in, it returns 7.0 percent or N.070 in net profit for the year, that compares with Lafarge Africa, (1.60 percent or N.016), and Cement Company of Northern Nigeria (CCNN), 2.06 percent or N0.0206.

The return on assets ratio (ROA), often called the return on total assets, is a profitability ratio that measures the net income produced by total assets during a period by comparing net income to the average total assets.

It is calculated as net income divided by total asset. A higher ratio shows a company has put its resources to work in generating profit, and shareholders crave a corporation that deliver a higher return on investment in form of bumper dividend and share appreciation.

Dangote is better at converting its investment into profits, compared with Lafarge’s and CCNN. One of management’s most important jobs is to make wise choices in allocating its resources, and it appears Dangote management is more adept than its two peers.

While industry’s ROA increased to 3.58 percent in June 2019 from 2.47 percent the previous year, it is lower than an all-time record of 9.12 percent recorded in 2015, when inflation rate was low and crude oil price, favourable.

Cement companies in Africa’s largest economy are yet to recover from the 2016 recession that paralyzed economic activities and slowed down construction activities.

Between 2004-2014, cement sector expanded at a robust Compound Annual Growth rate (CAGR) of 13.70 percent, however, growth has averaged -1.0 percent, in the past three years with only marginal recovery in growth of 4.50 percent in 2018.

While the dominant players in the industry spent more in the acquisition of property plant and equipment in the period under review, their capital utilizations are low.

Adebayo Bakare, Industrial Goods analyst at Afrinvest Securities Limited said that industry volumes are weak due to poor economic conditions in the private and public sectors. He also added that prices have also increased more than 40 percent since 2016, and that has pressured demand.

The cumulative acquisition of property, plant and equipment of Dangote, Lafarge, and CCNN hit a four year high of N85.12 billion as at June 2019, but the figure is 5.01 percent of combined property plant and equipment (PPE) balance of N1.82 trillion in the balance sheet. This means that the acquisition of PPE by these companies is immaterial.

A breakdown of the figures shows Dangote Cement’s capital expenditure spend stood at N74.10 billion in the period under review, which is 6.02 percent of N1.18 trillion PPE balance.

Lafarge Africa spent N7.89 billion on the acquisition of asset, which is 1.89 percent of total PPE balance of N417.19 billion.

CCCN, which recorded the fastest expansion in capex spend among peers, expended N6.17 billion on the acquisition of asset, an amount that is 3.02 percent of the PPE balance of N222.75 billion.

Onyeka Ijeoma research analyst –at Vetiva Capital Management is of the opinion that companies do not invest in new plants every year and that they still have to maintain the capacity that they have.

Yinka, Yinka Ademuwagun, equity research analyst with United Capital Limited said the jump in CCNN’s capex spend was largely driven by mergers and acquisitions activities, and he added that Dangote Cement invested in distribution assets this year.

“Dangote upgraded some their fleets but this will not be sustained,” said Ademuwagun.

CCNN, the only cement company in the North West, has total assets was N358.47 billion as at June 2019, this compares with N20.03 billion in 2016.

CCNN has an installed capacity of 2.0 million metric tonnes after entering a merger with Kalambaina cement (owned by BUA).

BALA AUGIE