Data by the International Monetary Fund (IMF) show that the correlation between average real GDP per capita and mobile penetration is positive in Africa. Similarly, the correlation between financial inclusion and mobile penetration is positive.

This suggests that the rollouts of Information and Communications Technology (ICT) could stimulate economic growth and financial inclusion.

“The results confirm that ICT, including mobile phone development, contribute significantly to economic growth in African countries. Part of the positive effect of mobile phone penetration on growth comes from greater financial inclusion,” IMF said.

Nigeria’s quest to give financial access to 80 percent of its citizens has been largely driven by its bank-led financial inclusion model, but the largest economy in Africa has lagged its Africa peers who adopted the use of technology. Hence, the question of whether the country can reduce its high exclusion population without the Telcos.

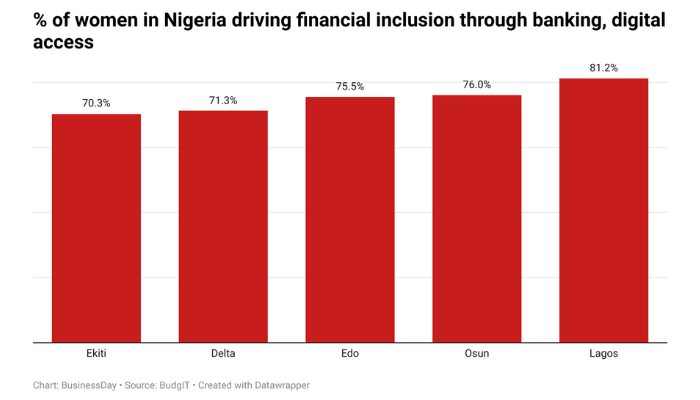

Most recent data by EFInA put Nigeria’s financial inclusion rate at 63.2 percent, meaning that as much as 36.8 percent adults still lack access to financial services.

As at the time Nigeria was considering the optimal approach needed to leverage new, innovative technology to deliver financial services to its people, the Central Bank analysed in some detail how to structure the guidelines and the regulatory environment to deliver the benefits on offer, without compromising the integrity of the financial system.

According to the World Bank’s 2017 Global Findex database, mobile money drove financial inclusion in Sub-Saharan Africa. The report stated that between 2014 and 2017, there was a significant increase in the use of mobile phones and the Internet to conduct financial transactions which contributed to a rise in the share of account owners sending or receiving payments digitally from 67 percent to 76 percent globally, while developing countries recorded 57 percent to 70 percent.

“Fulfilling the financial infrastructure gap in Africa, by using branchless banking services such as mobile financial services, is seen as a promising way to increase financial inclusion,” the International lender of last resort said.

On the reason for the aforementioned, the Washington-based Fund said it is because mobile telephony allows expansion and access to financial services to previously underserved groups in developing countries.

“It reduces transaction costs, especially the costs of running physical bank branches. The increasing use of mobile telephony in developing countries has contributed to the emergence of branchless banking services, thereby improving financial inclusion,” Peter Allum, a division chief at IMF said.

In the quest to achieve a 20 percent exclusion rate by 2020, the central bank on the 5th of October 2018 released an exposure draft guideline in which it proposed Payment Service Banks (PSB) aimed at deepening financial inclusion.

Since inviting Telcos and other industry players to apply for the mobile money licence over a year ago, the industry regulator has only granted Approval-In-Principle (AIP) to Hope, Money Master, and 9PSB to operate as payment service banks.

“Nigeria has a large mobile market, and the huge number provides an opportunity to use it in deploying easy-to-use technology that can improve access to financial services,” Oghogho Osula, financial expert and former MD/CEO of Coronation Trustees Limited said.

Data by Nigerian Communications Commission (NCC) analysed by BusinessDay revealed that the total number of subscribers per individual telecoms operator as of August 2019 stood at 176.89million.

Endurance Okafor