Nigeria’s biggest banks are feeling the pains of a dovish monetary environment as interest incomes move at a snail’s pace despite an increase in volume of loans from customers.

Interest income stems from the yields generated from lending to customers. Therefore, if there is an increase in loans given to customers, especially performing loans, it translates to an increase in interest income.

BusinessDay analysis shows the loans to customers of Nigeria’s biggest banks increased by 7.77 percent to N13.76 trillion in the first quarter of 2022 (Q1 2022) from N12.77 trillion in the first quarter of 2021 (Q1 2021).

However, the interest income has only increased by 8.61 percent in Q1 2022 to N534.60 billion from N492.23 billion in Q1 2021.

“When you factor in the impact of a dovish stance whereby interest rates are low or reduced, the loans to customers do not necessarily translate to an increase in interest income considering the fact that they are faced with subdued yields,” said Sesan Adeyeye at CSL Stockbrokers Limited, a subsidiary of FCMB Group Plc.

“However, looking at what has happened in the past two years, whereby yields have been low, just to cushion the impact on the economy, we saw that interest income was still subdued despite the increase in loans to customers, “added Adeyeye.

The biggest Nigerian banks are the tier one banks with the acronym FUGAZ which include First Bank of Nigeria, United Bank for Africa (UBA) Plc, Guaranty Trust Holdings Company (GTCO) Plc, Access Bank Plc, Zenith Bank Plc,

Loans to customers and interest income for these banks have grown in 2018 by 59.37 percent from N8.64 trillion and by 8.15 percent from N494.31 billion respectively.

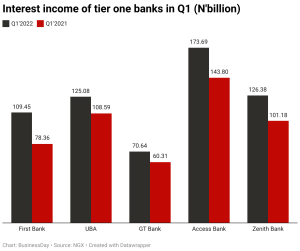

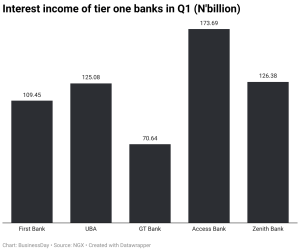

First Bank of Nigeria in Q1 2022 recorded an increase in its interest income by 39.6 percent to N109.45 billion from 78.4 billion in the same period last year.

Its loans to customers surged 32 percent to N3.05 trillion in Q1 2022 from N2.30 trillion in Q1 2021. The bank also recorded a profit after tax of N32.4 billion, a huge 107 percent increase from N15.6 billion last year.

UBA in Q1 2022 recorded an increase in interest income by 15 percent to N125.07 billion from N108.59 billion in the same period last year. Its loan to customers increased by 5 percent to N2.87 trillion in Q1 2022 from N2.73 trillion in Q1 2021. The Pan- African bank also recorded a profit after tax of N41.5 billion, an increase of 8.7 percent from N38.15 billion last year.

Likewise, GTCO in Q1 2022 recorded an increase in interest income by 17 percent to N70.64 billion from N60.3 billion in the same period last year. Its loan to customers increased by 4.8 percent to N1.72 trillion in Q1 2022 from N1.64 trillion in Q1 2021. The bank also recorded a profit after tax of N43.2 billion, a 5 percent decrease from N45.5 billion last year.

Read also: Bank stocks jump after CBN rate hike

Access Bank also recorded an increase in interest income by 20 percent to N173.7 billion from N143.8 billion in the comparable periods. Its loan to customers surged 31 percent to N4.28 trillion in Q1 2022 from N3.25 trillion in Q1 2021. The bank recorded a profit after tax of N57.4 billion, an increase of 9 percent from N52.5 billion last year.

Zenith Bank in Q1 2022 recorded an increase in interest income by 24.91 percent to N126.38 billion from N101.18 billion in the same period last year. Its loan to customers surged 25.03 percent to N3.55 trillion in Q1 2022 from N2.84 trillion in Q1 2021. The bank also recorded a profit after tax of N58.20 billion, an increase of 9.68 percent from N53.06 billion in the same period last year.

According to Adeyeye, the growth seen in the financials of both tier one and tier two banks in 2021 and 2022 was spurred by non-interest income, while the growth in the interest income was subdued majorly due to the low-interest environment.

In September 2020, the Central Bank of Nigeria reduced the Monetary Policy Rate (MPR) from 12.5 percent to 11.5 percent in order to provide cheaper credit to improve aggregate demand, stimulate production, reduce unemployment, and support the recovery of output growth.

The reduction was part of measures to mitigate the negative impact of the COVID-19 pandemic on the Nigerian economy. One major impact of the intervention was on the management of Non-Performing Loan (NPL) in the banking system.

Further diggings by BusinessDay showed that all the tier 1 banks, excluding Access Bank, recorded a decline in interest income in the first quarter of 2021 compared to that of the same period in 2020, despite the increase in loans to customers in the same period.

First Bank and UBA recorded a decline in interest loans in Q1 2021 by 25 percent and 0.47 percent respectively from N104.91 billion and N109.1 billion in the same quarter of 2020 respectively.

Likewise, GTCo and Zenith Bank recorded a decline in interest loans by 21.7 percent and 11.5 percent respectively, from N77.04 billion and N114.3 billion in the same quarter of the preceding year, respectively.

However, Access Bank recorded an increase in non-interest loans by 9.04 percent from N131.87 billion in the same quarter of the preceding year.

Johnson Chukwu, CEO, Cowry Asset Management said, “When the interest rates increase, the bank earns more from its lending activities, thereby its interest income will also increase. That means the bank is charging a higher interest rate on the loans and therefore earning more interest income.”

Recently, the CBN hiked the base rate for lending by 150 basis points to 13 percent, effectively raising the cost of borrowing within the country.

With the motive to combat accelerating inflation, the yield on government securities, which banks hold a good chunk of, is expected to rise, increasing their profitability and boosting investor sentiment towards their stocks.

“Banks are in the money with this decision,” said Omotola Abimbola, an analyst at Lagos-based investment bank, Chapel Hill Denham. “Their stocks are expected to rise as the CBN looks set to begin the process of interest rate normalisation.”

Banks have seen a subdued financial performance since last year due to the low interest rate environment, which curbed their profitability. That has dampened investor sentiment towards bank stocks, causing them to underperform the market.

While Nigerian stocks have emerged as the best performers in Africa this year with a return of 24 percent since the beginning of 2022, bankstocks have only managed a 6.17 percent return in the same period, nearly four times less than the average return of the market.

However, Gbolahan Ologunro, an economist at Lagos-based Cordros, believes the impact of the hike, which could either be positive or negative, wouldn’t be instantaneous. “I don’t think the impact would be instantaneous, but in the short run, probably from the third quarter to fourth quarter, when new loans would have been created.”

According to Ologunro, the impact on interest income depends on the application of loans, as the hike could lead to a decrease in the demand for loans by customers.

“On the surface, it is positive. But it then depends on what happens on the demand side. If the demand side weakens significantly, we may not really see a material impact on their interest income in subsequent quarters,” Ologunro said.