In a busy neighbourhood in Kano, Musa carefully slips ₦500 into an old envelope and hides it beneath his mattress. He knows about fintech; he has seen Opay and PalmPay around and even watched his neighbour use Kuda to settle a bill, but for him, saving still feels more secure when he can see and touch the money.

He is not alone.

In Enugu, Adaobi runs a small salon where most transactions are still cash-based. She has Moniepoint and PalmPay on her phone after her younger cousin persuaded her to try them. She occasionally checks balances or receives transfers, yet her handwritten notebook remains her most trusted financial record. For many like her, confidence in digital banking is still building, one cautious step at a time.

Their stories reflect a broader reality: fintech is growing, but tradition still holds sway. Many Nigerians are aware of digital finance, but awareness is not the same as adoption. For Musa and Adaobi, the shift is not just about technology; it is about trust, habit, and the comfort of what is familiar.

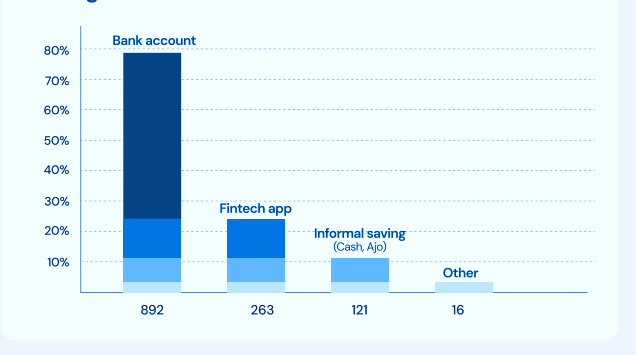

According to the 2025 Nigeria Financial Habits Survey by Column Content, 79.3% of Nigerians still trust traditional banks for saving, while 23.4% use fintech apps, and 10.8% rely on informal methods, such as cash at home or local savings groups. This mix reveals a deeper truth: digital finance is rising, but trust is still assumed, not earned.

Digital tools are expanding rapidly, but their reach remains uneven. Many Nigerians use fintech and banking apps to store money, yet only a few rely on them for real financial planning or budgeting. The gap is evident: people want more than digital wallets. They want solutions that help them save automatically, manage expenses with ease, and view their finances in one simple place.

This is where the next phase of financial innovation must turn its focus, not just on speed or but on building genuine trust through clarity, consistency, and usefulness. In a country where every naira matters, the real promise of finance lies in helping people see, plan, and act with confidence.

A significant development is emerging in Nigeria’s financial landscape. Mobile-first platforms like Opay, PalmPay, Kuda, and Moniepoint, once seen just as payment tools, are now vital to daily life. Opay now accounts for over 63 percent of usage, indicating that Nigerians are no longer just after convenience. They seek control, transparency, and reassurance in managing their money.

In a country where inflation cuts into earnings and income stays unpredictable, saving, even small amounts, has become an act of resilience. Most people save for emergencies or goals but still rely on memory or handwritten notes to track spending. Fintech companies are filling this gap with automation, transparency, and unified tools that mirror everyday realities.

These platforms are not replacing traditional banks; they are reimagining them for a generation that lives on mobile, values data, and seeks simplicity. Nigerians want to see their money clearly, plan with it easily, and trust the system that holds it.

As digital wallets replace paper ledgers and budgeting apps take the place of notebooks, a new kind of confidence is emerging. It is based on reliability, convenience, and the quiet certainty that technology can be both fast and dependable. One key question remains: can technology truly rebuild the trust that tradition once held, or is it quietly creating a new kind of financial belief?

The Transparency Test: Building Digital Credibility

In Nigeria’s fintech space, transparency has become the new measure of trust. The early promise of digital banking was speed and convenience, but credibility and clarity now define success. Platforms such as Opay, Kuda, Moniepoint, FairMoney, and Carbon are reshaping expectations, proving that trust grows not from branding but from consistent, verifiable experiences.

Kuda has turned fee transparency into an advantage through real-time alerts and clear charges that reassure users wary of hidden fees. Moniepoint’s agent network has built trust from the ground up, with each agent acting as a local anchor where banks are scarce. FairMoney offers instant credit scoring, while Carbon provides full transaction visibility, allowing users to control every naira they spend.

This shift is driven by cultural and regulatory changes. The Central Bank of Nigeria and the NDIC (Nigeria Deposit Insurance Corporation) are enhancing disclosure and audit standards, while new data ethics frameworks push fintechs to be clearer about how they handle user data. For consumers, this means moving from blind trust to informed trust, where confidence relies on evidence rather than promises.

Today’s digital audit trails, real-time receipts, and user-controlled data sharing form a new ledger of trust. Fintechs that make visibility and fairness central to their design are setting new standards. In a market where many Nigerians want to view all their financial activities in one place, transparency has become the base on which digital confidence is built.

Cracks in the Code: The Challenges of Digital Trust

Despite the shine of Nigeria’s fintech boom, cracks are beginning to show. As digital wallets, savings apps, and payment platforms grow, concerns about safety and security persist. The 2025 Nigeria Financial Habits Survey reveals a paradox: while 79 percent of Nigerians still save through banks, over 60 percent use fintech apps like Opay and Kuda for daily transactions. However, confidence in these platforms remains fragile.

Rising fraud and data breaches have weakened public trust. Reports of fake loan apps, phishing attacks, and unauthorised debits highlight a widening gap between innovation and integrity. Regulators are struggling to keep pace, as the speed of innovation outstrips the pace of oversight. New frameworks such as open banking and data protection policies have helped but often focus more on compliance than consumer protection.

Digital inequality deepens the challenge. Only a small fraction of Nigerians use budgeting apps, and many do not track expenses at all. This lack of financial literacy leaves users vulnerable. Experts warn that fintech’s next phase depends less on technology and more on sound governance. To stay credible, digital banks must balance speed with accountability and make user education part of their design. Nigeria’s fintech growth cannot only be about access; it must also secure trust.

Beyond the Interface: Banking on Trust

Nigeria’s digital finance revolution is entering a new phase. The age of convenience is giving way to credibility, where trust, not technology, will decide who leads the next chapter of banking. As mobile apps evolve into full ecosystems, a new benchmark is taking shape built on transparency, protection, and empowerment.

According to the CBN Governor, “Like an orchestra, our fintech ecosystem requires harmony between innovators and regulators, between inclusion and security, and between competition and collaboration. Only through such balance can we orchestrate a future that advances innovation, strengthens trust, and enhances financial inclusion.”

By 2030, competition in Nigeria’s fintech space will no longer be about faster transactions but about who Nigerians trust with their data and savings. The next generation of leaders will be those who turn innovation into inclusion and adoption into accountability.

In this future, banks will not only process payments but build partnerships. Credit will reach informal markets, sustainable finance will drive inclusion, and payments will move seamlessly across Africa’s trade corridors. Progress will not be measured by downloads or transaction volumes but by the restoration of digital trust. That will be the real revolution beyond the interface and the foundation of Nigeria’s next financial transformation