The men with two of the world’s toughest jobs are reaping different fruits from far-reaching reforms implemented since they took on the reins of Nigeria and Argentina.

Argentina’s reforms, anchored in economic prudence and fiscal discipline, seem to be yielding the desired outcomes, while Nigeria’s trajectory paints a contrasting picture.

Bola Tinubu, Nigeria’s president, and Javier Milei of Argentina embarked on some market reforms last year that were geared towards revamping their economies, but while the Milei-led government has put prices in check, his counterpart’s policies are yet to turn the corner for Nigeria.

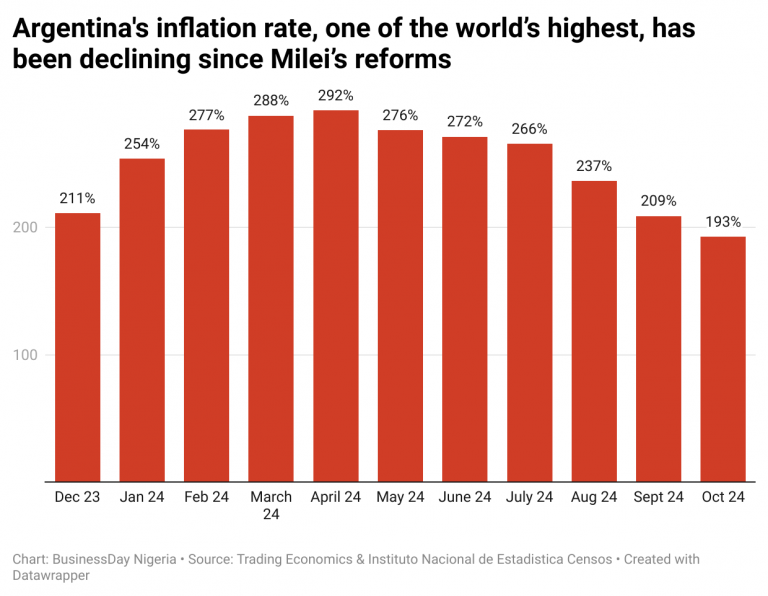

Milei, the libertan president of Argentina and an economist, faced with inflation exceeding over 200 percent, has curbed rising prices from a month-on-month figure of 25.5 percent when he took office last December to 2.7 percent in October. The lowest it has been since 2021.

The 54-year-old has fulfilled his campaign pledge to “take a chainsaw to the state,” as he cuts government departments in half to nine, downsized the public payroll and moved to eliminate private jets and other official perks while selling hundreds of state companies, making the country’s budget turned surplus after suffering many deficits.

While controversial, these steps quickly reined in inflation and restored a measure of market confidence. “We needed shock therapy,” Milei told international observers, emphasizing the urgency of restoring fiscal discipline.

“In a bold departure from Argentina’s long history of fiscal excesses, our primary policy is the pursuit of a balanced budget. Our financing needs, aside from rollover, will be nil,” Milei said in an interview with The Economist.

The quick reduction in public spending has helped the country of 46 million people swing from a fiscal deficit – the difference between the government’s spending and income – of 2 trillion pesos ($120 billion) last December to a surplus of 264.9 billion pesos as at April this year.

Argentina also reported a surplus in January, February and March, marking the first time it had achieved this monthly target since 2012.

From Buenos Aires, the capital, Mariana López, a small-business owner, said that while the reforms were initially painful, they created stability. “I no longer lose profits to unexpected currency crashes,” she said.

Market confidence in Argentina has soared under Milei, with the country’s sovereign dollar bond prices roughly tripling over the past 12 months.

Argentina’s country risk — the interest premium over US Treasuries which investors demand to hold the country’s debt — has fallen from more than 2,500 basis points this time last year to about 1,100, although it remains well above levels that would allow a return to bond markets.

Milei’s focus on a clear, albeit painful, economic strategy brought a sense of predictability to markets—something Nigeria desperately lacks.

Nigeria’s reforms: A case of half measures

Nigeria’s market reforms under President Bola Tinubu included removing fuel subsidies and floating the naira. However, the execution has left much to be desired.

These reforms, while theoretically sound and backed by international observers, lacked a coherent framework for managing their immediate fallout.

Inflation, the “dreaded monster”, rather than taking a back seat, soared, reaching 33.88 percent in October, eroding purchasing power and plunging millions further into poverty.

For Bolanle Adeoye, a civil servant in Lagos, the reforms have been devastating. “Everything is more expensive—transport, food, school fees. There’s no relief,” she said.

Unlike Argentina, where immediate compensatory measures such as social safety nets accompanied the reforms, Nigeria’s policy rollouts have been abrupt, with little cushioning for the most vulnerable.

Argentina and Nigeria: A tale of mounting debt

Milei inherited a debt legacy of about 60 percent to the country’s gross domestic product (GDP). The second largest South American economy is by far the largest debtor to the IMF.

One of the richest countries in the 19th century is equally troubled with external financial pressures as it has a $14 billion debt repayment due next year and may not be able to access credit until the peso currency is stronger.

But Argentina, one of the world’s largest exporters of food, is ramping up its agricultural produce, its main exports, to drive in scarce dollar liquidity to boost its economy.

Nigeria’s public debt has ballooned to an all-time high of N134.2 trillion and it is expected to reach N136 trillion with the fresh borrowing of $2.2 billion (N1.8trn); its debt-to-GDP ratio rose to 50.7 percent in October 2024 from 46.1 percent in the corresponding period of 2023, according to the IMF.

In July this year, a supplementary budget of N6.6 trillion was sent to the Senate due to a budget deficit of N9.18 trillion driven by various factors, including substantial non-debt recurrent expenditures (N8.76 trillion), debt servicing (N8.27 trillion), and capital expenditures (N9.99 trillion).

The 2025 budget proposal of N47.9 trillion is a 36.62 percent increase from the amended N35.06 trillion budget for 2024. This upward trend in government expenditure continues against the backdrop of weak revenue generation and heightened economic challenges.

Fiscal prudence to the rescue

Every of the economic gains the Milei-led government has seen were consolidated by fiscal discipline, lower deficits and reduced money growth.

He was able to pull off a “miracle” bringing back a country that’s suffering from hyperinflation and synonymous with economic crisis by slashing public spending by 30 percent in real terms, achieving fiscal balance in his first month in office.

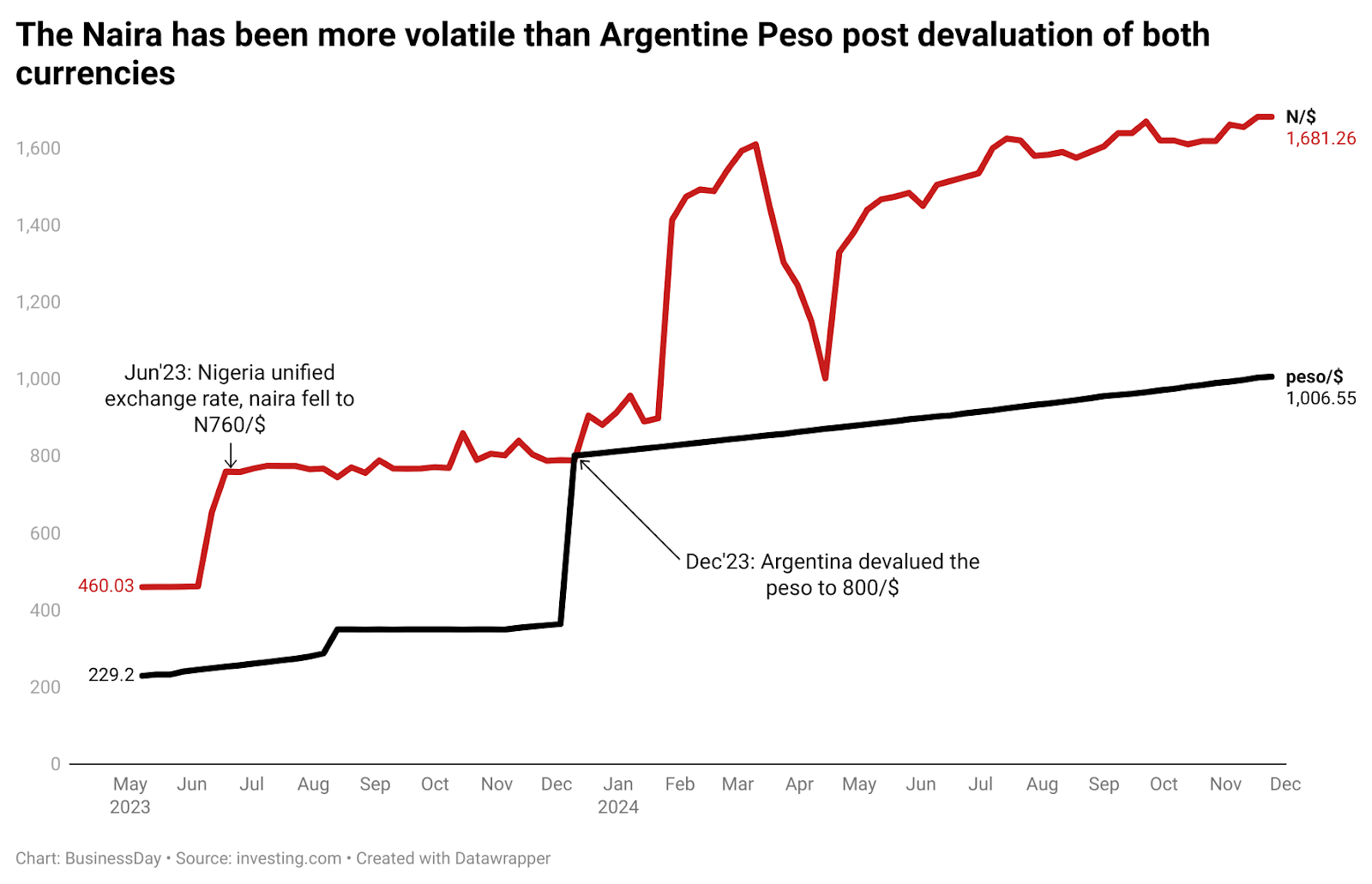

Like Nigeria, Argentina devalued its currency, the Peso, by 50 percent, slashed state subsidies for fuel, and raised import taxes, narrowing the black-market premium from over 100 percent to 25 percent in just about 11 months in office.

“The worst is past,” Milie said in an interview with Financial Times. “More than 80 percent of economic indicators have turned positive real wages have been growing for the past four months.”

But these reforms are not without its twists too. Poverty in the South American nation swelled to 53 percent while unemployment accelerated to 7.6 percent in the first half of this year, a sharp rise from 6.2 percent in the same period last year.

While confidence in Argentina’s economy is gradually returning due to strict fiscal balance and reduced government expenditure, the case for the most populous nation in Africa is different.

Since the naira has been devalued last year, it’s lost over 70 percent of its value, making it one of the worst performing currencies in the world. This is despite the recent increase in the country’s foreign reserves.

Critics have argued that the policies were hurriedly made, and that the government had put the cart before the horse. Some noted that the reforms were wrongly sequenced, pointing in the direction of Milei experiment.

“Nigeria has all the potential. The reforms are here to stay, but the government needs to cut its wasteful spendings just like Argentina and widen its revenue net,” a renowned economist who doesn’t want to be mentioned said.