Investors who are looking for direction in the Nigerian equity market in 2019, particularly for stocks listed in the banking sub-sector, will do themselves a great deal of good by reading the latest projections for the nation’s equity market in the RMB Nigeria Stockbrokers’ equity report.

Entitled “Nigerian Banks: A leap of faith. Take it”, the report identifies banking stocks both foreign and local investors could bet on for the remaining part of the year. The recommended stocks are supported with tested and proved technical and fundamental analyses.

It will be recalled that following the bearish run in 2018, where the equity market ended the year at -18.8 percent which amounted to over N2 trillion loss in market capitalisation, investors have remained cautious in their moves in the market year-to-date, due partly to the forthcoming general elections and the paucity of reliable equity research reports.

In their latest report, analysts at RMB Nigeria Stockbrokers rated Guaranty Trust Bank (GTB), Zenith Bank, and the United Bank for Africa (UBA) as overweight, implying that these stocks will outperform peers in the industry this year. On the contrary, Access Bank, First Bank of Nigeria Holding Company and Stanbic IBTC Bank were rated as equal weight. Access Bank’s current rating is subject to review following the on-going merger with Diamond Bank.

“This is mostly on the expected binary outcome of key milestone events in 2019e, such as the resolution of Atlantic Energy and sale of the Ontario asset for FBNH and improved funding costs and possibly a relaxed effective CRR for Access Bank, which could support appreciable re-rating. On average, our banking coverage is trading on a 2019e P/B of 0.8x on ROE of 19.5 percent, cheaper than their Middle East and African peers’ 1.3x on 14.5 percent ROE. On an absolute basis, we see an average potential total return of 42 percent for our coverage”, the analysts said.

“In a basic sense, if an analyst rates a stock as “overweight,” he or she thinks that the stock will perform well in the future. They believe the stock is worth buying and could outperform the broader market and other stocks in its sector. On the flipside, an “underweight” rating means the analyst thinks future performance will be poor. One can view “overweight” and “underweight” as being synonyms for “buy” and “sell,” The Balance, a financial intelligence source said.

The ratings assigned to the aforementioned stocks follow a cautious short-term outlook from a loan book growth which is expected to witness 5 percent year on year particularly in the first half of the year, with expectation that loan growth to pick up in the second half of 2019 and to hit about 11 percent year on year thereafter through 2020. In addition, these stocks are trading very cheap, with a 2019e price book ratio of 0.8x and return on equity of 19.5 percent. These compare with 1.3x, 1.1x and 1.4x for Middle East and Africa, Kenyan and Egyptian banks respectively.

The six banks covered in the analysis, which are GTB, Zenith, UBA, Access, FBNH and Stanbic IBTC, have a combined N2.8 trillion market capitalisation, which translates to 25 percent of the market capitalisation of the Nigerian capital market in the second week of January 2019.

Another factor considered was the concentration of aggregate loans. According to RMB Stockbroking analysts, the loan book of the Nigerian banking system was concentrated in two sectors, which are services, and, oil and gas. Based on their findings, 37 percent of the loans of the six banks were concentrated in the services sector, and to be followed by oil and gas at 23 percent. Combined, these sectors accounted for 60 percent of the Nigerian banking system’s loans.

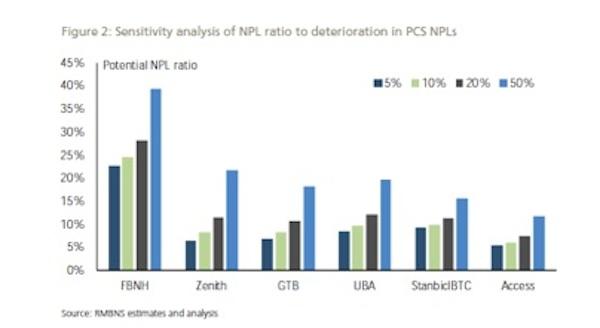

Further, Stanbic IBTC, Zenith and GTB showed the highest resistance to capital erosion from deteriorating asset quality based on the stress test conducted. In other words, the three banks could accommodate non performing loans rising over the level each bank recorded in the first half of 2018, without violating the regulatory 16 percent capital adequacy ratio (CAR).

What sets these banking stocks apart?

GTB

The target price for GTB is N48 just as the stock presently trades at N32.10 per share. It is believed that GTB will exhibit a ROE of 26 percent before year end while its valuation relative to peers is at premium. GTB’s earnings and loan book are attractive compared to Tier 1 peers. And based on the stress analysis, the bank’s return on equity has the potential to remain above its cost of equity just as the quality of its loan book relative to other Tier 1 banks stands at 82 percent as against 75 percent for others.

However, with 21 percent of its loan portfolio exposed to the Nigeria’s upstream sector, and 38 percent across oil and gas value chain, there is likelihood that GTB could witness 10 percent deterioration in its upstream loan book, implying that the year-end NPL could rise to 7.3 percent from the present 4.30 forecast for 2019e.

Zenith Bank

Zenith Bank is also rated overweight as it is expected to hit N29 per share based on the current valuation. The report suggests a 47 percent return inclusive of 14 percent dividend yield. Zenith Bank trades on a 2019e price book ratio and return on equity of 22 percent.

Zenith Bank’s management is reputed for having strong attitude towards value creation which it has done overtime by lowering funding cost with a multi-period low cost of funds of 3.3 percent as at September 30, 2018.

“From the analysis above, a 120bp decline in cost of funds relative to our expectations could increase EPS by 13 percent and vice versa. Similarly, we find our valuation to be sensitive to cost of funds: on our estimates, a 100bp change in cost of funds could lead to a N5/share change in our valuation, based on our estimates”, the RMBN analysts said.

UBA

United Bank of Africa’s (UBA) target price is N11 per share and it presently trades at N7.25 per share. This projection is hinged on its diversification strategy and the growth momentum from its African subsidiaries. Based on the estimates, UBA’s African subsidiaries are projected to deliver 49 percent of its earnings in 2019 as against 46 percent in 2018. The projected 2019 earnings forecasts are anchored on a solid 20 percent year on year growth from its African subsidiaries. Those in Nigeria are projected to grow earnings by 5 percent.

TELIAT SULE