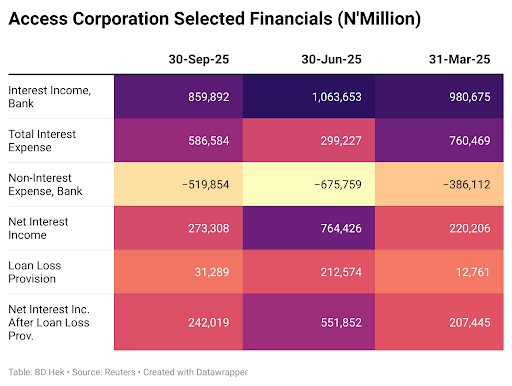

| Nigeria’s Access Corporation is a classic tale of ambition running ahead of immediate returns. Over the years, the banking giant has stitched together a straggly empire across continents as it pursued a strategy of ruthless expansion. With the grand vision of building a seamlessly integrated global network, it now faces the unfortunate reality that its financial performance crawls behind its peers and wobbles against market expectations.

While competitors tightened their focus, Access opened its chequebook. Fanfare and promises of synergies and market dominance greeted each deal. And as it completed its fourth cross-border deal in July this year after acquiring Mauritius-based Afrasia Bank to solidify its footprint in the Indian Ocean hub, its empire-building kicked into overdrive. A $109.6 million (N159 billion) swoop for Kenya’s National Bank in October pushed its East African dreams as its Kenyan unit lost $1.47 million (2.13 billion). A string of buys since 2019 including a swoop on Nigeria’s Diamond Bank had propelled it to top Nigeria’s banking sector by customer base, consistent with a five-year plan to 2027. The aim is to move from base expansion to optimality, with investment in people, technology and infrastructure knitting it all together. |

|

| The ambition is bold, but the numbers are a sobering tale of toil. Half-year 2025 pre-tax earnings slumped from N360 billion to N303 billion despite a 46 per cent jump in interest income to N1.94 trillion. Return on equity (ROE) perishes at 11.4 per cent. Investors in Access stock have rued their investment decision as they watched their counterparts who staked money in rivals like Zenith, GTCO, and UBA book stock gains of as much as 62% in the year compared to their meagre 4.8 per cent. Market expectations for bumper harvests are mired in mirage as delays in interim results fan doubts. Analysts say that margins have been slashed by integration costs and FX pressures as the N42 trillion balance sheet swells, but each Naira delivers a languid punch.

Despite Board’s defence that this is a bridging cost of a promising strategy, analysts point at a two-fold risk of opportunity cost and execution risk. Access is pursuing scale, but its rivals are driving efficiency, generating cash, reducing debt, and rewarding investors. Moreover, Access’ larger a portfolio and expanded geographical play implies more laboured integration and enhanced risk of culture mismatch and regulatory friction. Will Access show clear signs of accelerating returns to buoy sliding investors’ tolerance or will the empire bulk under its own weight. For investors, it is time for patience or a stiff drink. Africa’s largest producer, Dangote Cement, earned a landmark N743 billion for the first nine months of 2025, surpassing its earning for the whole of 2024, driven majorly by increase in cement prices. Rival BUA Cement’s after-tax earnings spiked by 492 per cent to N290 billion, while Lafarge Africa posted N208 billion in earnings. These manufacturers are the legs of Nigeria cement industry’s tripod, steadied by import bans. They all thrive on cement prices that have doubled in recent years. They have priced out small builders and low-income dreams. Thus, infrastructure booms and government contracts pad revenue and residential demand languishes as many families opt for shanties over unaffordable bricks. With Nigeria’s housing shortfall estimated at over 28 million units, the irony bites harder: the fortunes of the cement makers are toughening the plight of homeless Nigerians. High input costs and land-hoarding worsen the deficit, but manufacturers’ pricing discipline suppresses mass adoption. Nigeria’s cement market grows at 8.4% each year, estimated to reach $1.44 billion by the end of 2025. This veils a segmented boom that favours the elite, leaving the masses to boodle. A pragmatic way out? The Nigerian government should partner with the manufacturers to adopt an approach bordering on shared value, in which case the cement makers could introduce a lower-cost cement for the affordable-housing segment. Prices will be close to “cost-plus”, not margin-maximising. This implies that the government will complement this effort through actionable affordable housing programmes to secure volume and distribute at a modest margin. The manufacturers should be shifting their cement boom to housing boon, roofing the nation and cementing their dominance in the long-term. The alternative is a situation with a distressed populace and idle potential languishing in the mud. NB Plc: A Frothy Brew of Prospect and Price The outlook is cautiously refreshing, with analysts fixing 2025 revenues at N1.5 trillion (c.$1 billion at current rates). Though a down from the previous N1.59 trillion forecast, this still reflects a robust 38 per cent growth. As the festive season beckons, can the cheer spark recovery in the fourth quarter? This can happen if inflation lessens the force of its bite and Naira remains stable to sustain premiumisation firepower that pushed Gross margin to 39.7 per cent. It was 29.5 per cent in 2024. NB has convinced consumers to ignore their strained wallets and trade up to premium. |

|

| Costs are under the tap too, narrowing markedly to 60 per cent, and hinting at staying power of the margin gains. Procurement efficiencies and FX stability provided succour to the devaluation tragedy of 2024. Gross and operating margins are expected to leap above historical levels to 42 per cent and 24 per cent.

However, a hike in corporate taxes to 34 per cent and a one-off hit from the N6 billion impairment on the integration of the South African drinks group Distell and a hiked tax rate to 34 per cent have diluted earnings forecasts. 2025 per share earnings have been recalibrated downwards from ₦5.57 to ₦5.28. This is still a remarkable recovery from ₦12.07 loss per share in 2024, just the froth has flattened, scraping the target price to N80 per share. This is a modest upside that justifies a “hold” rating. NB trades at a discount to regional peers on key multiples as ongoing risks appear to have been incorporated. Having adroitly managed costs and product mix, the brewer hopes for a buoyed Nigerian consumer spending. Without this, NB’s shares prospects may remain just as balanced as a well-spurted Legend Stout that promises a rich flavour but requires patience to fully appreciate. Investors may then opt for a slower pour. |