At 26, Nafisa Musa knows how to stretch a naira. Living in Kano and juggling a side hustle in phone repairs with part-time studies, she rarely has a fixed income. Yet every month, she scribbles down savings goals in a weathered notepad.

ŌĆ£I try to save N5,000 monthly,ŌĆØ she says, ŌĆ£but sometimes I have to break it for emergencies or food. Still, I try.ŌĆØ

Emenugha Victor, a self-employed Nigerian, uses Piggyvest to lock away 50-60 percent of his funds, living on what is left. He doesnŌĆÖt classify his saving pattern as more or less, but saves when necessary. He also spends less, rarely touches his savings, and lists food, data, and transportation as his main expenses.

For Chinedu Herbert, a 24-year-old entrepreneur in Enugu, money comes in waves. ŌĆ£Some weeks I get good client payments; other times, nothing for days,ŌĆØ he says. His weapon of choice? A budgeting app that helps him track expenses and set saving goals. ŌĆ£Without it, IŌĆÖd just be guessing.ŌĆØ

In Kaduna, 21-year-old student Ogu Cletus Chibueze leans heavily on fintech platforms like Opay and Palmpay not just for transactions but for peace of mind. ŌĆ£I lock small money there so I wonŌĆÖt touch it. ItŌĆÖs like hiding it from myself,ŌĆØ she says with a laugh.

Read also:┬ĀManaging the rising cost of living, tailored wealth building plans for Nigerian millennials and Gen Z

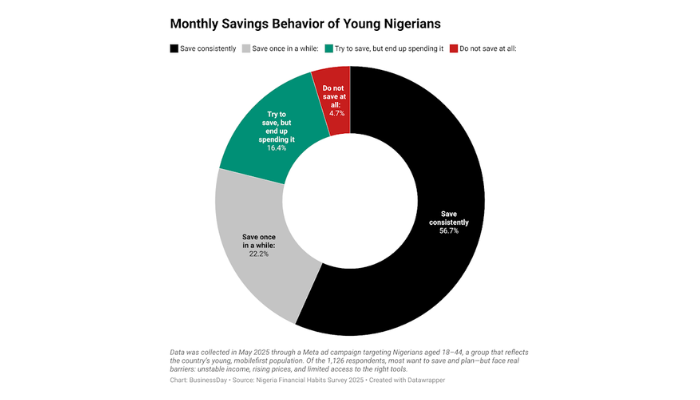

These personal stories reflect a broader, data-driven picture painted in the Nigeria Financial Habits Survey 2025, published by research and communications firm Column. Drawing responses from 1,126 young Nigerians aged 18-44, the report reveals a generation striving to plan, budget, and save, despite inflation, income instability, and digital gaps.

It said more than half of the respondents, 56.7 percent, save consistently, and 22.2 percent save once in a while. Only 4.7 percent admitted to not saving at all. But these good intentions run into harsh realities. A third of respondents (36.3 percent) said they only save ŌĆ£sometimes,ŌĆØ and nearly one in five (19 percent) said they canŌĆÖt save at all, either because their income is too low or too unstable.

ŌĆ£Saving is no longer just about willpower,ŌĆØ the report notes. ŌĆ£ItŌĆÖs about capacity.ŌĆØ Even those who do save tend to put aside small amounts: 35 percent save between 11 percent and 25 percent of their income, while 27.7 percent save just 1ŌĆō10 percent.

The report titled ŌĆ£How Nigerians Save, Spend, and Use Financial ToolsŌĆØ disclosed that motivations for saving are rooted in survival. Emergencies topped the list (53.2 percent), followed by specific goals like education or business (28.9 percent). Fewer than one in ten saved to build a general financial cushion.

Most people still trust traditional banks when it comes to saving; 79.3 percent keep their money in a bank account. However, fintech apps are gaining ground, with 23.4 percent using them.

According to the report, most respondents are comfortable using financial apps. 96.9 percent reported using at least one, with Opay (63.9 percent) and Palmpay (15.3 percent). Yet while digital adoption is widespread, deep financial engagement is not.

ŌĆ£Only 5.2 percent of Nigerians use dedicated budgeting apps, and 36.9 percent donŌĆÖt track their spending at all. Among those who do, the majority still rely on manual methods, like pen-and-paper, memory, or notes apps,ŌĆØ it said.

This gap between digital access and meaningful use is a wake-up call. ŌĆ£WeŌĆÖre seeing a shallow engagement with financial tools,ŌĆØ the report said. ŌĆ£People have the apps, but theyŌĆÖre not using them to their full potential, largely because they donŌĆÖt meet users where they are.ŌĆØ

Meanwhile, 75.2 percent of respondents said they want to see all their financial activity in one place, underscoring the need for unified dashboards and open banking solutions.

Read also:┬ĀContending with rising costs amid static income

Spending patterns reflect harsh economic realities.

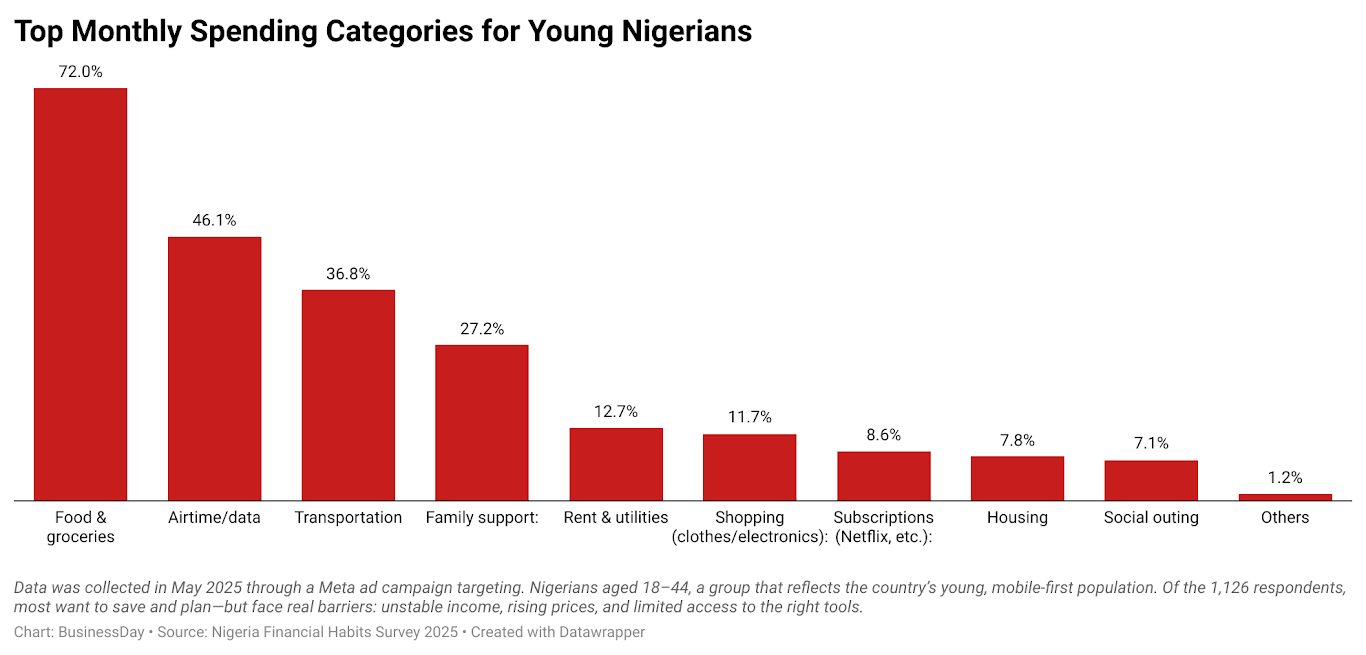

The report pointed out that Nigerians spend first on survival. Food and groceries were the top expenses for 72 percent of respondents, followed by airtime/data (46.1 percent), transportation (36.8 percent), and family support (27.2 percent). Subscriptions like Netflix or Spotify barely made the list at 8.6 percent, revealing how discretionary spending takes a back seat.

Budgeting isnŌĆÖt universal either. It said. Just over half (57.2 percent) say they stick to a budget, while 17.1 percent admit they often overspend. The reasons? Not recklessness, but necessity. Many underestimate expenses (45.6 percent) or face unexpected emergencies (28.8 percent).

ŌĆ£ItŌĆÖs not that people donŌĆÖt want to plan,ŌĆØ the report explains. ŌĆ£ItŌĆÖs that prices change so fast, and income is so unstable, that planning becomes a luxury.ŌĆØ

Oliver, a direct sales agent who prefers physical cash savings, said that itŌĆÖs a more disciplined approach since digital access can make spending too easy.

He spends more of his savings many times, and his top expenses are food, data, and transportation.

Impulse spending, triggered mostly by discounts, emergencies, or peer influence, often leads to regret. Still, a significant 38.4 percent say they feel motivated to regain control afterward.

The latest data shows that inflationary pressures, while still elevated, have begun to soften. NigeriaŌĆÖs headline inflation rate eased for a second consecutive month to 22.97 percent in May 2025, down from 23.71 percent in April, according to the National Bureau of Statistics (NBS).

On a monthly basis, inflation slowed to 1.53 percent from 1.86 percent the previous month, a sign that the governmentŌĆÖs macroeconomic reforms may be starting to yield results.

Despite this, NigeriaŌĆÖs private sector growth drops in June, with business activity slowing to the lowest in seven months despite signs of easing inflation, the latest Purchasing ManagersŌĆÖ Index (PMI) report by Stanbic IBTC Bank shows.

According to the report, the headline PMI fell to 51.6 in June from 52.7 in May, marking the weakest expansion since the current growth streak began late last year.

While the reading remains above the 50.0 threshold, a sign of improving business conditions, the slower pace underscores the fragile nature of NigeriaŌĆÖs economic recovery.

ŌĆ£Despite remaining in expansion territory, the decline signals a modest improvement in operating conditions, primarily driven by a notable slowdown in output, new orders, and purchasing activity,ŌĆØ the report said.

Read also:┬ĀRebased inflation rate does not resolve rising cost of living ŌĆō LCCI

What is triggering this change in the payment system?

For banks, the message is clear: evolve or risk irrelevance. ŌĆ£Banks are trusted storage lockers, but not active financial partners,ŌĆØ the report said. Young users want more than safekeeping; they want automatic savings, goal tracking, and visual dashboards. Embracing open banking frameworks is key.

Fintechs, on the other hand, are already a step ahead, but need to close the usage gap. While interest in smart tools is high, adoption is low. Embedding automation, simplicity, and integration into the user journey could turn fintechs into the true financial homes of young Nigerians.

Policymakers also have a role. With 46.1 percent of users citing airtime/data as a key expense, affordable mobile access is vital. Support for job creation, small business growth, and digital infrastructure will go far in turning financial aspirations into reality.

Moreover, regulation must keep pace with innovation. While Nigeria introduced open banking guidelines in 2023, implementation remains sluggish. Speeding this up could unlock personalised financial ecosystems for millions.