After three years of digital isolation, Nigerian banks have quietly resumed international transactions on naira-denominated debit cards, reconnecting millions of citizens to global platforms from Amazon to Netflix. This policy reversal, while seemingly technical, represents a profound shift in Nigeria’s economic strategy—one that signals both growing confidence in the foreign exchange market and the fragile nature of the country’s macroeconomic recovery.

The Genesis of Financial Isolation

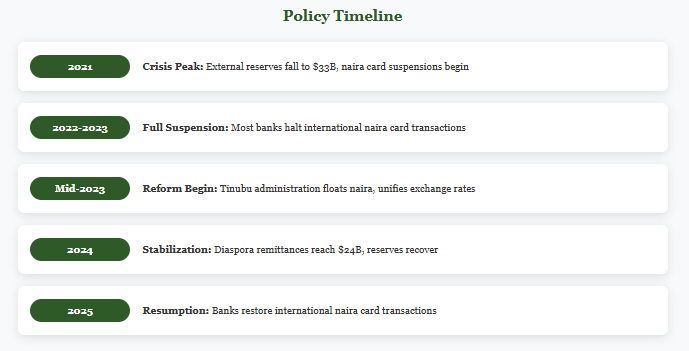

The suspension of international naira card transactions between 2021 and 2024 was born of desperation, not design. Nigeria found itself trapped in a perfect storm of economic pressures: external reserves had plummeted from $45 billion in 2019 to just $33 billion by 2021, oil production was hampered by theft and infrastructure decay, and the Central Bank of Nigeria’s rigid exchange rate regime had created dangerous arbitrage opportunities. International card transactions, though individually modest, represented a cumulative drain of approximately $1.2 billion annually on scarce dollar reserves. With Nigerians exploiting the gap between official and parallel market rates—using cards priced at official rates for transactions valued at black market premiums—the CBN faced an impossible choice: maintain the illusion of exchange rate stability or preserve what remained of the country’s external buffers. The suspension was, in effect, an informal capital control—a crude but necessary instrument to prevent total reserve depletion during Nigeria’s most acute balance-of-payments crisis in decades.

The Costly Arithmetic of Survival

The three-year restriction achieved its primary objective: preserving foreign exchange for critical imports. CBN data suggests the policy saved an estimated $3.5 billion in forex outflows, providing breathing room for the economy’s most vulnerable sectors. Domestic payment platforms experienced a 40% surge in adoption, while import substitution received an inadvertent boost—rice production, for instance, grew by 18% as businesses were forced to source locally. Yet these gains came at a steep price. Nigeria’s burgeoning digital economy withered as freelancers, remote workers, and small businesses lost access to global platforms. The policy inadvertently accelerated informal dollarization, with demand for peer-to-peer cryptocurrency transactions and offshore accounts surging. Rather than solving the underlying forex crisis, the restrictions merely redirected it into less transparent channels.

The human cost was equally significant. Millions of Nigerians found themselves financially severed from the global economy, forced to rely on expensive workarounds or abandon international transactions entirely. The suspension highlighted the brutal trade-offs facing policymakers in a resource-constrained economy: short-term stability versus long-term competitiveness.

The Turning Tide

The recent lifting of restrictions reflects a confluence of factors that have gradually restored confidence in Nigeria’s foreign exchange market. Most significantly, the Bola Tinubu administration’s decision to float the naira in mid-2023 eliminated the dangerous arbitrage opportunities that had plagued the previous regime. The convergence of official and parallel market rates—now trading within ₦30 per dollar of each other—has reduced speculative pressures and restored some measure of market confidence. External reserves have rebounded to $38 billion by June 2025, supported by higher oil output (rising from 1.2 million barrels per day in 2023 to 1.6 million currently) and a surge in diaspora remittances, which reached $24 billion in 2024. Perhaps more importantly, May 2025 alone saw total forex inflows rise by 62% month-on-month to $5.96 billion, driven by increased participation from both domestic and foreign investors. The CBN’s embrace of market-driven foreign exchange pricing has been central to this recovery. By abandoning the fiction of an artificially strong naira, policymakers have eliminated the distortions that made the previous system unsustainable. The result is a more transparent, albeit weaker, exchange rate that better reflects economic fundamentals.

Macroeconomic Implications and Risks

The resumption of international naira card transactions carries profound implications for Nigeria’s economic trajectory. On the positive side, it represents a vote of confidence in the naira’s stability and the CBN’s reform agenda. Banks’ willingness to resume these services suggests they believe current forex liquidity levels are sustainable—a marked shift from the pessimism of previous years. For consumers, the immediate benefits are tangible. Millions of Nigerians can now access international services directly, reducing reliance on expensive parallel market solutions. The creative and digital economy, which thrives on cross-border transactions, will receive a significant boost. Banks themselves stand to benefit, with the Nigeria Deposit Insurance Corporation projecting a ₦120 billion annual increase in fee income from international transactions.

However, significant risks remain. The policy will inevitably increase forex outflows as pent-up demand is released. While banks have implemented spending limits—typically ranging from $500 to $4,000 per quarter—the cumulative impact could strain the still-fragile forex market. The CBN must remain vigilant against speculative abuse, particularly the use of cards to fund offshore trading accounts. More fundamentally, the resumption of international transactions does not address Nigeria’s underlying structural challenges. The economy remains dangerously dependent on oil exports, vulnerable to global price shocks and production disruptions. Without genuine diversification, any improvement in forex liquidity remains hostage to external factors beyond Nigeria’s control.

The Path Forward

The naira card revival represents neither a complete victory nor a cosmetic gesture—it is a carefully calibrated step toward macroeconomic normalization. It suggests that the worst of Nigeria’s forex crisis may be behind us, but it also highlights the economy’s continued fragility. To sustain this progress, policymakers must resist the temptation of premature liberalization. The CBN’s monitoring systems must be robust enough to detect and prevent speculative abuse. More importantly, the government must accelerate structural reforms that address the root causes of forex instability: over-reliance on oil, weak manufacturing capacity, and inadequate export diversification.

The resumption of international naira card transactions is ultimately a test of Nigeria’s commitment to market-oriented reforms. If managed prudently, it could mark the beginning of a new chapter in the country’s economic development. If not, it risks becoming another cautionary tale of policy reversal driven by short-term pressures. For now, millions of Nigerians have regained a vital financial lifeline. Whether this privilege proves sustainable depends on the choices made in the corridors of power in Abuja—and on the global economic forces that continue to shape Nigeria’s destiny. The naira’s journey back to international respectability has begun, but the destination remains uncertain.