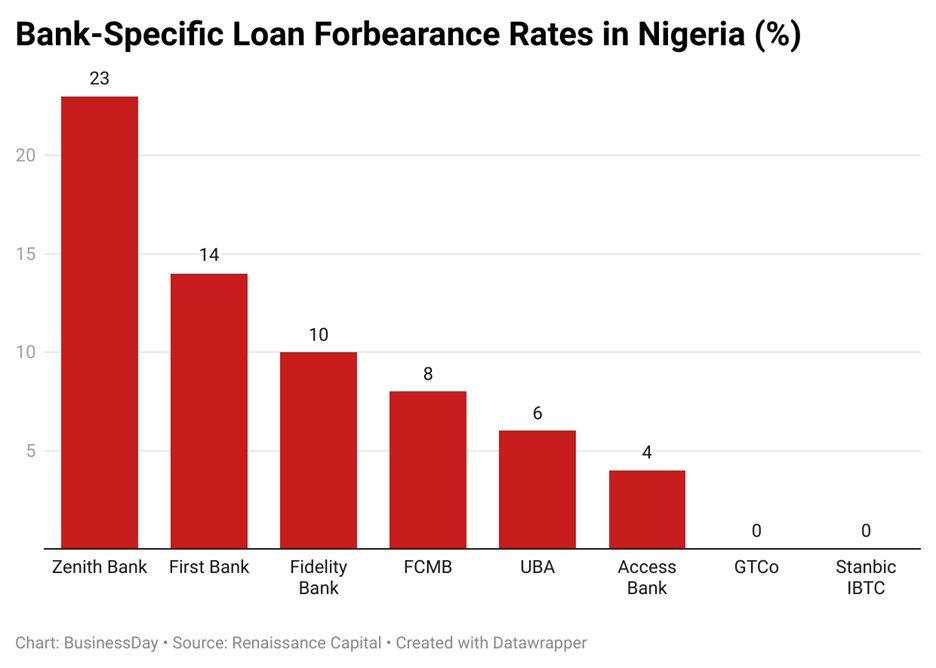

At a time when Nigerian banks are being told to come clean about their risky loans, GTCO and Stanbic IBTC are already ahead of the curve. A new report by Renaissance Capital (RenCap) reveals that both lenders recorded zero forbearance, a bold statement in today’s tightly watched financial sector.

Their position comes as the Central Bank of Nigeria (CBN) shifts away from post-COVID leniency and tightens the screws on the financial system. In a sharp policy turn, the CBN has ordered commercial banks to halt dividend payments, suspend bonuses, and freeze offshore investments until they fully recognize risky loans and clean up their balance sheets.

For the banks still holding on to old regulatory breathing room, the message is simple: no more window-dressing.

Forbearance is no longer a free pass

Forbearance used to give banks a way to reclassify troubled loans without showing them as bad. It bought time during the worst of the economic storms, currency crashes, inflation, and COVID disruptions. But that lifeline has now been cut.

The RenCap report confirms this shift: Forbearance-related exposures are now being pushed straight to the profit-and-loss account and equity no more hiding. This move, while painful for banks’ earnings, is aimed at restoring investor confidence and revealing the real health of the system.

Who’s still exposed?

While GTCO and Stanbic IBTC show no loan forbearance, other banks still have sizable exposures. According to RenCap estimates, Zenith Bank’s 23 percent of its total loan book is under forbearance. First Bank, 14 percent; Fidelity Bank, 10 percent; FCMB, 8 percent; UBA, 6 percent; and Access Bank, 4 percent.

These numbers reflect just how reliant some banks have been on regulatory relief. GTCO, in contrast, cleaned its books last year by making full provisions and write-downs — a move that now puts it in a stronger position as regulatory heat rises.

Why these matters

In an environment of rising fiscal risk, weak investor confidence, and currency volatility, banks with transparent books and strong buffers will have the edge. For shareholders, this shift may mean slimmer dividends in the short term. But in the long run, disciplined risk management and regulatory compliance will be key to attracting fresh capital.

“Investors are watching closely. No one wants surprises anymore,” said one Lagos-based analyst. “The banks that have nothing to hide are going to be the first to raise new money when the time comes.”

What it means for the sector

This isn’t just about cleaning up past mistakes, it’s a signal of how the financial system will operate going forward. The end of forbearance marks the beginning of stricter oversight, more honest accounting, and tighter discipline.

Banks will now need to focus more on actual lending to the productive sectors, improve operational efficiency, and double down on digital tools to stay competitive. The old model of relying on short-term gains and regulatory cover is no longer sustainable.

The bigger picture

Nigeria’s economy needs credible banks to survive its many challenges, from a falling naira to rising debt costs. Without strong financial institutions, the private sector can’t grow, and the public sector can’t manage its budget shocks. GTCO and Stanbic IBTC are showing what financial discipline looks like. Others will either catch up or be left behind.

As one market watcher put it, “The era of accounting tricks is over. Now, we’ll see who’s really solid and who’s been coasting on regulatory grace.”

This reset may be painful, but it’s long overdue. In banking, as in life, facing the truth is the first step toward real strength.