When Fela Kuti released his ŌĆ£Overtake don Overtake OvertakeŌĆØ song in 1989, he likely thought the issues raised in what could be referred to as an activism music would have been resolved. Sadly, more than three decades later, the issues linger.

In the last 10 years, devaluation has hit several Nigerian families hard. Doris Onu, an entrepreneur who suffers frequent asthmatic attacks, could afford her inhaler, which sold for less than N3,000 in 2014. That same brand has jumped 400 percent to N15,000 a decade later, leaving the 23-year-old sourcing available alternatives to her plight.

ŌĆ£The inhaler was just steadily rising, and each time I inquired, the pharmacist would say the nairaŌĆÖs rate is impacting the cost,ŌĆØ Onu, who owns a salon at Igando, Lagos, said. ŌĆ£Though the price is gradually falling, I doubt if it could ever drop to where it used to be.ŌĆØ

For Abdul Haruna, N100,000 in 2014 could afford to pay the school fees of his five children. Now, he spends N1.5 million on school fees every term.

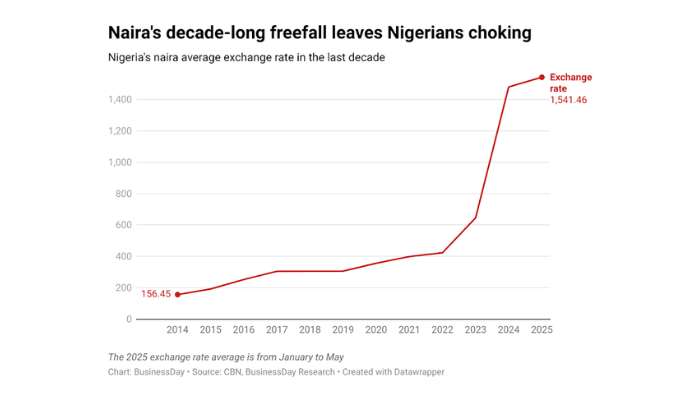

For over a decade, the Nigerian naira has been in retreat. In 2014, a dollar bought N160. By May 2025, it could buy almost N1,600. The depreciation has accelerated, especially since mid-2023 when the central bank scrapped the official exchange rate peg in favour of a unified, market-driven rate.

Read also:┬ĀHow naira devaluation is reshaping NigeriaŌĆÖs economy

That reform won applause from foreign investors and multilateral banks, but it has seen the currency lose more than 70 percent of its value, leaving ordinary Nigerians grappling with economic pain with little relief in sight.

In no other major African economy has currency devaluation been so prolonged or so punishing. While thereŌĆÖs been relative stability in recent times, the ripple effect is still choking millions of Nigerians.

The steep devaluation of the naira together with the abolishing of fuel subsidies by the President Bola Tinubu administration two years ago stoked inflation and triggered the worst cost-of-living crisis in a generation.

Food prices, which were already elevated due to insecurity in northern farming zones and global supply shocks, have surged further. Imported goods, medicines, school books, and auto parts are now unaffordable for many.

These rising cost pressures saw NigeriansŌĆÖ per capita income plummet by a staggering 72.8 percent, the lowest itŌĆÖs been since 2004, dropping from approximately $3,223 in 2014 to $835 this year, according to recent estimates by the International Monetary Fund (IMF).

But the pains are even direr for Mimi Agboola, a parent with two kids, who will have to pay school fees and pay house rent ŌĆō both of which have more than tripled. Yet her salary has barely improved.

ŌĆ£I have had to change my childrenŌĆÖs school to a less expensive school,ŌĆØ Agboola, who works with a Lagos-based private firm, said.

Even their meals these days are not as rich as they used to be. ŌĆ£Now I try to make fish sauces, rather than giving them individual pieces of fish, because the pieces would not even go round.ŌĆØ

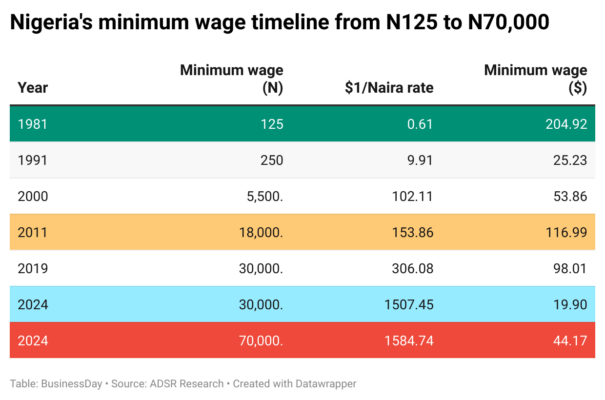

In 2011 when the countryŌĆÖs minimum wage stood at N18,000, the naira was quoted at N153.86/$, which amounted to a worker earning at least $116.99 monthly pay.

Read also:┬ĀThe devaluation of intellect in Nigeria

But as the Tinubu-led government increased the wage by 133 percent from N30,000 to N70,000 last year, the exchange rate had weakened to N1584.74/$, bringing the new minimum wage to a low of $44.17 in dollar terms as inflation and fluctuating currency had eroded the value of the wage review.

ŌĆ£What we are witnessing is not just inflation, itŌĆÖs immiseration,ŌĆØ said Michael Adeyemi, a Lagos-based developmental economist. ŌĆ£The nairaŌĆÖs decline has hollowed out the middle class and pushed millions into survival mode.ŌĆØ

The freefall is not merely a monetary story, it is the human toll that gives it weight. In Aba, once the capital of Nigerian small-scale manufacturing, fashion designers now complain they cannot import cloth from China or even thread from Turkey.

Though they acknowledged that thereŌĆÖs been some improvement in the exchange rate, the business is now largely run by entrepreneurs who have enough capital to weather the storm of any fluctuation.

ŌĆ£Our businesses are dying,ŌĆØ said Chike Udo, who runs a once-busy garment shop. ŌĆ£People now wear their old clothes until they tear.ŌĆØ

From Soludo to Cardoso

During Charles SoludoŌĆÖs tenure as the Central Bank of Nigeria (CBN) governor from May 2004 to May 2009, the exchange rate moved marginally from N132.8 to N134.5 per US dollar, a relatively stable period marked by robust foreign reserves, oil boom-era inflows, and the banking consolidation exercise, which bolstered investor confidence.

Sanusi Lamido Sanusi, who governed from June 2009 to June 2014, witnessed a more noticeable depreciation of the naira from N146.7/$ to N155.7/$. While this was still a modest shift over five years, it reflected growing pressures from falling oil prices around 2011ŌĆō2014 and increasing demand for foreign exchange.

Under Godwin Emefiele, who served from June 2014 to June 2023, the exchange rate experienced a dramatic plunge from N155.7 to N462.4, a devaluation of over N306.7 in nine years. This period encapsulated the height of NigeriaŌĆÖs forex crisis, two major recessions (2016 and 2020), prolonged periods of multiple exchange rates, capital control policies, and a dip in foreign investor confidence. The CBN, under Emefiele, was often criticised for defending the naira through aggressive interventions rather than allowing a more market-reflective rate, which created arbitrage opportunities and widened the gap between official and parallel market rates.

Read also:┬ĀGoldman says devaluation on cards again for Naira as oil sinks

Folashodun Shonubi, who briefly acted as governor from June to September 2023, oversaw one of the sharpest short-term devaluations in NigeriaŌĆÖs history, from N462.5 to N756.9 in just three months.

Olayemi Cardoso, who took over in September 2023, inherited an exchange rate of N756.9 and has since seen the official rate more than double to N1599.5 per dollar, a staggering N842.6 devaluation in under 18 months.

Plights of the people

But so far, foreign capital has trickled in, not flooded. Meanwhile, local businesses are left to navigate volatility with no safety net. Even though inflation is easing, itŌĆÖs still at a double-digit, with borrowing rate at an all-time high.

The hope is that reforms, both fiscal and structural, will eventually strengthen the naira. Yet, in markets from Kano to Port Harcourt, few are betting on a quick recovery. ŌĆ£What use is hope when you canŌĆÖt afford basic medication?ŌĆØ asked Onu in her Lagos salon.

With a population of over 200 million people, most of them under 30, the stakes are high. The nairaŌĆÖs collapse is more than an exchange rate story, itŌĆÖs a referendum on the countryŌĆÖs future.

A bag of rice stood at N9,167, according to a November 2014 commodity index by Novus Agro Nigeria. A 60kg bag of garri cost about N5,667, with a 100kg bag of maize going for N5,417.

Now, a bag of rice is over N80,000, with garri and maize more than 12 times their 2014 prices.

Read also:┬ĀNigeriaŌĆÖs debt jumps 48.6% in 2024 on naira devaluation

ExpertsŌĆÖ opinion

Ayokunle Olubunmi, head of financial institution ratings at Agusto & Co., said given the import dependent nature of the Nigerian economy, the persistent naira devaluation has raised the cost of living and moderated the standard of living.

Ayodeji Ebo, managing director and chief business officer at Optimus by Afrinvest, said over the past decade, the nairaŌĆÖs depreciation has significantly impacted both households and businesses.

For households, he said it has eroded purchasing power, driven up the cost of living, and reduced the real value of savings. For businesses, especially those reliant on imports, it has increased costs and planning uncertainty. However, some manufacturers export-driven and local, have benefited from improved competitiveness.

ŌĆ£Overall, the sustained depreciation has weighed heavily on economic stability, business confidence, and household welfare,ŌĆØ he said.