NigeriaŌĆÖs biggest palm oil maker, Presco Plc has delivered a record-breaking performance in the first quarter of 2025, with pre-tax profit nearly doubling to N58.6 billion, highlighting the strength of its integrated edible oil business model amid rising demand and disciplined cost management.

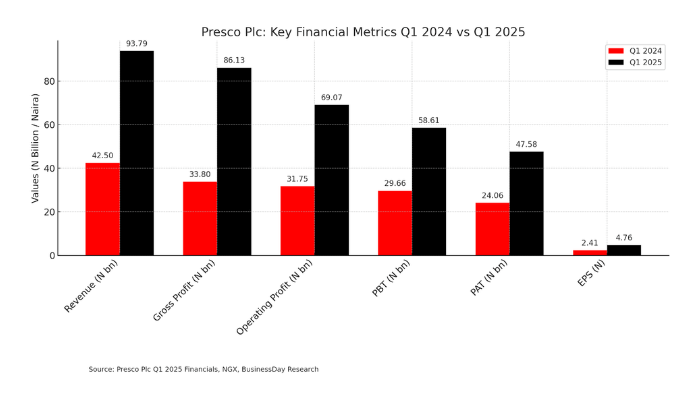

The companyŌĆÖs revenue surged by 120.4 percent to N93.8 billion, up from N42.5 billion in Q1 2024, as it capitalised on higher prices and volumes in NigeriaŌĆÖs growing vegetable oil market.

This sharp revenue expansion reflects PrescoŌĆÖs operational scale and strong downstream value chain, reinforcing its dominance in the oil palm sector.

Gross profit for the quarter jumped by 154.8 percent to N86.1 billion, while operating profit grew 117.6 percent year-on-year to N69.1 billion. The earnings momentum translated into a robust 97.8 percent rise in profit after tax to N47.6 billion, from N24.1 billion in the same period last year.

Read also:┬ĀPresco to pay N42 final dividend as profit more than doubles to N77.79bn

Earnings per share also nearly doubled, climbing from N2.41 to N4.76, providing strong signals for shareholder value creation.

Charting profitability

PrescoŌĆÖs Q1 2025 result places it among the top-performing agribusiness stocks on the Nigerian Exchange (NGX) so far this year. The companyŌĆÖs earnings before interest, tax, depreciation, and amortisation (EBITDA) rose to N71.6 billion, a 117.9 percent increase year-on-year.

Despite a 359.3 percent surge in interest expenses to N10.5 billion, the companyŌĆÖs operating income remained strong enough to absorb financing costs without denting margins.

Its EBITDA margin stood at an impressive 76.3 percent, indicating the high profitability of its vertically integrated model that spans plantation cultivation, processing, and specialty oil refining.

Balance sheet and investment posture

Presco also expanded its asset base by 15.5 percent to N548.6 billion, reflecting ongoing investments in plantation and refinery upgrades. Current assets rose by 36.1 percent to N232.4 billion, signalling improved liquidity.

However, total liabilities climbed 40.1 percent to N369.6 billion, resulting in a 15.3 percent decline in equity to N179 billion.

The equity decline is primarily due to dividend payments and capital structure realignments, according to the companyŌĆÖs investor relations team. Still, the debt-funded growth appears strategic and value-accretive, given the significant rise in profitability.

Read also:┬ĀThree things to learn from PrescoŌĆÖs profit run

Investor signals and outlook

PrescoŌĆÖs stellar Q1 earnings reinforce investor confidence in agribusiness stocks amid macroeconomic headwinds. With food inflation still high and the government focusing on local content and agricultural self-sufficiency, the company is well positioned to benefit from policy tailwinds.

The market has already begun responding to its improved outlook. Analysts expect continued earnings momentum throughout 2025, backed by seasonal harvest yields, pricing power, and enhanced refinery throughput.

ŌĆ£PrescoŌĆÖs performance reflects the strength of its integrated business model,ŌĆØ said Reji George, managing director, Presco Plc. ŌĆ£Our focus on operational excellence and value creation continues to deliver results for stakeholders.ŌĆØ

For long-term investors, the companyŌĆÖs near doubling of EPS and significant earnings leverage make it a solid defensive stock with upside potential, especially in a high-interest-rate environment where stable cash flows are highly valued.