Stable exchange rate, growing external reserves and need to checkmate government’s fiscal expansion occasioned by higher oil price benchmark and supplementary budget are possible reasons that could make monetary easing by Central Bank of Nigeria (CBN) in the next one year unlikely, analysts have said.

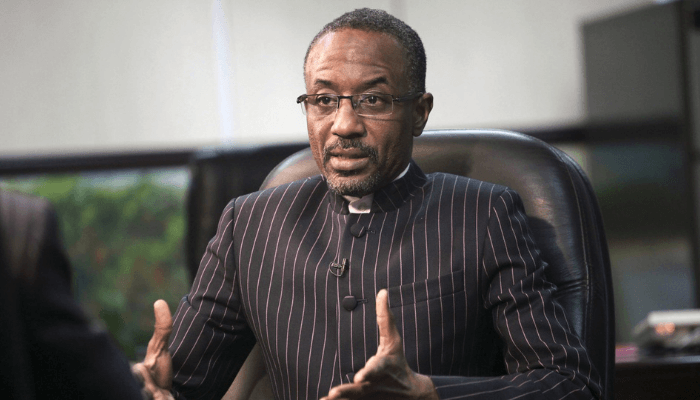

The implication is that Sanusi Lamido Sanusi, CBN governor’s tight monetary stance for over two years may be maintained for the remaining 15 months tenure as governor of CBN.

Sanusi, who was sworn in as CBN governor June 3, 2009, amidst banking crisis of confidence, solvency and liquidity, reportedly said last week that he would not seek second term, when his five-year tenure expires June next year.

The analysts are of the opinion that Sanusi may have decided against second term and consequently bow out now that the ovation is loudest considering the fact that monetary easing may not have positive effect on interest rates with the current decay in infrastructure. Also, considering the fact that the reduction in inflation is not sustainable due to the base year effect and the commencement of 2015 campaign with its attendant spending by politicians, which may likely upturn achievements recorded so far.

Read also:¬ÝWhat monetary, fiscal authorities can do to curb FX pressure

Samir Gadio, emerging markets strategist, Standard Bank, London, said, “We suspect any major shift in the CBN’s formal policy stance is improbable over the next year now that CBN governor, Sanusi, has indicated that he will not seek a second term.

“Besides, the likelihood of a cut in the MPR has reduced, given the decline in net capital inflows in Q1:13 and the continued fiscal expansion, as illustrated by the increase in the oil price benchmark to USD79 pbl in the 2013 budget.”

Ken Iwelumo, former senior vice president/Stockbroker Bank of America/Merrill Lynch, said, “I believe that Governor Sanusi will continue with his current strategy for his remaining term. His tight monetary policy has brought stability in terms of the economy, interest rates and exchange rates to Nigeria in a very unstable economic world.”

Razia Khan, analyst with Standard Chartered Bank, London, said, “Do we see a continuation of the monetary stance? That is the hope. We should not forget that interest rate policy is set by a committee rather than a single individual. Sanusi showed great courage in resisting the pressure to ease, when the beneficial impact of such easing may have been questionable, and might have put at risk Nigeria’s currency stability.”

Khan, in the recently published regional focus, ‘Nigeria’s Policy Outlook’, said, “While the calls for rate easing may be growing, we believe there are good reasons to stay on hold. January 2013 is better-than-expected inflation print was no more than a base effect. Easing, based solely on this, may be premature. The Nigerian economy has not yet seen sufficient structural change to drive inflation sustainably lower.”