The first quarter of 2025 marked a standout period for Nigeria’s exploration and production (E&P) companies. Crude oil output rose by 8.1 percent year-on-year to 1.67 million barrels per day, up from 1.54 million bpd in Q1 2024, reflecting improved operational stability and upstream activity.

Nigeria’s active rig count climbed to 38 during the period, its highest in recent years, underscoring the renewed momentum in the sector. With international oil majors such as Mobil, Shell, and Agip having exited the onshore landscape in 2024, indigenous E&P firms have firmly taken the lead. While oil prices trended lower in the quarter, higher production volumes among listed players helped cushion the impact.

Seplat Energy Plc has emerged as the country’s largest onshore E&P operator following its acquisition of Mobil Producing Nigeria Unlimited (MPNU). Aradel Holdings has also solidified its presence, with its influence bolstered by a strategic stake in Renaissance Energy, the consortium that acquired Shell’s onshore assets.

In this story, BusinessDay aims to examine which of these two powerhouses delivered stronger results in Q1 2025—and why it matters.

Read also: Aradel, Oando, Seplat: Which is a better buy option?

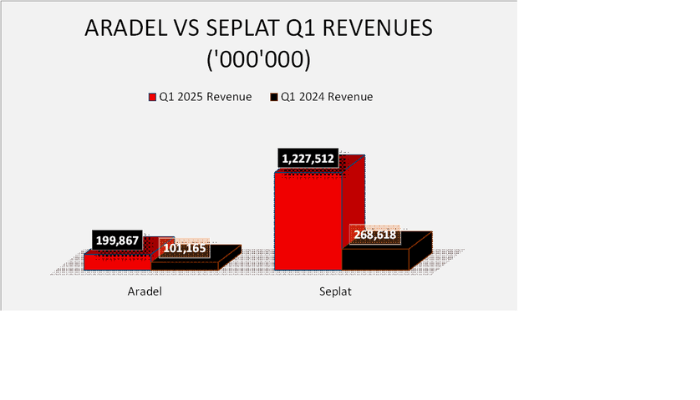

Headline Financials

Seplat recorded a staggering 350 percent year, on, year revenue growth to $809.3 million, up from $179.8 million in Q1 2024. Aradel, while trailing Seplat in absolute terms, posted an impressive 70 percent YoY revenue growth to $131.4 million, from $77.4 million a year earlier.

On the bottom line, Seplat posted a N35.4 billion net profit, recovering from a N2.9 billion net loss in Q1 2024. Aradel, meanwhile, delivered N34.2 billion in net income, its strongest quarterly performance on record.

Seplat’s earnings surge was largely driven by production, with volumes jumping 167 percent YoY to 131,561 barrels of oil equivalent per day (boepd), compared to 49,258 boepd in Q1 2024. This uplift reflects the early benefits of the MPNU acquisition.

Aradel generated significantly less from crude oil sales, $124 million during the quarter, yet its integrated model provided some support. Its refining operations contributed $36.3 million, underscoring a more diversified revenue base.

Despite Seplat’s higher profits, its net margin stood at just 3 percent, compared to Aradel’s 17 percent. On gross margins, Seplat (44 percent) outperformed Aradel (39 percent), a reversal from Q1 2024, when Aradel held a commanding 62 percent to Seplat’s 24 percent. Operating margins further reflected this shift, Aradel posted a 32 percent margin (down slightly from 35 percent in Q1 2024), while Seplat recorded a 29 percent margin, down from 46 percent.

Read also: Aradel completes $19.5m acquisition of Olo and Olo West Marginal Fields

In E&P, cash is king

Away from the profitability metrics, in terms of cash flow, Seplat posted a N328.5 billion net operating cash flow during the quarter. In Q1 2024, the group recorded a significantly lower N22.2 billion net operating cash flow.

Aradel posted a significantly lower NOCF of N30.6 billion during the quarter, marking a 45 percent year, on, year decline from the N55.8 billion NOCF recorded in Q1 2024.

The fifteen, fold uplift in Seplat’s cash generation was driven by a surge in production volumes, powered by its newly integrated SEPNU assets. Conversely, Aradel’s cash conversion was constrained by elevated project expenditures and a buildup in receivables and payables.

Notably, Aradel’s cash, flow statement shows a N30.8 billion increase in restricted cash, funds earmarked for specific, unspecified obligations further reducing its available liquidity. In Nigeria’s upstream sector where companies face combined petroleum profits tax and hydrocarbon tax, strong operating cash flow is vital to absorb hefty tax burdens and fund capital, intensive operations.

The divergence widens when we look at free cash flow. Aradel managed just N1.55 billion in FCF, while Seplat delivered a commanding N267.45 billion. This strong cash surplus allowed Seplat to fund capital projects internally, repaying N1.39 trillion of debt in Q1 even as it drew N986 billion in new borrowings, without leaning heavily on external finance.

Together, these metrics underscore Seplat’s superior cash‐generation engine and financial flexibility, while highlighting the funding and liquidity challenges Aradel must address to support its growth ambitions.

Return to shareholders

In line with its robust performance, Seplat declared a $0.046 interim dividend for Q1 2025—a 53 percent increase from the $0.03 distributed in Q1 2024. At its current share price of N5,700, Seplat trades at a price-to-earnings (P/E) ratio of 109.3x.

Aradel, which did not declare a dividend for the quarter, remains a relatively cheaper stock, trading at a share price of N448 and a P/E ratio of 57.7x. This valuation gap reflects Seplat’s stronger cash profile and consistent dividend policy, though it also leaves room for upside if Aradel can unlock greater operational efficiency.

Q1 2025 showcased two very different success stories in Nigeria’s E&P landscape. Seplat has leveraged scale, inorganic growth, and operational efficiency to emerge as a cash-generating powerhouse with strong investor returns. Aradel, while profitable and agile, faces challenges in translating top-line strength into cash flow and liquidity—critical ingredients for long-term sustainability in the oil business.

Ultimately, while both firms delivered standout net income, Seplat’s performance—measured by cash flow, production output, and shareholder returns—places it ahead of the curve in this quarter. For investors, it underscores a fundamental truth in upstream oil: profits matter, but cash is king.