Nigeria’s private sector credit extension remains significantly lower than that of its sub-Saharan African peers, despite recording a modest recovery in recent months.

According to the Central Bank of Nigeria (CBN)’s latest data, private sector credit rose by approximately 9 percent year-on-year to N76.3 trillion in March 2025, rebounding from a slight moderation observed in February.

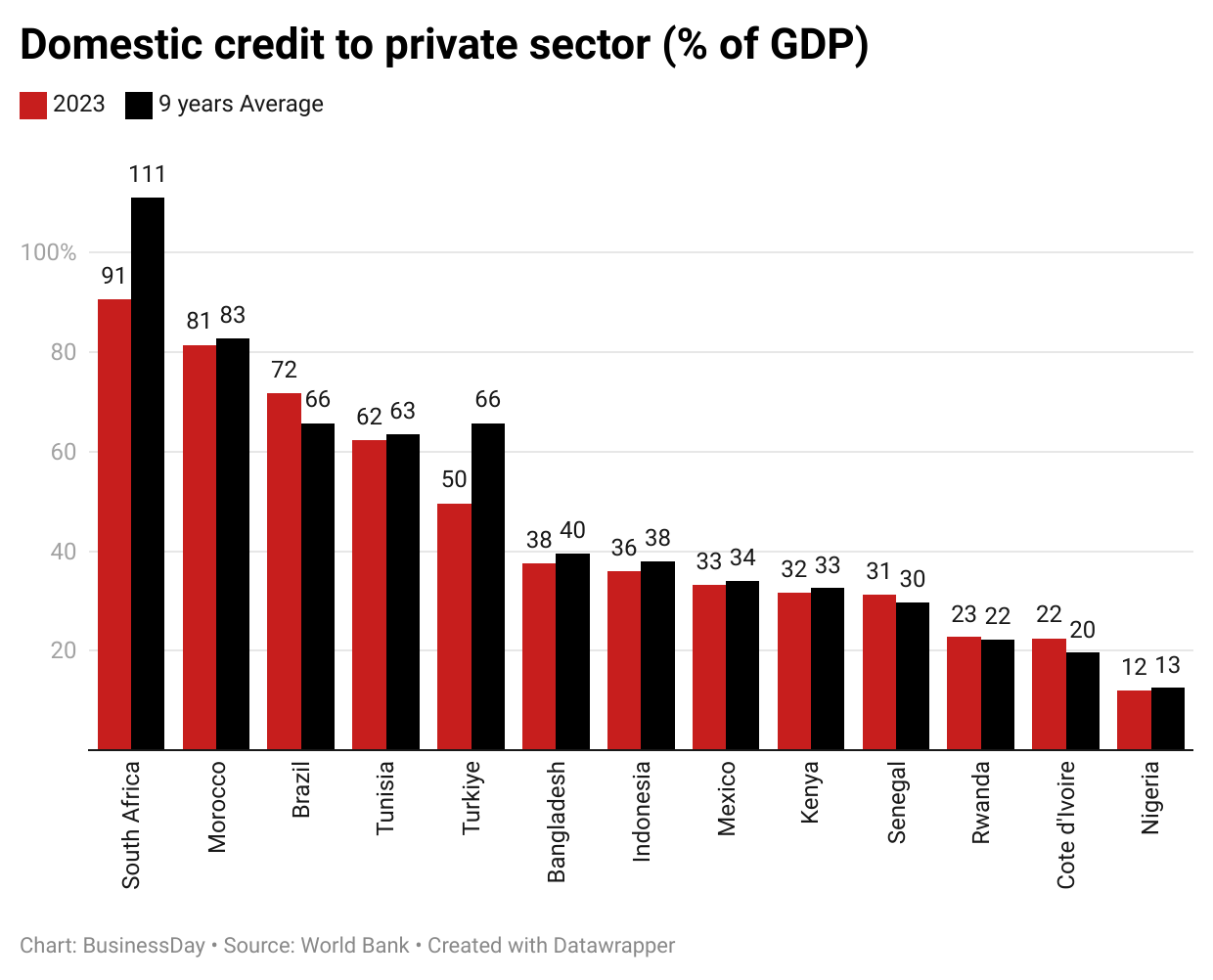

Nigeria’s domestic credit to the private sector stood at just 12 percent of GDP in 2023 — one of the lowest figures among major African economies, according to World Bank data. In 2024, the figure probably rose to 28.3 percent of GDP based on the estimations of analysts at FBN Quest.

In comparison, South Africa’s private sector credit penetration is 91 percent, while Kenya and Senegal recorded 32 percent and 31 percent respectively. Rwanda and Côte d’Ivoire also outperformed Nigeria, with ratios of 22 percent and 20 percent, respectively. Even among emerging economies outside Africa, countries such as Indonesia (36 percent) and Bangladesh (38 percent) maintain far stronger credit-to-GDP ratios than Nigeria.

This significant gap underscores Nigeria’s underdeveloped financial intermediation and the challenges facing efforts to deepen credit access in the economy. A combination of high interest rates which have moved from 18.50 percent in July 2023 to 27.50 percent in November 2024, tight liquidity conditions, and risk aversion among lenders continues to constrain credit growth, despite an expanding financial sector.

Nigeria’s Private Sector Access to Credit to GDP is one of the lowest, behind South Africa and Brazil according to the World Bank. Ndiame Diop, the World Bank Country Director for Nigeria, recently stressed the importance of expanding access to finance for private businesses. Speaking during the last Financial Inclusion Conference hosted by the CBN, Diop identified two critical priorities for Nigeria’s economic transformation: fostering the growth of labour-intensive, export-oriented sectors, and supporting micro and small enterprises with financing to scale into medium-sized firms. He specifically referenced private sector access to credit as a key barrier that must be addressed.

Yemisi Edun, Managing Director of First City Monument Bank (FCMB), similarly stressed the critical role of credit in boosting economic growth, particularly for small businesses speaking at the 17th Annual Banking and Finance Conference in Abuja. According to her, “In the country, SMEs, which play a major role in employment and economic growth, are struggling with limited access to credit.”

She noted that Nigeria’s private sector credit remains significantly low relative to GDP, and emphasized that improving access to finance is essential for sustainable development.

Lessons from peer economies

Experiences from higher-performing African economies offer valuable lessons. In South Africa, strong legal frameworks for collateral recovery, sophisticated credit bureaus, and a robust financial system have enabled banks to lend more confidently to the private sector. Kenya’s progress has been supported by mobile-based lending innovations and regulatory reforms aimed at expanding financial inclusion, particularly among small and medium-sized enterprises (SMEs). Additionally, the Central Bank of Kenya (CBN) recently benchmarked the Central Bank Rate (CBR) at 10 percent in April 2025.

Similarly, Morocco’s high private sector credit penetration — at over 80 percent of GDP — is linked to its diversified economy, sound monetary policy management, and deliberate efforts to strengthen its banking sector’s resilience. Morocco’s central bank, Bank al-Maghrib, cut the benchmark interest rate to 2.25 percent from 2.5 percent at its latest quarterly policy meeting in March 2025.

South Africa’s interest rate also stood at 7.50 percent.

The way forward for Nigeria

To close the credit gap, Nigeria would need to address several structural barriers. Strengthening the legal environment for loan recovery, expanding the reach and effectiveness of credit registries, and incentivising banks to lend to SMEs and underbanked sectors are crucial. Further, unlocking alternative lending channels such as fintech platforms and development finance institutions can help broaden access to credit.

While monetary policy tightening has contributed to price stability, a more balanced approach that supports real sector growth through improved credit access will be necessary to drive inclusive economic development. The current interest rate is not sustainable. One thing that is common among countries with high credit to GDP ratio is their low interest rate with an exception to Turkey.

As the fiscal space narrows and private sector investment becomes even more vital for growth, ensuring a well-functioning credit system will be key to Nigeria’s economic resilience.