The financial health of Nigeria’s downstream oil sector is coming under fresh scrutiny. Despite robust revenue growth across leading players, weak profit margins, rising debt levels, and declining liquidity suggest that the sector is facing sustained financial pressure—even if it’s not always headline-grabbing.

Growth without margin: An industry-wide concern

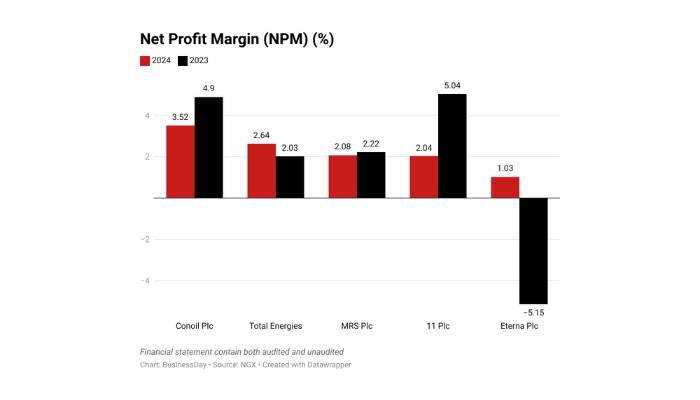

While firms like MRS Oil Nigeria Plc and Conoil Plc posted impressive top-line numbers in 2024—N312 billion and N323 billion respectively—profit margins across the board remain razor thin.

MRS’s net profit margin declined from 2.22 percent to 2.08 percent, and Conoil’s fell from 4.9 percent to 3.52 percent. Eterna Plc reported a slim 0.43 percent margin, while 11 Plc dropped from 5.04 percent to 2.04 percent. Total Energies held relatively steady at 2.67 percent, up from 2.03 percent.

This trend underscores a major industry issue: escalating costs are eroding profitability even as sales grow. For investors, the key takeaway is that revenue alone isn’t an indicator of financial health if companies can’t convert growth into sustainable profit.

Read also:¬ÝNigeria‚Äôs oil sector and the ‚ÄòVery Bad People‚Äô

Efficiency is slipping

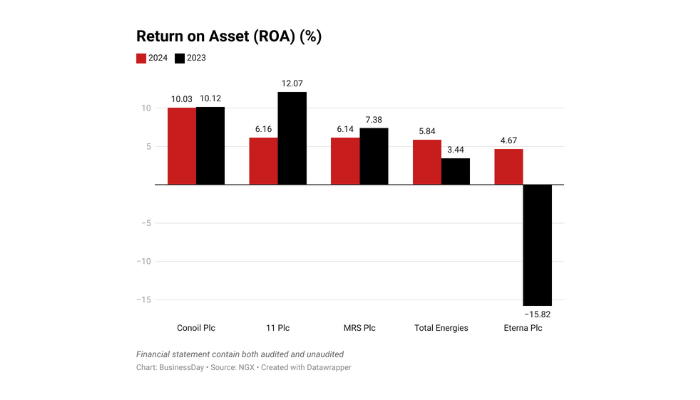

Declining returns on assets (ROA) show that many companies are struggling to use their resources efficiently. MRS, for example, saw its ROA drop from 7.38 percent to 6.14 percent, despite higher revenue. In contrast, Conoil maintained stronger operational efficiency with a double-digit ROA, showing that few players are effectively managing their growth.

Aggressive expansion—such as MRS’s recent acquisitions—hasn’t always translated to improved performance. In fact, such moves may be compounding short-term inefficiencies, especially in a tight-margin environment.

Debt levels rise across the board

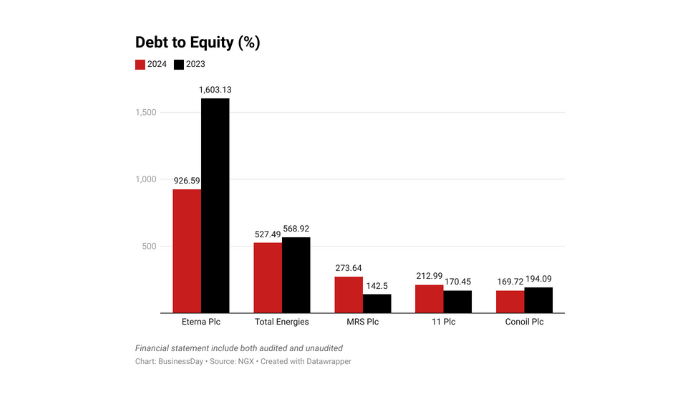

Rising leverage is another cause for concerns. MRS’s debt-to-equity ratio jumped from 142.50 percent to 273.64 percent in one year. Eterna’s is even more alarming at 926.59 percent, while Total Energies experiences a drop to 527.49 percent. Even Conoil, which reduced its ratio from 194.09 percent to 169.72 percent, remains heavily geared.

These numbers point to a growing reliance on debt financing. In a sector where margins are thin and cash flow is unpredictable, such debt levels introduce serious financial risk. Companies that fail to restructure liabilities or boost internal cash generation could find themselves in distress.

Liquidity pressures tighten

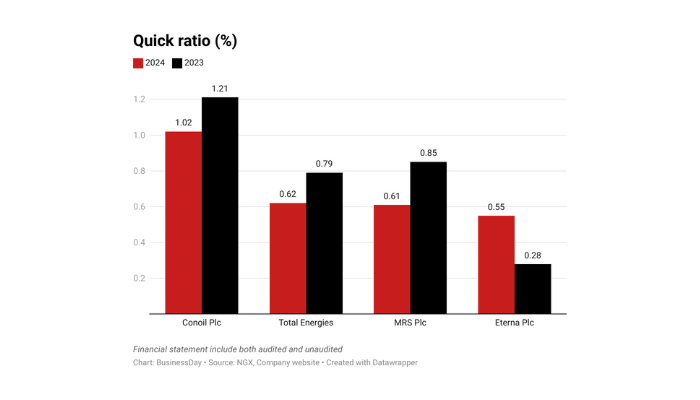

Most companies are also experiencing liquidity constraints. MRS’s quick ratio dropped from 0.85 to 0.61, while Total Energies and Conoil also saw declines. Eterna continues to operate with a weak ratio of 0.51, indicating a potential inability to meet short-term obligations without external support.

These liquidity strains suggest that more companies may soon be forced to either borrow more or liquidate assets just to stay afloat—a cycle that could intensify financial instability.

A legacy of regulation

An analyst points to the long-standing regulatory burdens in Nigeria’s downstream oil sector as a major contributor to the current financial strain.

While recent deregulation aimed to create more flexibility and improve margins, the expected benefits may take longer to materialise. In the meantime, companies continue to battle the hangover effects of years of suppressed pricing and limited operational autonomy.

Read also:¬ÝNigeria‚Äôs oil sector choked by bureaucracy

MRS’s delisting: A strategic shift, not a struggle

MRS Oil Nigeria Plc’s plan to delist from the Nigerian Exchange and transition to NASD OTC shouldn’t be mistaken for retreat. Despite strong 2024 earnings and 71 percent revenue growth, the company appears to be repositioning for greater flexibility and broader access to private capital.

With NASD OTC now housing big names and offering less rigid compliance burdens, MRS’s move may reflect a shift in how downstream oil players are navigating Nigeria’s tough business terrain—not a sign of weakness, but of strategy.

What investors should watch

The evolving story of Nigeria’s downstream sector holds lessons for market participants. First, revenue growth without margin expansion is often illusory.

Second, excessive leverage can quickly become unmanageable in low-margin environments. Third, structural reforms like deregulation take time—and patience—before their benefits are felt on corporate balance sheets.

As companies recalibrate in response to new realities, the real test will be who can maintain financial resilience while adapting to a more volatile and demanding landscape.