BusinessDay analysed the financial statements of the eight banks to have published their results for 2024 in order to uncover how each one is maximising shareholder value.

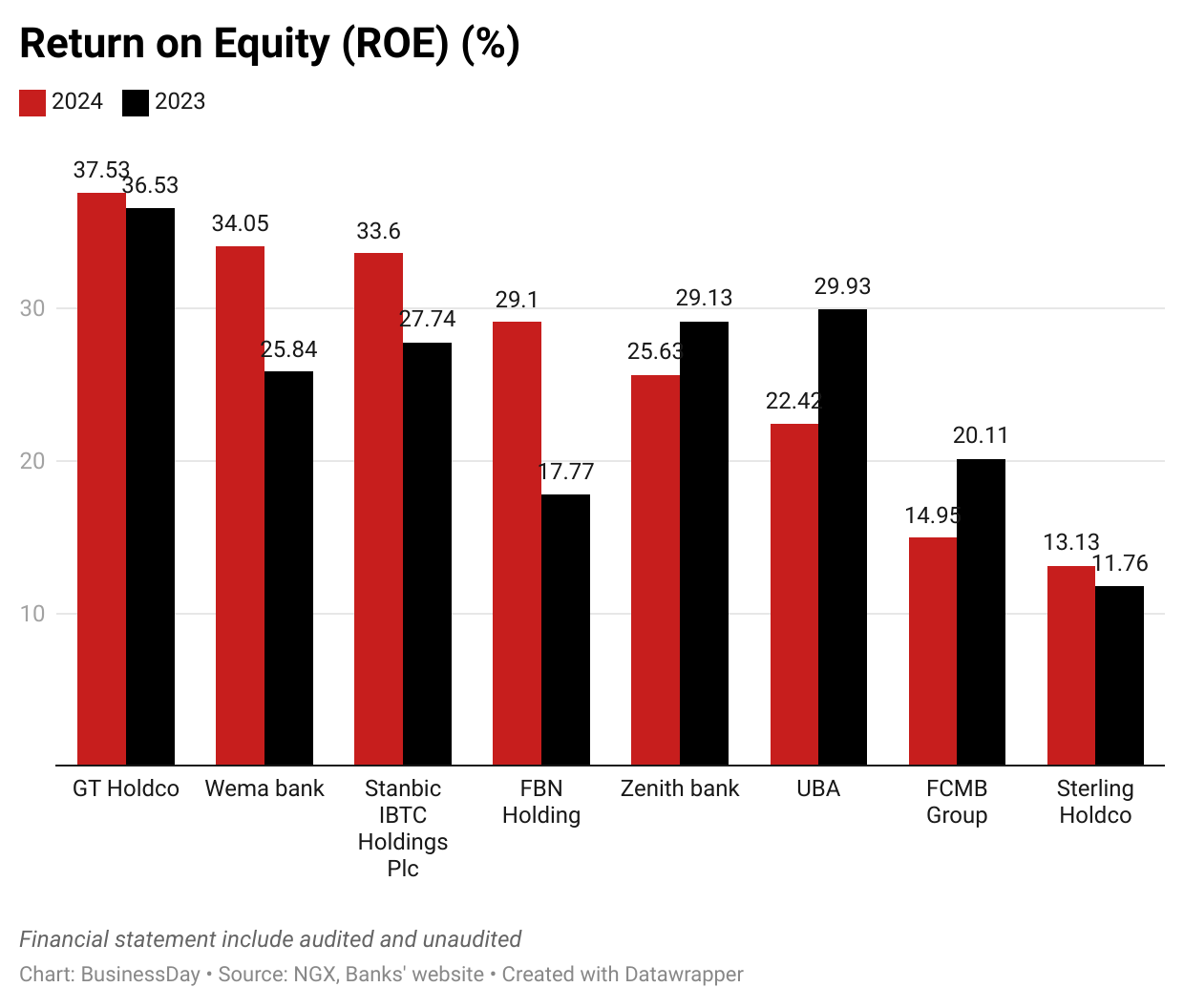

Return on equity

Of the eight banks that have released their financial statements for 2024, Guaranty Trust Holdco (GT Holdco) utilised shareholder funds better than anyone else with a 37.53 percent return on equity (ROE).

In the last two years (2023-2024), the same bank has given an ROE of 37.03 percent on average, followed closely by Stanbic IBTC with 30.67 percent.

This means that for every N100 of shareholders’ equity, GT Holdco generated N37.53 in net profit in 2024. This analogy applies to other banks’ ROE, highlighting the profitability of banking in Nigeria.

However, profitability is just one part of the picture. GT Holdco again recorded the highest return on assets (ROA) at 6.88 percent, followed by Zenith Bank (3.45 percent) and Stanbic IBTC (3.26 percent), indicating their ability to generate profit relative to their total assets. Meanwhile, banks with lower ROA, like Sterling Holdco (1.07 percent) and FCMB (1.53 percent), may be operating with lower efficiency or prioritising expansion and reinvestment over immediate profitability.

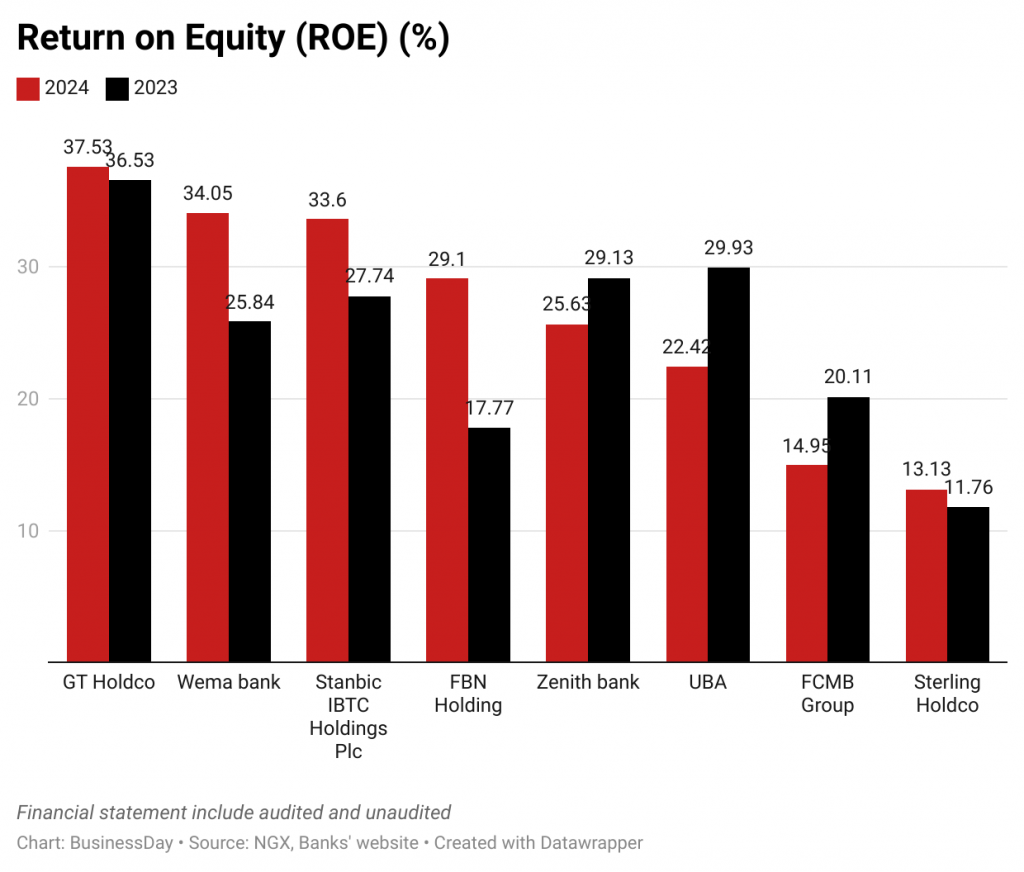

When it comes to efficiency in using assets to generate revenue, GT Holdco generated the most revenue per naira of assets, with an asset turnover ratio of 14.52 percent, ahead of Zenith Bank (13.26 percent), FBN Holdings (12.55 percent), and Stanbic IBTC (11.91 percent), meaning they generated more revenue per naira of assets. A higher asset turnover ratio signals strong operational efficiency.

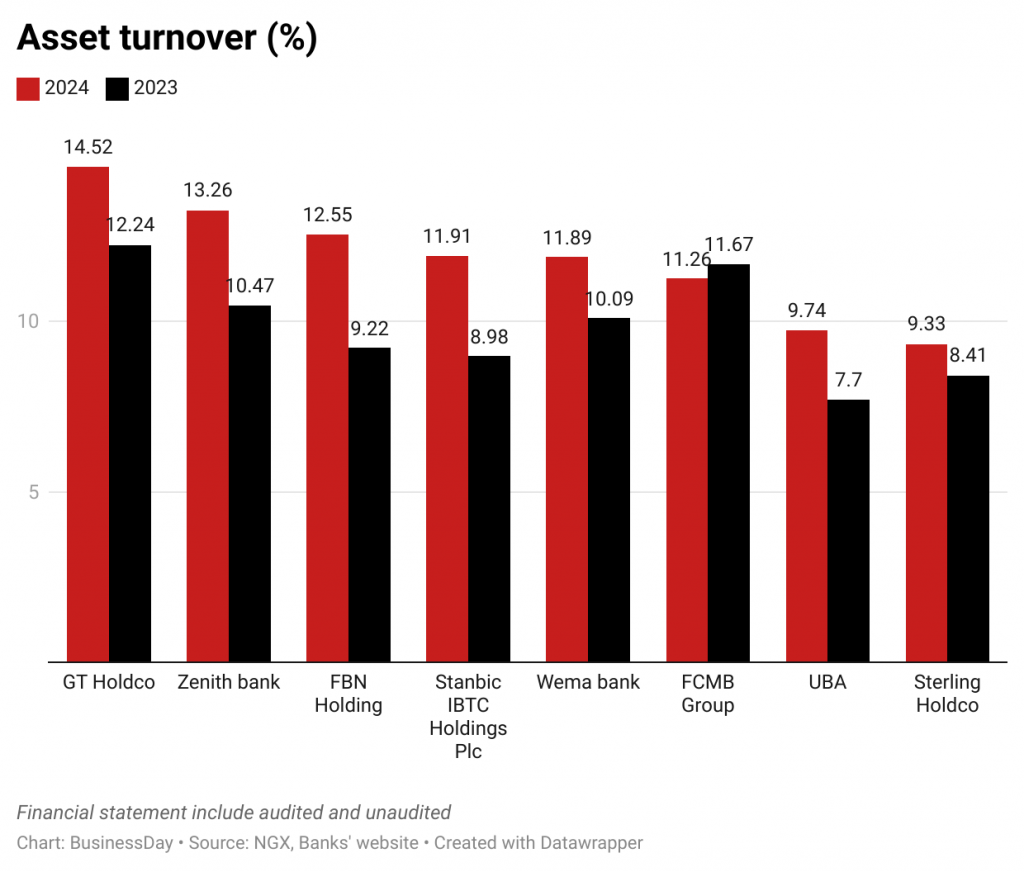

Profitability: How much Banks retain from revenue

While return on assets measures profitability relative to total assets, the net profit margin (NPM) shows how much of a bank’s revenue actually translates into profit. GT Holdco led with an impressive NPM of 47.8 percent in 2024, showing an improvement from 45.48 percent recorded in 2023. This is quite exceptional, especially when big lenders like Stanbic IBTC, Zenith Bank and UBA recorded declines from last year.

The decline in NPM across most banks suggests increased costs or strategic reinvestments. Meanwhile, Sterling Holdco (11.43 percent) and FCMB (13.58 percent) had lower margins, reinforcing their focus on reinvestment and expansion rather than immediate profitability.

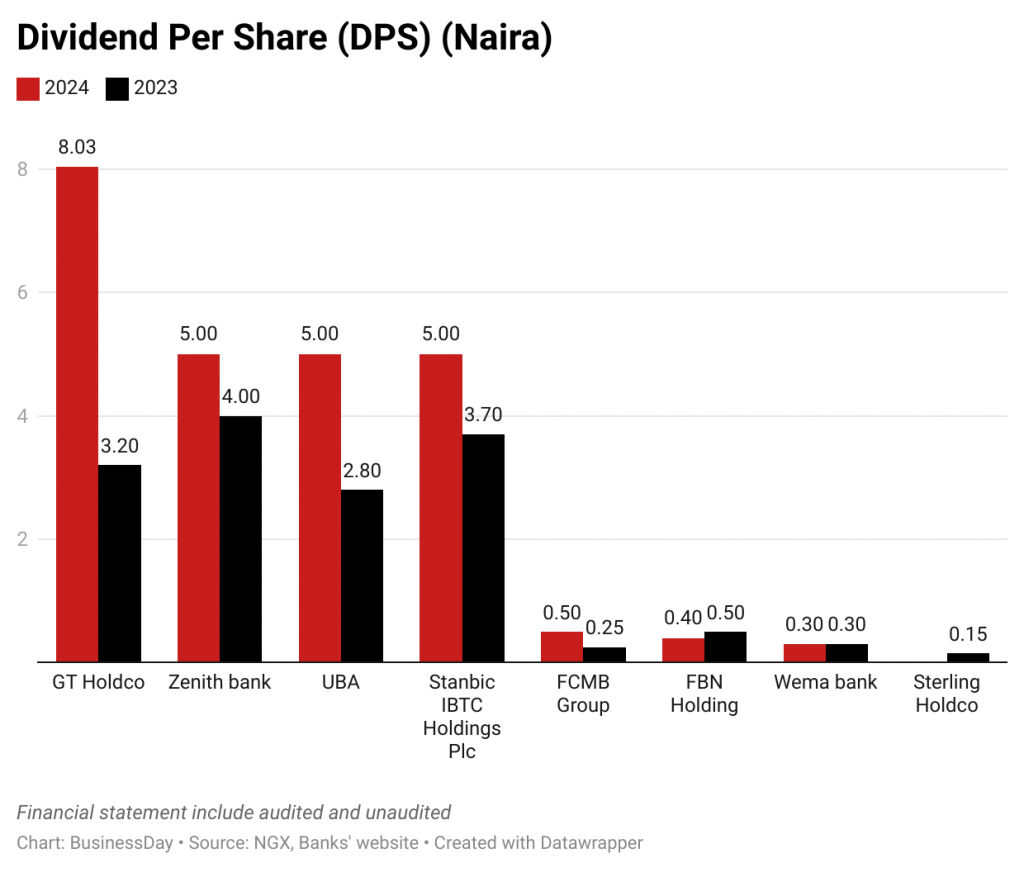

Dividend payouts: Rewarding shareholders

GT Holdco led the 2024 dividend payouts with N8.03 per share, demonstrating strong earnings and a commitment to rewarding shareholders. UBA, Stanbic IBTC and Zenith Bank followed with N5 per share each, maintaining a balance between profitability and payouts. In contrast, FBN Holdings, FCMB, and Wema Bank offered lower dividends at N0.40, N0.50, and N0.30 per share, respectively—likely reflecting a strategy of reinvesting earnings amid recapitalisation efforts. Sterling Holdco’s dividend per share was not available, suggesting either no declared payout or a strategic reinvestment approach.

For shareholders, the total dividend received depends on the number of shares held and the Dividend Per Share (DPS). For example, an investor with 100,000 shares in GT Holdco would receive N803,000 in dividends, while a 100,000-shareholder in FBN Holdings would get N40,000. The same principle applies across all banks: those with higher DPS deliver greater cash returns, while lower DPS banks may be prioritising long-term growth over immediate distributions.

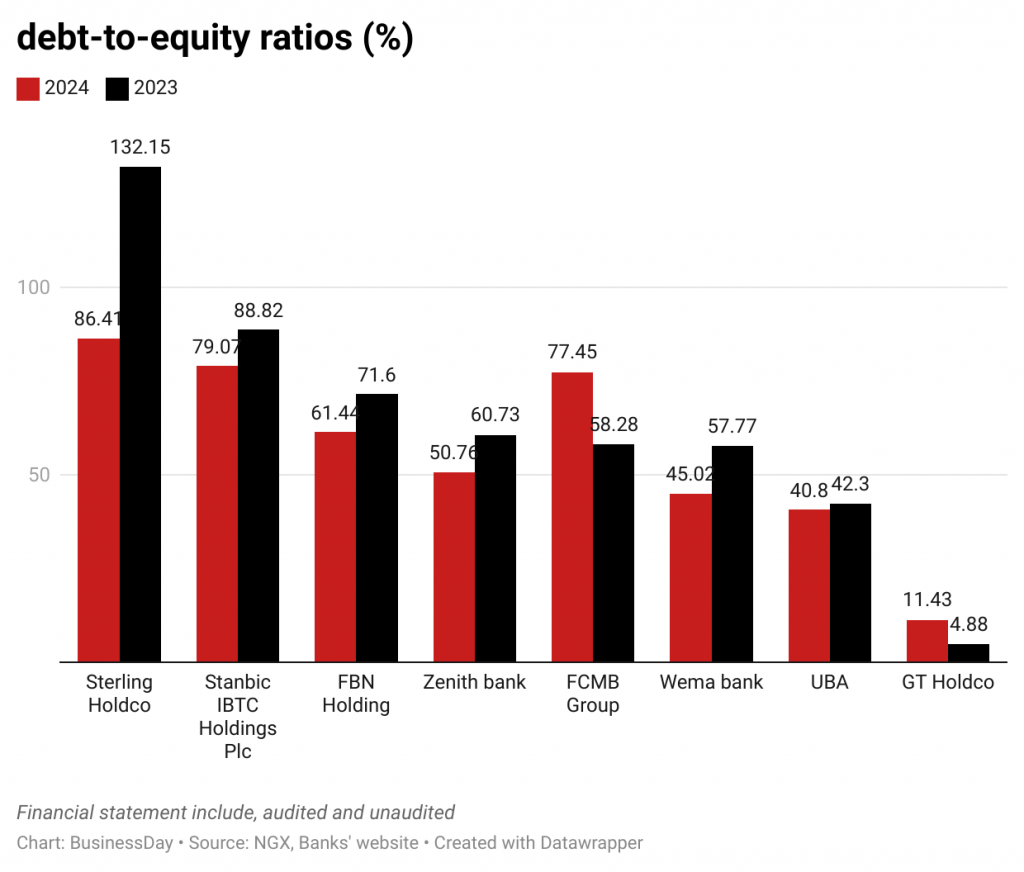

Debt and financial stability

While dividends and profitability attract attention, risk and stability are just as critical. Debt levels vary across banks, affecting financial flexibility. Zenith Bank and UBA had total borrowings of N2.04 trillion and N1.39 trillion, respectively. However, their debt-to-equity ratios of 50.76 percent and 40.80 percent suggest they are using debt strategically while keeping equity strong. This means they are leveraging external financing for growth without becoming excessively dependent on borrowed funds, maintaining a balance between risk and stability.

On the other hand, despite having lower total borrowings than Zenith and UBA, FCMB and Sterling Holdco carry higher debt-to-equity ratios, at 77.45 percent and 86.41 percent, respectively. Stanbic IBTC also has a significant debt-to-equity ratio of 79.07 percent, indicating a higher reliance on debt relative to their equity. This strategy can amplify returns but also increases financial risk, making stability a key factor for investors to consider.

A notable exception is GT Holdco, which has a significantly lower debt-to-equity ratio of 11.43 percent, reflecting its conservative use of leverage. While this suggests stronger financial stability, it may also indicate a more cautious growth strategy compared to peers.

Overall, while some banks strategically manage their debt-to-equity balance, others rely more heavily on borrowings, highlighting different risk profiles investors must evaluate.

Similarly, the interest coverage ratio, which measures how well banks can meet their interest obligations, varies significantly across institutions.

GT Holdco leads with an exceptional ratio of 447.10x, indicating its strong ability to cover interest expenses comfortably. Stanbic IBTC follows with a still impressive 194.73x, reinforcing its financial strength.

On the other hand, FCMB (29.61x) and Sterling Holdco (34.83x) have comparatively lower coverage ratios, suggesting they have less flexibility in managing interest expenses. Wema Bank’s ratio of 56.21x also places it in a moderate position.

While higher interest coverage ratios indicate stronger financial health and a lower risk of financial distress, banks with lower ratios may face more pressure if borrowing costs rise or profitability weakens.

Profitability vs. Risk

Nigerian banks have demonstrated resilience and strong earnings in 2024, but their strategies vary significantly.

GT Holdco stands out with an exceptional 47.38 percent net profit margin, significantly higher than its peers, reflecting both profitability and operational efficiency. Stanbic IBTC (27.37 percent), Zenith Bank (26.01 percent), and UBA (25.96 percent) have also maintained strong margins while balancing profitability with shareholder returns.

Meanwhile, Wema Bank (20.65 percent), FCMB (13.58 percent), and Sterling Holdco (11.43 percent) exhibit lower profitability levels, suggesting a greater emphasis on reinvestment and expansion rather than immediate shareholder rewards. Debt levels, asset efficiency, and interest coverage continue to be key determinants of long-term financial stability.

For investors, the choice between high-dividend banks and those prioritising growth depends on risk appetite and investment goals. Regardless, the 2024 financial reports affirm that Nigeria’s banking sector remains profitable and dynamic.