Cement is the backbone of Africa’s infrastructure and economic development, yet its price varies dramatically across the continent.

From Nigeria to Kenya, Egypt to South Africa, factors such as production capacity, import reliance, government policies, and currency fluctuations create a complex pricing landscape.

While some nations enjoy relatively stable and affordable cement prices, others grapple with soaring costs that hinder construction and housing projects. Understanding these price differences is crucial for investors, policymakers, and industry leaders seeking to drive sustainable growth and unlock Africa’s full infrastructure potential. But what really determines the cost of cement across Africa?

The African setting

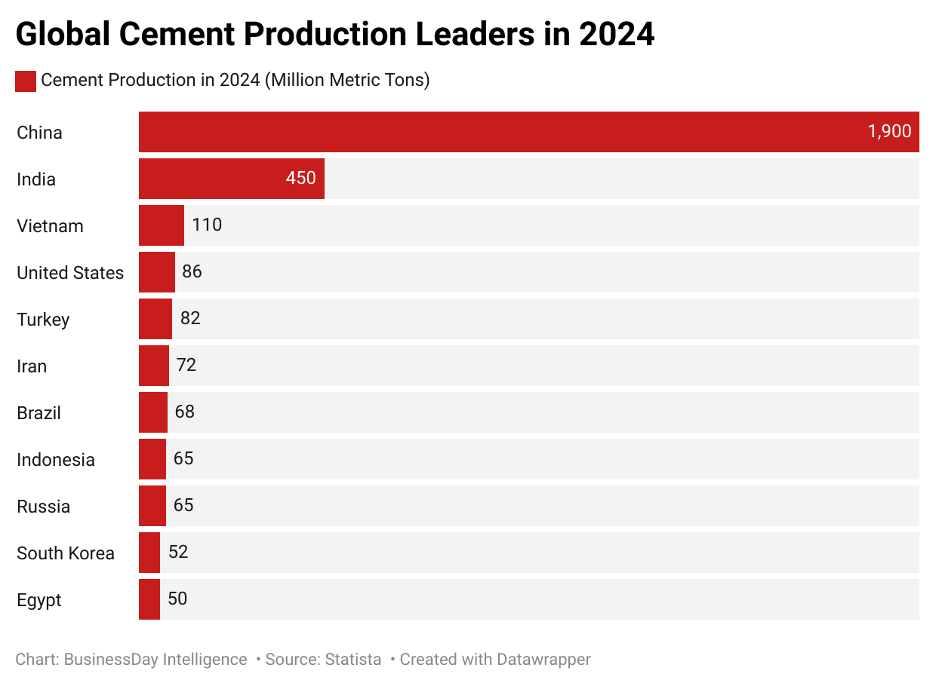

Nigeria’s cement sector reflects broader industry trends across Africa, where demand often outpaces production capacity, leading to higher cement prices compared to other developing regions. As of 2021, Africa’s cement industry had a total installed production capacity of 386.1 million tonnes per annum (Mt/a), accounting for just 5% of global cement production. However, actual output remains significantly lower due to challenges such as input shortages, foreign exchange constraints, equipment maintenance issues, and supply chain disruptions.

Despite these limitations, the sector is poised for growth. By 2025, Africa’s cement production is expected to reach 244.1 Mt/a, driven by urbanization, infrastructure expansion, and industrialization. The industry’s compound annual growth rate (CAGR) between 2020 and 2025 is projected to range from 2.6% to 2.9%, signaling steady expansion. Addressing production bottlenecks and enhancing local supply chains will be critical in closing the gap between installed capacity and actual output, ensuring the continent meets its growing cement demand.

The West African market

Nigeria has long established itself as a powerhouse in Africa’s industrial sector, with cement production standing as one of its most influential industries. Home to three of the continent’s largest cement producers—Dangote Cement, BUA Cement, and Lafarge Nigeria—the country plays a central role in meeting domestic demand while shaping regional markets. While these industry giants primarily supply Nigeria’s infrastructure and construction needs, Dangote Cement has expanded its reach across Africa, reinforcing the country’s position as a key player in the continental cement trade.

However, challenges persist. The West African cement industry has experienced significant price fluctuations, with Nigeria ranking among the countries with some of the highest cement prices globally. Despite being the largest cement producer in Sub-Saharan Africa, with a production capacity exceeding 58.9 million tonnes per year, it continues to experience significant price surges. Between 2021 and 2024, cement prices nearly doubled, reaching an unprecedented NGN 10,000 per 50-kilogram bag (US$6.46) by January 2025. This has critical implications for infrastructure development and housing affordability, making it a critical issue for investors and policymakers.

In recent years, Nigeria’s cement production capacity has grown significantly, exceeding 60 million metric tons per year (mt/y) as of 2023, making it the largest producer in Sub-Saharan Africa. Major manufacturers have invested heavily in expanding production facilities to meet rising domestic demand and explore export opportunities. Despite this progress, Nigeria still lags behind global industry leaders like China and India, which dominate the international cement market.

West Africa’s cement market: A complex interplay of economics, policy, and competition

The price of cement across West Africa is shaped by a delicate balance of economic conditions, government policies, and logistical challenges. While some countries benefit from localized production and state subsidies, others grapple with import dependencies, forex fluctuations, and high transportation costs, all of which push cement prices to record highs in certain markets.

One of the biggest cost drivers is currency fluctuation, particularly in nations like Ghana and Côte d’Ivoire, which rely heavily on imported cement and raw materials. As local currencies depreciate, the cost of importing clinker, gypsum, and fuel rises, making cement more expensive. Nigeria’s cement industry has not been spared from these challenges. In the first quarter of 2024, leading cement manufacturers—Dangote Cement, BUA Cement, and Lafarge Africa—reported substantial forex-related losses. Lafarge Africa, for instance, recorded a ₦21.8 billion forex loss, a stark contrast to the ₦320 million gain in the same period the previous year. Dangote Cement was hit even harder, with losses soaring from ₦9.79 billion in Q1 2023 to ₦63.77 billion in Q1 2024, primarily due to rising costs of sourcing natural gas and other dollar-priced inputs.

Beyond forex challenges, government policies significantly influence pricing. Some nations, like Niger and Senegal, have introduced tax exemptions and subsidies to make cement more affordable, boosting construction activity in the process. Conversely, Nigeria’s import restrictions, designed to protect local manufacturers, have inadvertently driven higher prices by limiting supply. Taxation has also become a major burden. According to the Federal Inland Revenue Service (FIRS), the cement industry’s tax contributions have surpassed those of all commercial banks combined, with Dangote Cement alone remitting ₦412.9 billion over the past three years.

Infrastructure and logistics also play a crucial role in cement price disparities across the region. Landlocked countries like Mali and Burkina Faso face higher prices due to costly transportation expenses, while coastal nations with access to ports and domestic production facilities enjoy relatively lower prices. In addition, poor road networks and inefficient distribution systems make cement significantly more expensive in rural and remote areas, restricting access to affordable building materials.

Cement prices also tend to fluctuate seasonally, rising during the dry season when construction activity peaks and falling during the wet season when demand slows. However, economic disruptions and supply chain issues can override these seasonal patterns, leading to unexpected price surges that impact housing affordability and infrastructure development.

Historically, West Africa’s cement sector has operated under a tacit price arrangement, where government policies—including tax incentives and import bans—protected local producers. While this approach fostered a strong domestic manufacturing base, it also limited competition and kept prices artificially high. This landscape began shifting in October 2023, when BUA Cement made a bold move, slashing its ex-factory price to ₦3,500 per bag in anticipation of new plant completions. This aggressive pricing strategy forced a market-wide adjustment, with cement prices dropping from ₦10,000-₦15,000 per bag to an average of ₦7,000-₦8,000 per bag. The result? BUA’s market share surged by 9.4% to 20.6% in just a few months.

Looking ahead, the West African cement industry remains at a crossroads. Addressing forex instability, taxation burdens, energy costs, and supply chain inefficiencies will be key to ensuring a sustainable, competitive, and affordable cement market for both investors and consumers. The region’s continued urbanization and infrastructure growth mean that cement demand will only increase, making long-term pricing strategies and investment in production capacity more critical than ever.

Building a sustainable and competitive cement industry in West Africa

West Africa’s cement industry faces rising production costs, logistical inefficiencies, and market instability. However, targeted reforms can enhance efficiency, reduce costs, and ensure a stable cement supply.

High energy costs remain a major challenge, with innovations like carbon capture, geopolymer concrete, and cementless concrete in advanced economies reducing energy consumption. West African manufacturers must adopt similar technologies to remain competitive. Poor transportation infrastructure further inflates costs, especially in landlocked countries. Investing in better road and rail networks—as seen in China’s Belt and Road Initiative—can significantly reduce logistics expenses.

Government policies also impact pricing. In Nigeria, cement manufacturers paid more in taxes than commercial banks, with Dangote Cement alone remitting ₦412.9 billion in three years. A tax review could ease production costs, making cement more affordable. Unregulated pricing allows market manipulation, unlike India and the Philippines, where price monitoring ensures fairness.

Diversifying construction materials can also ease demand. Local alternatives like pozzolana have reduced costs in Kenya and Turkey, lessening reliance on imported clinker. Finally, regional trade cooperation under AfCFTA could stabilize supply and pricing. By embracing these reforms, West Africa can build a competitive, efficient, and sustainable cement industry that supports infrastructure growth.

Future market trends

Industry experts predict that cement prices in West Africa will continue to be influenced by economic policies, energy costs, and production capacity expansion. The demand for cement is expected to grow as urbanization and infrastructure projects increase. In response, governments and manufacturers must work towards a sustainable pricing model that balances affordability and profitability.

Looking ahead, Nigeria’s cement industry remains a key driver of economic diversification and industrialisation. With continued investments, rising urbanisation, and expanding export potential, the sector is poised for sustained growth. Addressing market challenges while leveraging emerging opportunities will be crucial in ensuring Nigeria solidifies its position as a leader in Africa’s cement production and infrastructure development.