ŌĆ”As data show CBNŌĆÖs reduced intervention in FX market

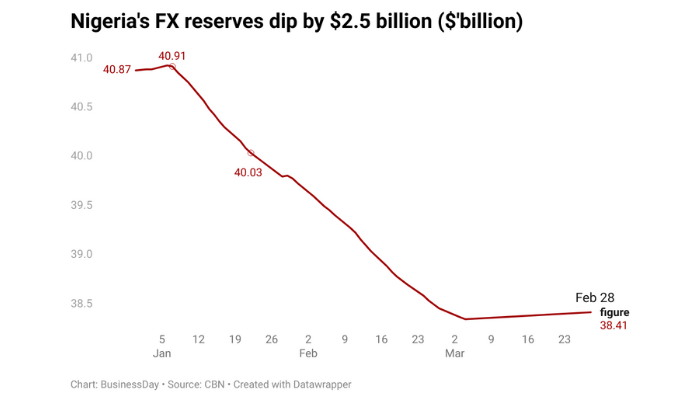

A sharp decline in NigeriaŌĆÖs external reserves to a six-month low has dominated financial headlines in recent days, stoking fears of renewed instability in the naira and a potential pullback by investors.

Yet, a closer examination of data and policy direction suggests that these concerns may be misplaced.

The Central Bank Governor Olayemi Cardoso had forewarned investors about the expected dip in reserves during a meeting last year, citing planned foreign exchange obligations in the first quarter (Q1) of 2025. This transparency, rare in previous administrations, aimed to ensure investor confidence remained intact despite short-term fluctuations.

Read also:┬ĀCBNŌĆÖs reforms put Nigeria on spotlight for investors

Predicted decline, not unexpected shock

Zeal Akaraiwe, CEO of Graeme Blaque Advisory, confirmed that the CBN had projected a reservesŌĆÖ decline in Q1. ŌĆ£In an investorsŌĆÖ meeting last year, Yemi Cardoso, governor of the apex bank, had informed in advance that it would be financing debt repayments and other standard financial obligations in Q1, which would lead to a decline in foreign exchange (FX) reserves, rather than efforts to defend the naira,ŌĆØ he stated.

Prior to this year, NigeriaŌĆÖs reserves had been on a steady climb. Between January and December 2024, the countryŌĆÖs external reserves swelled from $32.6 billion to $40 billion, an increase of nearly $8 billion. This was largely attributed to the liberalisation of the foreign exchange market in 2023, which enabled autonomous inflows to become the primary source of FX supply, reducing the CBNŌĆÖs role in active market interventions.

Even during periods of significant naira depreciation last year, the central bank opted to prioritise reserves accumulation over currency defense, breaking away from past interventionist policies.

Shifting market dynamics: Rise of autonomous inflows

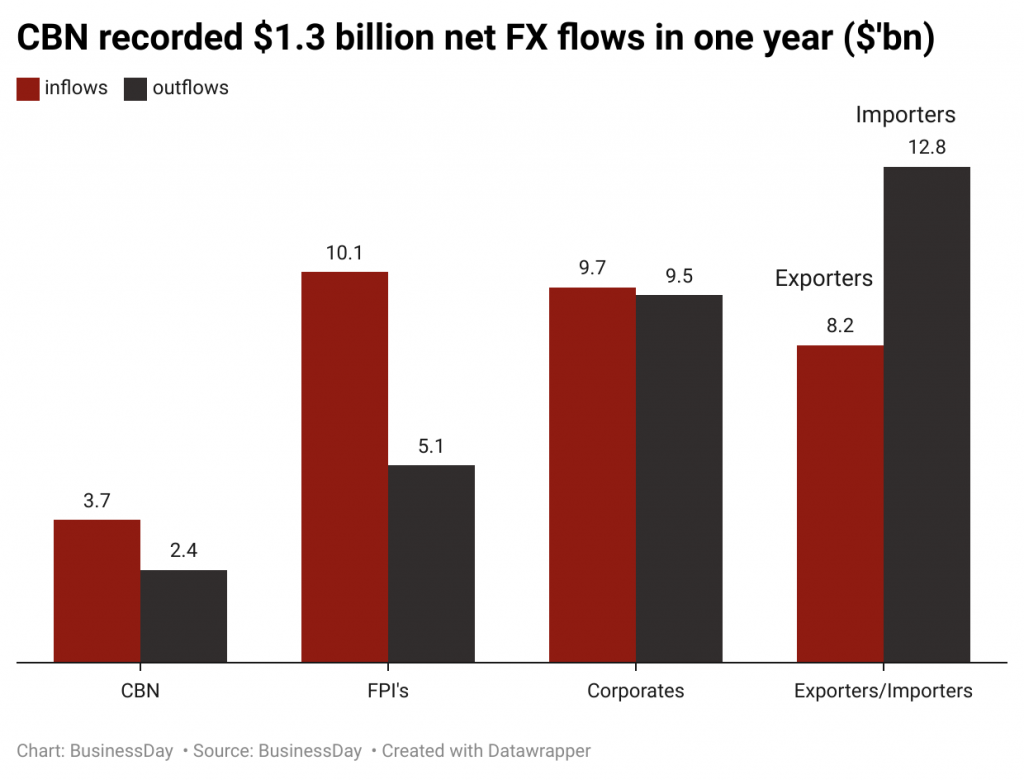

Official data illustrate the CBNŌĆÖs diminishing influence in the FX market, as foreign portfolio investors and diaspora remittances increasingly drive dollar inflows.

Total FX inflows into NigeriaŌĆÖs economy fell to $8.4 billion in November 2024, down from $9.2 billion in October. However, inflows via the CBN saw a steeper decline of 35 percent, falling to $2.9 billion over the period, according to the CBN data.

This sharp drop in central bank-driven inflows underscores the CBNŌĆÖs deliberate strategy to allow the market to dictate the nairaŌĆÖs value through price discovery.

Meanwhile, autonomous inflows, which accounted for about 65 percent of total FX receipts, rose from $4.7 billion in October to $5.5 billion in November.

ŌĆ£The increasing allocation of FX through autonomous sources can be attributed to the CBNŌĆÖs supportive measures to bolster market liquidity,ŌĆØ analysts at FBNQuest Merchant Bank said in a research note to clients.

Cardinal Stone analysts similarly downplayed concerns over declining reserves, attributing the trend to external debt servicing, including the repayment of the International Monetary FundŌĆÖs (IMF) $3.4 billion COVID-19 emergency loan under the Rapid Financing Instrument (RFI).

The IMF had extended the financial lifeline to Nigeria in 2020 amid the pandemic-induced economic downturn and plunging oil prices. The repayment schedule, which began in 2023, is expected to be completed this year.

Read also:┬ĀInvite firms with unresolved $2.4bn FX contracts, Muda Yusuf urges CBN

By the end of February 2025, NigeriaŌĆÖs reserves had shed $2.42 billion, settling at $38.45 billion, according to data tracked by BusinessDay. Despite this, sources close to the CBN remain confident that reserves accretion will resume in the second quarter (Q2), supported by increased market transparency and a projected rise in remittance inflows to $1 billion per month.

Restoring investor confidence: The CBNŌĆÖs strategic overhaul

The Cardoso-led CBN has made clear its intent to undo the distortions left by the tenure of former governor Godwin Emefiele. Beyond liberalising the FX market and limiting direct interventions, the apex bank is seeking to restore investor confidence through orthodox monetary policies.

ŌĆ£Confidence is indeed returning; thereŌĆÖs no more frontloading of a yearŌĆÖs supply of forex because of BMatch transparency,ŌĆØ said a source familiar with the CBN operations. ŌĆ£But things can roll back if the direction of travel isnŌĆÖt maintained, which could overturn all the gains made.ŌĆØ

The Bloomberg BMatch system, introduced for FX trading on December 2, 2024, has played a key role in stabilising the naira by enhancing transparency and operational efficiency. Since its implementation, the currency has appreciated by over 10 percent, supported by improved market confidence.

Weaker Naira, stronger economy?

President Bola TinubuŌĆÖs bold move to allow a more than 100 percent devaluation of the nairaŌĆöfalling from N460/$ before the 2023 elections to around N1,500/$ŌĆöhas, in the eyes of many economists, restored NigeriaŌĆÖs competitiveness.

The devaluation, long considered overdue, has led to a significant improvement in the countryŌĆÖs balance of payments. The current account, a broad measure of trade performance, has returned to a firm surplus. Capital inflows, albeit heavily driven by portfolio investments, have started re-entering the Nigerian economy.

Crucially, the weaker naira has also provided a much-needed boost to government revenue. The fiscal windfall has helped narrow NigeriaŌĆÖs budget deficit from 6.4 percent of the gross domestic product (GDP) in early 2023 to 4.4 percent in early 2024, alleviating fiscal pressure.

While fears over NigeriaŌĆÖs reserves depletion persist, the broader economic picture suggests that the country is in a far stronger position than critics acknowledge.

Read also:┬ĀHow CBN is reinforcing oversight to strengthen financial system

The CBNŌĆÖs decision to prioritise market stability over direct intervention appears to be yielding results, with investors responding positively to improved transparency and liquidity.

However, analysts polled in a BusinessDay survey say maintaining policy consistency will be critical.

ŌĆ£Underlying NigeriaŌĆÖs history of failed exchange rate devaluations is its policymakersŌĆÖ consistent unwillingness to keep the exchange rate competitive in the period after each devaluation,ŌĆØ said David Lubin, former managing director and head of emerging markets economics at Citibank.

ŌĆ£Time now to end that pattern and resist the temptation to let the currency strengthen excessively. The path to a more capital-rich, more diverse Nigerian economy can only be built on a competitive naira,ŌĆØ Lubin said.