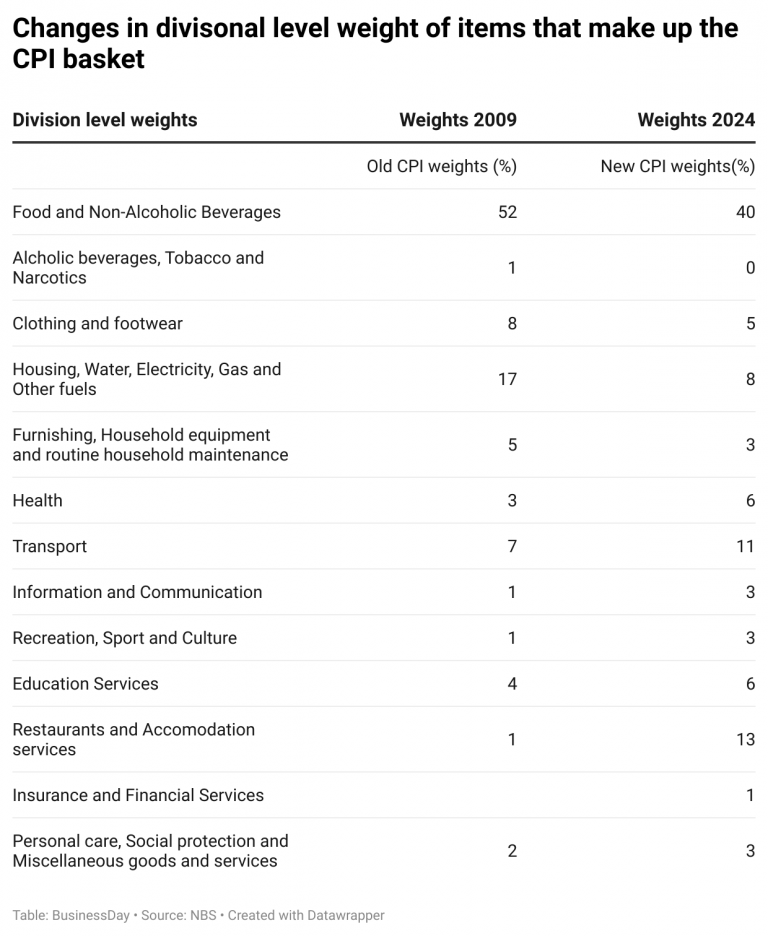

With the recent reshuffling of the inflation basket, the combined influence of food, non-alcoholic beverages, housing, electricity, gas, and other fuels has been suppressed by 72.29 percent, effectively diminishing their impact on inflation.

Nigerians have been awaiting the release of repackaged GDP and inflation figures—data the National Bureau of Statistics (NBS) has been meticulously refining for over a year.

Initially scheduled for publication on 31 January 2025, the figures remain under wraps. The NBS, it seems, is still fine-tuning its numbers.

An anonymous source has suggested that while the GDP’s output-based valuation is ready, delays stem from finalising the expenditure approach—an integral part of the rebasing exercise. Meanwhile, concerns are mounting over how these new figures will be interpreted. A recent BusinessDay report underscored fears that key indicators, such as tax-to-GDP and debt-to-GDP ratios, could be misinterpreted.

The Financial Derivatives Company (FDC), in its February 2025 Lagos Business School (LBS) breakfast session, went a step further, raising questions about data integrity and reputational risk. There is growing scepticism over the consistency of data across sectors, the transparency of the adopted methodology, and whether the final output will truly reflect Nigeria’s economic realities.

Read also: Rebased inflation rate stokes interest rate uncertainty

A question of methodology

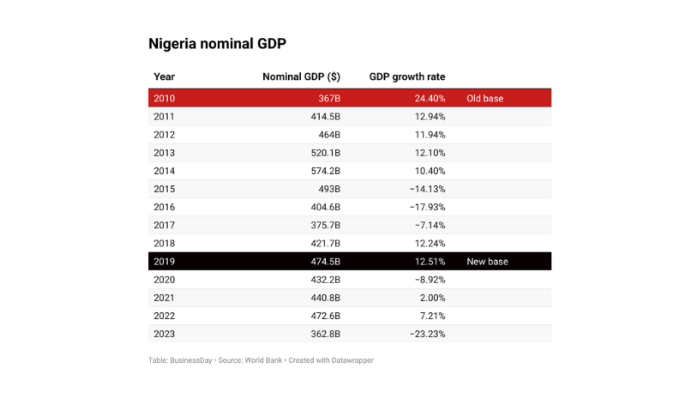

Rebasing GDP requires selecting a new base year, ideally the most stable year after the previous benchmark. A review of Nigeria’s nominal GDP from 2010 to 2023 reveals that growth was strongest in 2010—one of the reasons it was chosen as the base year for the 2014 rebasing. According to an in-house economist, “The best-performing year is typically selected as the new base for GDP, while the worst-performing year is used for CPI.” This explains why 2024 has been designated as the new base year for CPI.

The NBS has reiterated that the rebasing exercise draws from multiple sources, including the Nigerian Living Standards Survey (2019-2023), the National Business Sample Census (2021), and the National Agricultural Sample Census (2020). These datasets provide crucial insights into household expenditure, business activity, and agricultural output. The Bureau insists that the methodology aligns with international standards.

Yet doubts persist. On the CPI rebasing, experts have voiced concerns about the accuracy of the inflation basket’s composition, the weighting of items, and the credibility of data collection methods. Political and institutional interests also loom large. The government is committed to expanding Nigeria’s economy to $1 trillion by 2030 and achieving 15 percent inflation by 2025—ambitious targets that some fear may have influenced the statistical exercise.

Since President Bola Tinubu’s administration assumed office in May 2023, Nigeria’s unemployment rate has plummeted from 33 percent to around 4 percent—a decline so dramatic that many question the methodology behind it.

If unemployment figures can be recalibrated so swiftly, might inflation data be similarly adjusted to align with political objectives rather than economic reality?

The inflation conundrum

Taiwo Oyedele, Chairman of the Presidential Fiscal Policy and Tax Reforms Committee, has provided a compelling argument for why 15 percent inflation is attainable. “If you look at 2024, inflation was 33 percent. If things remain as bad as they were in 2024, in 2025, nominally, inflation will be 25 percent. Why? That’s the base effect,” Oyedele explained.

“You had 100, the price went up by 33, now it became 133. When you do year-on-year, you’re comparing the next one with the 133. So, 33 over 133 is 25. If 2025 is as bad as last year, we’ll have 25. But if you look at what pushed inflation in 2024, the biggest factor by a mile was the exchange rate pass-through. We moved from N900 to N1,600, at some point hitting N1,800 or N1,900. Nigeria is one of the most resilient countries in the world. We should not be talking about 34 percent at the end of December. We took that shock of exchange rate pass-through along with the one on PMS (petrol subsidy removal), which was not just about PMS alone, but other cost pressures as well.”

Yet the rebasing exercise complicates this projection. Without CPI rebasing, the inflation rate would have naturally declined to 25 percent due to the base effect. However, the recalibrated inflation basket now carries different weights, meaning inflation will no longer behave as it did under the old model.

Read also: Nigeria’s inflation drops to 24.48% in January after rebasing

The politics of the inflation basket

Under the new methodology, the weight of food in the inflation basket has been slashed from 51.8 percent to 40.1 percent. At the same time, other components such as health, transport, and education have seen their influence increase. This shift is significant. Food accounts for 57 percent of household consumption, yet its statistical weight has been diminished, muting its impact on the inflation rate.

A simple illustration underscores the effect: food’s influence on inflation has been reduced by 22.59 percent. Future spikes in food prices will therefore exert less upward pressure on inflation figures than before.

Likewise, the combined weight of housing, water, electricity, gas, and other fuels—essentials for most households—has been cut from 16.7 percent to 8.4 percent, a 49.7 percent reduction.

Taken together, the influence of food, non-alcoholic beverages, housing, electricity, gas, and other fuels has been suppressed by 72.29 percent. Effectively, this adjustment tames inflation statistically—even if household budgets tell a different story. It is akin to muzzling a guard dog to stop it from barking, without addressing the intruder at the gate.

The NBS has justified these changes by citing the substitution effect and evolving income dynamics—a standard rationale in inflation calculations. Yet, historical data suggests that not all countries that rebased their CPI saw inflation decline. Uganda, for instance, experienced an increase from 2.3 percent to 2.71 percent after shifting its CPI base year from 2009 to 2021. Kenya and Nigeria have had similar experiences in past rebasing exercises.

Data integrity and the benefit of doubt

Data integrity is always a contentious issue in large-scale economic measurements. Statistical agencies operate under immense pressure, navigating political expectations, methodological challenges, and the limitations of available data. The NBS insists that its numbers are rigorously compiled and internationally benchmarked.

Yet for businesses, investors, and ordinary Nigerians, the real test will be whether the rebased GDP and CPI figures align with the lived economic experience. A statistical decline in inflation is unlikely to convince consumers facing persistently high food and energy costs. Similarly, a larger GDP may not translate to a more prosperous economy if the underlying growth drivers remain weak.

For now, the Bureau deserves the benefit of the doubt—but trust, once strained, is difficult to restore.