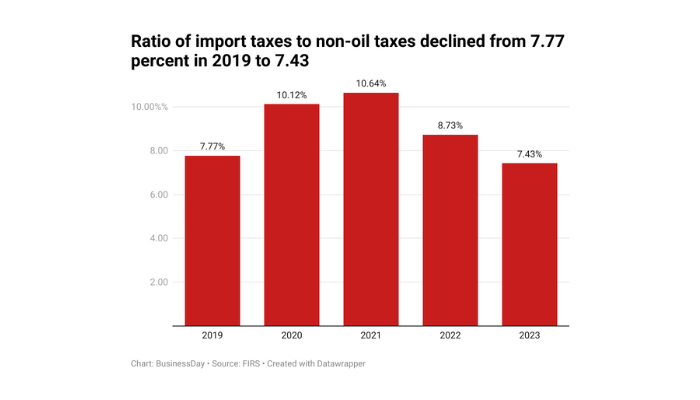

Despite the Nigerian Customs Service (NCS) installing container scanners in 2022, data from the Federal Inland Revenue Service (FIRS) reveal a concerning trend: the ratio of import taxes to non-oil taxes declined from 7.77 percent in 2019 to 7.43 percent in 2023. While ongoing tax reforms are commendable, the government must address additional challenges to achieve its projected revenue targets by 2025.

A report by Financial Derivatives Company (FDC) Prism, published on 31 December 2024, highlights that the scanners, designed to inspect 400 containers daily, have not significantly boosted import tax revenue.

Paradoxically, the NCS has consistently surpassed its revenue targets over the past four years (2021–2024). Yet, the import and non-oil taxes ratio has declined since the scanners were installed.

“Multinational corporations, for instance, often reduce their tax liabilities through transfer pricing—a practice where goods, services, or intangible assets are priced strategically between related entities within the same corporate group.”

In 2024, the NCS collected a record N6 trillion, driven largely by naira depreciation and higher foreign exchange (FX) rates for clearing goods at ports. Similarly, the FIRS exceeded its 2024 target by 76 percent, collecting N21.6 trillion, primarily from non-oil taxes buoyed by exchange rate fluctuations and inflation. However, these achievements mask a deeper issue: subtle tax evasion, particularly at the borders.

Understanding transfer pricing and its role in tax evasion

Tax evasion remains one of the most effective tools for cheating the government, and border taxes are no exception. Multinational corporations, for instance, often reduce their tax liabilities through transfer pricing—a practice where goods, services, or intangible assets are priced strategically between related entities within the same corporate group. While transfer pricing is a legitimate business practice, it can be manipulated for tax evasion or profit shifting.

For instance, imagine a global toy manufacturer, Sunny Toys, with two subsidiaries:

Sunny Toys USA—based in the United States, where corporate taxes are high.

Sunny Toys Nigeria—located in a tax haven with minimal corporate taxes.

Here’s how the scheme works:

Production: Sunny Toys USA designs and manufactures toys, incurring significant costs on materials, labour, and machinery.

Manipulated Sales: Instead of selling directly to retailers, Sunny Toys USA “sells” the toys to Sunny Toys Nigeria at an artificially low price—say $1 per toy instead of $10.

Profit Shifting: Sunny Toys Nigeria then sells the toys at the actual market price of $10 per unit. Since most of the profits are recorded in the low-tax country, Sunny Toys USA reports low profits and thus pays lower taxes in the US. At the end, Nigeria’s subsidiary will rake in huge profit while the parent U.S. is minimising tax liabilities.

Though not identical, similar strategies can be deployed to evade import taxes at borders. For instance, a container worth $10 million might be declared at just $4 million, reducing the tax liability significantly. If the government charges 1 percent on the value of imported goods, this under-declaration will result in $40,000 instead of $100,000 in revenue—a substantial loss.

Multinationals are not without their challenges with tax officials.

Multinational companies operating in Nigeria face significant challenges when dealing with the Federal Inland Revenue Service (FIRS), particularly regarding withholding tax credits. A head of treasury in a multinational company anonymously shared his experience of how FIRS officials deliberately withheld access to tax credits, demanding illicit payments before allowing companies to use their rightful funds.

When a company sells goods or services, clients typically deduct 10 percent of the invoice as withholding tax and remit it to the FIRS on the company’s behalf. However, “despite these deductions, FIRS often fails to allocate the amounts to the company’s tax profile,” Anonymous said. When companies attempt to offset their tax liabilities using the accumulated withholding tax credits, they are met with resistance.

He cited, for instance, if one’s company has about $2 million in withholding tax credits. Instead of allowing the company to apply the credit toward its tax obligations, the FIRS official in charge may sometimes demand a 5 or 10 percent cash bribe before processing the reconciliation.

If the company refused to comply, the tax assessment continued to accrue interest, forcing them to negotiate unofficial payments or struggle to raise additional cash to cover their tax bill.

Even when the company successfully recovers their funds, “FIRS often applies outdated exchange rates, significantly devaluing the amounts owed in foreign currency.”. For instance, some companies have had their dollar-denominated tax credits converted to naira at rates as low as N305 per dollar, even when the prevailing exchange rate had risen to over N1,000 per dollar.

These practices put undue financial pressure on businesses, forcing them to borrow money to meet tax obligations that should have been covered by their existing tax credits. In many cases, reconciliation efforts drag on for years without resolution, and companies are left with no option but to pursue legal action or unofficial settlements.

Although the current tax reform bill is already in place to take care of this menace if approved and implemented.

Uganda’s Experience with cargo scanners

The case of Uganda illustrates this challenge. In 2018, the Uganda Revenue Authority installed non-intrusive cargo scanners at key border points to combat tax evasion. While the scanners reduced undercounting and misclassification of goods, they inadvertently gave rise to a new form of evasion: “underpricing.” Larger firms, particularly multinationals, adapted by undervaluing imports, leading to a 7.7 percent drop in taxed imports and a 9.8 percent decline in tax receipts.

It appears Nigeria might be facing a similar predicament. Since the installation of scanners in 2022, the ratio of import taxes to non-oil taxes has declined from 8.73 percent to 7.43 percent in 2023. While the FIRS’s record of N21.6 trillion revenue in 2024 is impressive, a detailed breakdown of this figure is needed to assess the true impact of border tax receipts (NCS VAT).

Policy recommendation

To address these challenges, the FDC report offers several recommendations. First, Nigeria should adopt an all-inclusive unit valuation system for imported goods. This approach would focus on accurate unit prices, reducing the prevalence of underpricing—a strategy often undetected by cargo scanners.

Second, greater attention must be paid to multinational corporations importing goods into Nigeria. As seen in Uganda, these firms are adept at evading taxes through sophisticated means, including transfer pricing and profit shifting to low-tax jurisdictions. By undermining the domestic tax base, they deprive the government of much-needed revenue.

The FDC advocates for a multi-pronged approach, including meticulous unit value analysis, to curb profit shifting and underpricing. Such measures would not only enhance revenue collection but also ensure a fairer tax system for all stakeholders.

In conclusion, while the installation of scanners was a step in the right direction, it is clear that technology alone cannot solve the problem of border tax evasion. Nigeria must adopt comprehensive strategies to tackle underpricing, strengthen oversight of multinational corporations, and close the revenue gaps that hinder its economic potential.