Over the past decade, Nigeria has struggled to keep pace with the economies ahead of it, while those once trailing have closed the gap and, in some cases, overtaken it.

In 2010, the average Nigerian was 2.62 times wealthier than their counterparts in Ghana, Kenya, Rwanda, and Uganda. Fast forward to 2023, that advantage has dwindled by 39 percent, leaving Nigerians only 1.61 times wealthier. On average, a Kenyan and a Ghanaian are now 1.3 times wealthier than a Nigerian, while Rwanda and Uganda have virtually caught up according to BusinessDay analysis.

On the economic front, Nigeria’s economy in 2010 was, on average, 18 times larger than those of seven peer African nations, excluding South Africa. By 2023, this margin had shrunk to just 10 times, with Egypt surpassing Nigeria in economic size. This trend raises critical questions: Why are others catching up with Nigeria, while it struggles to ascend?

One answer lies in policy reform and institutional inefficiency. As Bismarck Rewane aptly noted, “Policy change without institutional reform is a problem.” Recent economic reforms, while necessary, have plunged citizens and businesses into deeper hardship. Even the World Bank acknowledges that Nigeria will need 10 to 15 years of consistent reforms before tangible benefits are felt.

Health Sector: A Deteriorating Edge

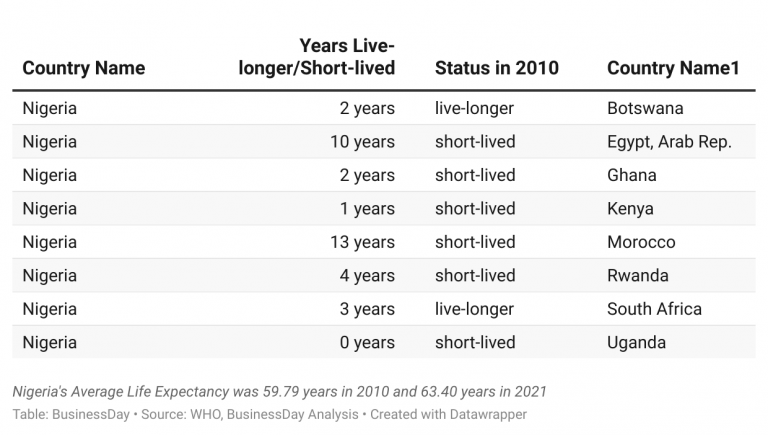

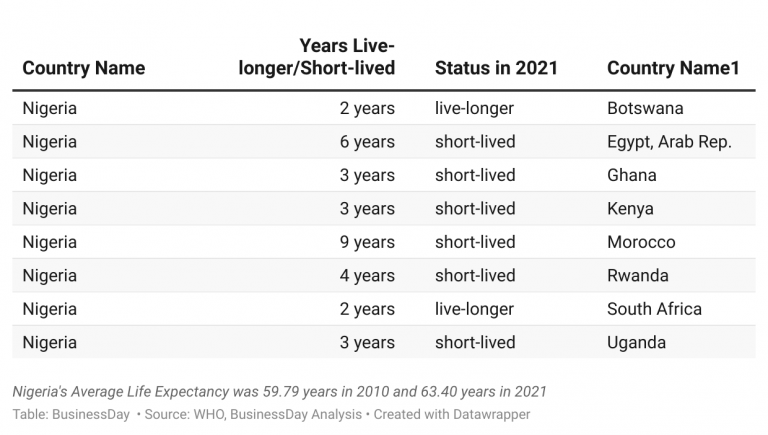

In 2010, a Nigerians life expectancy exceeded that of Botswanans and South Africans by 2.43 years on average. By 2021, the gap has been reduced to 2.03 years. While Nigeria’s average life expectancy rose marginally from 59.79 years in 2010 to 63.40 years in 2021, few other nations have made far greater strides.

Walter Ollor, Professor of Economics, and a former chairman of the International Merchant Bank, highlights the obvious realities of the health sector. “In some hospitals, you must buy every single item and pay upfront before receiving care, even in life-threatening situations,” he said. “Universal health insurance is crucial. It will ensure longer lives and better health outcomes for all.”

Power Sector: A Persistent Bottleneck

Nigeria’s electricity generation hit a three-year high of 5,105 MW in July 2024. Yet, this pales in comparison to South Africa, which generated 42,000 MW in January 2024. In a surprising turn, Tanzania’s government recently shut down five hydro-power stations—not due to shortages, but to manage excess electricity.

In 2004, Nigeria’s electricity consumption per capita was 10.86 times less than the average of seven selected African nations (Botswana, Egypt, Ghana, Kenya, Morocco, South Africa and Tanzania). A decade later, while these countries improved their per capita consumption, Nigeria’s figures remain dismal. For instance, South Africa consumed 4,183.83 kWh per capita in 2014, compared to Nigeria’s 142.13 kWh—a staggering 29.44 times difference according to the World Bank data analysed by BusinessDay.

The obstacles in Nigeria’s power sector—including outdated transmission infrastructure, gas shortages, and poor governance—are well-documented. Countries like Egypt and Morocco have successfully leveraged Siemens to address similar challenges, reaping significant results. In Nigeria, Siemens first engaged in the early 2000s, with little to show for it. Under Buhari’s administration, another Siemens deal failed to gain traction. Now, the current government has approved a €161 million Siemens project in 2024. Why does a company that delivers results elsewhere falter in Nigeria?

Mohammed Haruna, a Journalist and a former Vision 2010 member, attributes past failures to a lack of continuity in visioning. “If Obasanjo had implemented Vision 2010 proposals, we could have overcome many of these challenges,” he remarked in Daniel Obi’s Lost Vision. Haruna points out that Nigeria’s transmission network is obsolete, undermining the little power it generates.

Debt: An Underutilised Tool

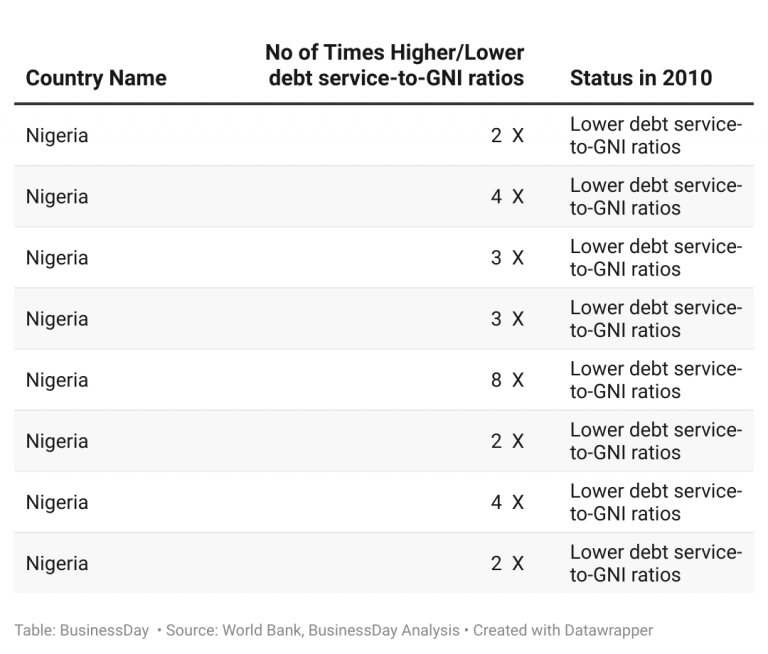

Economic theory emphasises debt’s role in financing essential public goods during periods of growth. In 2010, Nigeria’s debt service to Gross National Income (GNI) ratio was 3.29 times lower than the average of its peer nations. By 2022, this gap had narrowed to 2.38 times, indicating Nigeria’s relative underutilisation of debt.

Contrary to popular belief, debt accumulation can drive development if strategically deployed. Nations that have closed the gap with Nigeria carry higher debt service-to-GNI ratios. The challenge lies not in taking loans but in ensuring they serve the public good, rather than elite interests.

Shubham Chaudhari, former World Bank Country Director for Nigeria, stressed the importance of elite consensus during a 2023 symposium at the University of Ibadan. He shared an illustrative analogy: “In some countries, elites grow a small loaf of bread into a larger one so everyone gets a share. In Nigeria, the small loaf is not only left unexpanded but is monopolised by the elite.”

The Way Forward

Nigeria’s current trajectory is unsustainable. Institutional reforms must accompany policy changes to ensure long-term impact. Universal health insurance, investment in power infrastructure, and strategic debt utilisation are crucial steps. Above all, a commitment to elite consensus and sacrifice for the greater good will determine whether Nigeria can reverse its decline and reclaim its position as a leader on the African continent.

The path ahead is arduous but not insurmountable. Will Nigeria seize the moment or remain a case study in missed targets and squandered opportunities?