… New Eurobonds surpass older issues in returns

… Nigeria stares down $12bn in Eurobond payments over next decade

When Nigeria returned to the Eurobond market with its latest $2.2 billion offer, it wasn’t just economic reforms that lured investors—it was the eye-catching yields.

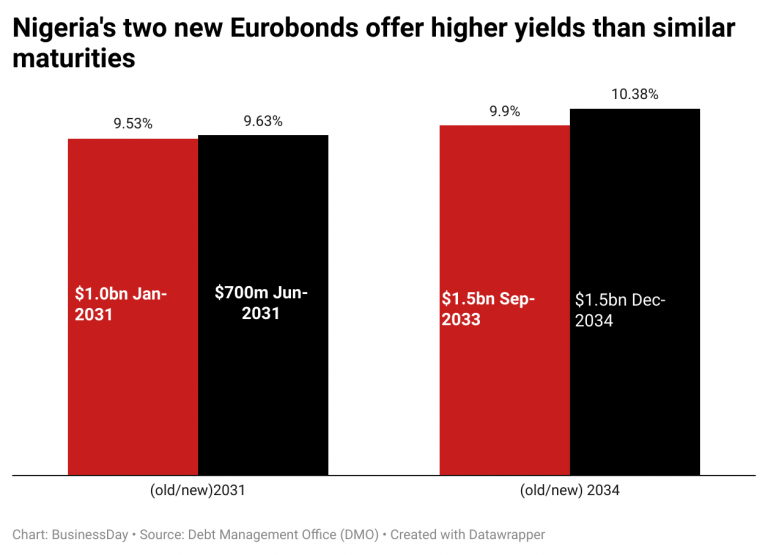

Like bees to honey, global investors were drawn to Nigeria’s mouth-watering interest rates, with the government offering returns of 9.625 percent for a six-and-a-half-year bond and 10.375 percent for a ten-year issuance.

For yield-hungry investors, these bonds are irresistible compared to similar Nigerian Eurobonds trading on the secondary market and those issued by other African economies this year.

A Bounce in New Bonds

Nigeria’s new $700 million Eurobond maturing in 2031 was priced at 9.625 percent, higher than the 9.53 percent secondary market yield on the country’s existing $1 billion Eurobond due January 2031, according to Debt Management Office (DMO) data.

Similarly, the 2034-maturity $1.5 billion Eurobond came with a 10.375 percent yield, eclipsing the 9.9 percent on the older 2033 bond.

“Looking at existing maturities, the new bonds offer higher yields than comparable short- and mid-term Eurobonds, making them highly attractive for Foreign Institutional Investors,” said Igho Alonge, asset manager and wealth advisor.

Alonge predicted yield compression as demand picks up in the secondary market, a signal that investors are eyeing the new bonds eagerly.

Giant “yield” of Africa

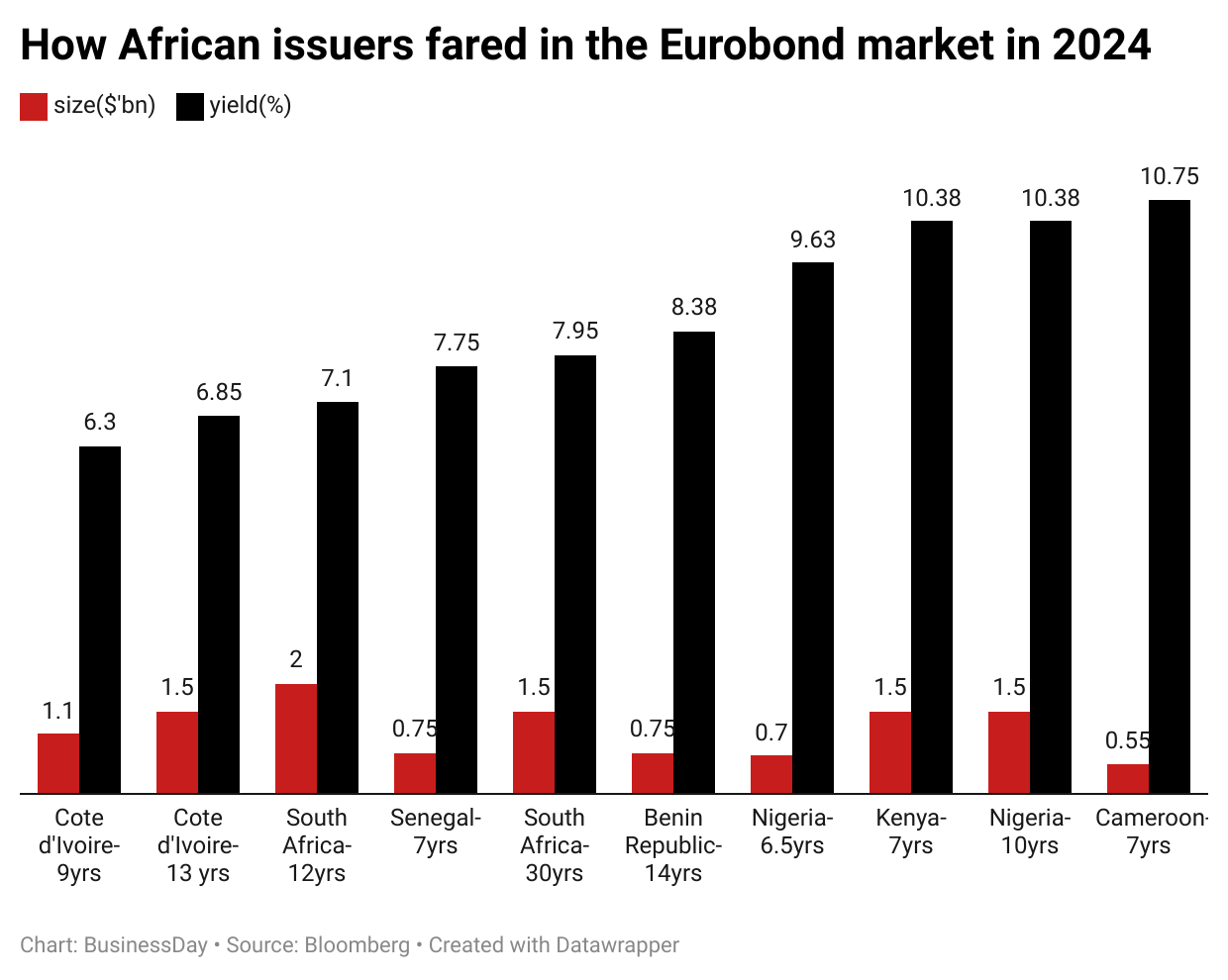

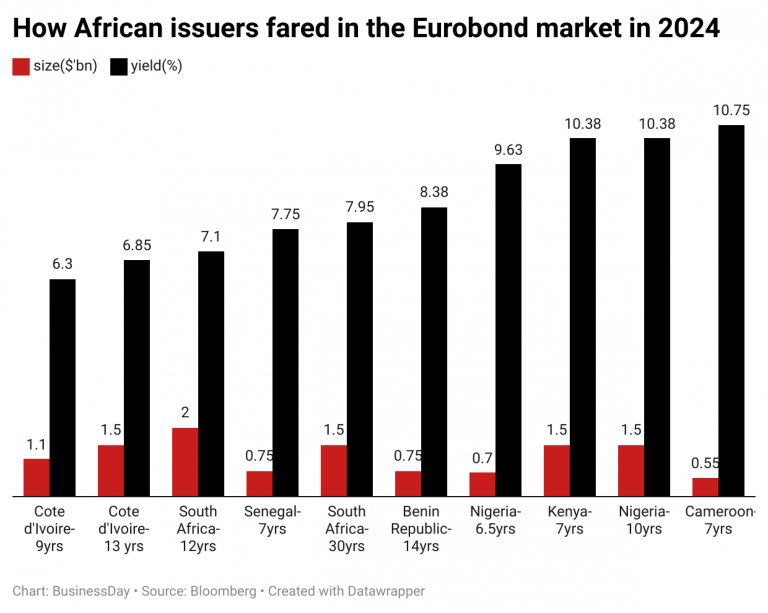

Nigeria joined six other African nations—Kenya, Cameroon, Côte d’Ivoire, Benin, Senegal, and South Africa—to tap the Eurobond market this year.

However, Nigeria’s borrowing came at a steeper cost compared to most of its peers, excluding debt-strained Kenya and Cameroon, whose bonds are junk-rated.

Kenya, for example, paid 10.375 percent for its seven-year $1.5 billion bond, reflecting concerns over its fiscal challenges.

The East African nation was under pressure to refinance a maturing $2 billion bond, while recent downgrades by Moody’s, Fitch, and S&P highlighted growing investor skepticism.

Cameroon, grappling with a public debt burden expected to hit 250 percent of government revenues this year, issued a similar-tenor $550 million Eurobond at an even higher rate of 10.75 percent.

“In spite of improved market conditions, the interest rate is still high, making the operation costly and indicating persisting investor concerns about the country’s external debt and fiscal sustainability,” said Raphael Cecchi, an analyst at Credendo.

As of November 15, 2024, Cameroon’s Long-Term Foreign-Currency Issuer Default Rating (IDR) is ‘B’ with a negative outlook.

Cameroon remains plagued by insecurity and violence in the north due to Islamist terrorism, and by a continuing armed conflict in the anglophone southwest regions.

A possible political crisis is to be feared in the coming years with long-serving President Paul Biya, 91, announcing his candidacy for another seven-year term at the October 2025 elections.

“His old age means he is very unlikely to serve a full term this time, which will probably pave the way to a period of political and economic uncertainty (given the absence of a successor), possibly leading to high instability,” Cecchi said.

Lagos-sized West African neighbour outshines Nigeria

Meanwhile, countries like Côte d’Ivoire, Benin, Senegal and South Africa secured comparatively cheaper financing.

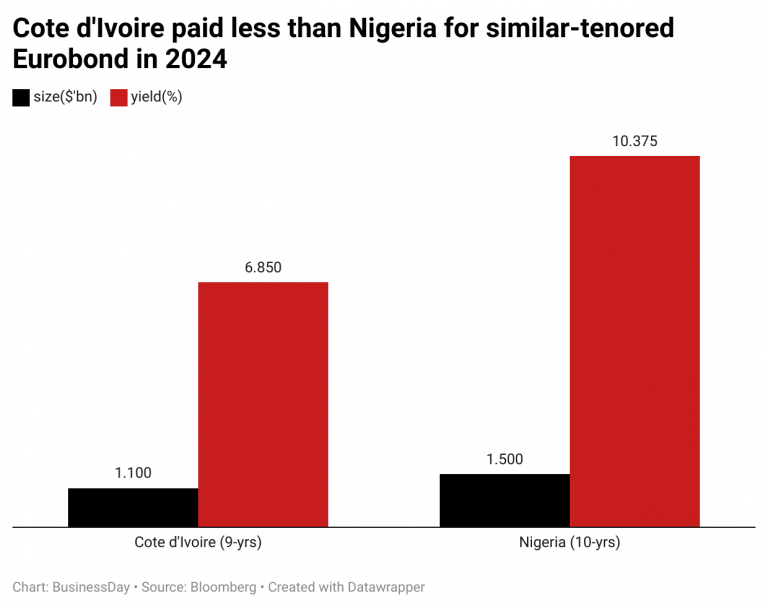

Côte d’Ivoire, the world’s largest cocoa producer, sold its first dollar bonds in almost seven years, issuing two tranches of debt totaling $2.6 billion in an offering that was oversubscribed more than three times.

The West African country of 29 million raised a nine-year $1.1 billion sustainable bond at 6.3 percent and a conventional bond at 6.85 percent, according to authorities.

South Africa’s Eurobonds attracted rates of 7.1 percent (12-year) and 7.95 percent (30-year).

Typically, a longer-dated bond attracts higher interest than one with a shorter tenure. This means South Africa would have paid less than Nigeria did to raise a 6.5-year and 10-year bond.

Benin, in its debut Eurobond sale, issued a 14-year $750 million bond at 8.38 percent, achieving near-sevenfold oversubscription.

Senegal, another of Nigeria’s West African neighbours, also raised $750 million in debt maturing in 2031 at a coupon rate of 7.75 percent, with JP Morgan Chase & Co managing the sale which happened in June.

The emerging oil and gas producer sold $500 million in the first instance, which was increased by $250 million the next day.

The Debt Ahead: Nigeria’s $12bn Eurobond Schedule

Nigeria now has 14 outstanding Eurobonds, and with the addition of the new 2031 and 2034 maturities, the government faces annual principal payments for the next decade, starting November 2025.

The total repayment obligation stands at $11.868 billion through 2034, excluding maturities in 2038, 2047, 2049, and 2051, which amount to an additional $4.75 billion.

The scale of these payments underscores Nigeria’s rising external debt obligations, leaving no room for complacency.

As global investors count their returns, analysts say Nigerian policymakers must ensure the loans are effectively deployed to fuel sustainable economic growth.