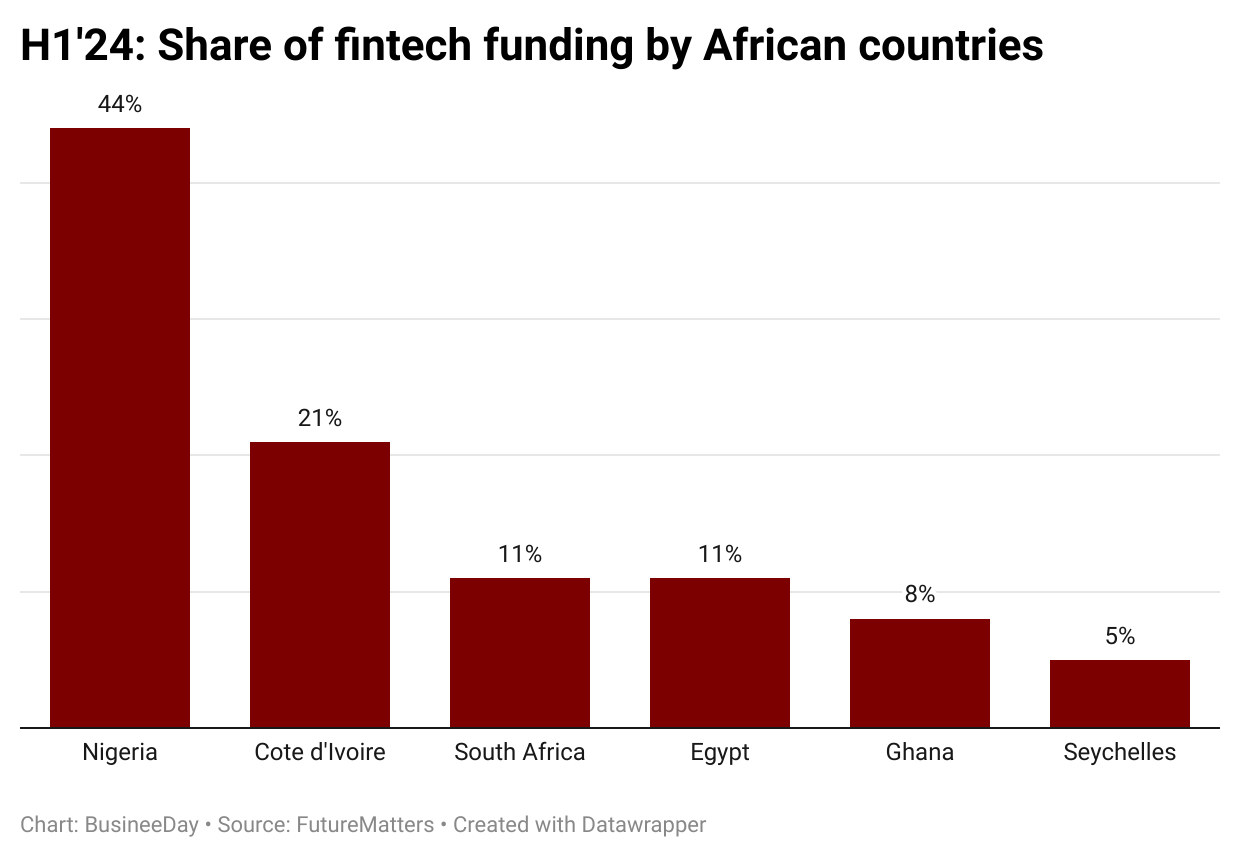

Nigeria remains the frontrunner in Africa’s fintech sector, accounting for 44 percent of the total fintech funding raised across Africa in the first half of 2024, according to a new report by FutureMaters.

The report on the State of Fintech in Africa: First Half 2024 disclosed that despite an overall decline in investment across the continent’s fintech sector, Nigeria accounted for 44 percent of the total fintech funding, followed by Cote d’Ivoire with 21 percent, and South Africa with 11 percent.

Other countries included Egypt with 11 percent, while Ghana and Seychelles accounted for 8 percent and 5 percent, respectively. According to the report, in the first half of 2024, investments in the fintech sector in Africa fell by 77 percent to $286 million compared to $826 million in H1 2023.

Similarly, data by Afridigest, an African data and research platform, revealed that among the big four African countries, Nigeria led with the highest fintech funding of $140 million, followed by Kenya with ($97 million), Egypt with ($35 million) and South Africa with ($34 million).

It said, “Nigeria, Egypt, Kenya, and South Africa (NEKS) accounted for 90 percent of fintech funding. But they only accounted for 70 percent of deals. While investors increasingly explore beyond these core markets, they’re core for a reason — and they dominate big-ticket deals.”

Nigeria is known as a tech powerhouse in Africa, and recent data revealed its substantial lead over its African counterpart despite losing its top spot to Egypt the previous year, according to experts.

Iyinoluwa Samuel Aboyeji, co-founder and founding chief executive officer of Accelerate Africa, acknowledged the dip in funding but expressed optimism about the human capital driving the fintech space.

“While the significant decline in investments is a cause for concern, the resilience shown in certain regions and the crucial role of human capital in driving sustainable growth provides a glimmer of hope,” Aboyeji said.

The State of Fintech in Africa report emphasised that deal activity, particularly in East Africa, shows resilience and highlights potential growth areas despite this downturn.

“The region’s funding doubled to $16.4 million, driven by innovation labs that support startups through incubation, mentorship, and capacity-building programs,” it said.

The report also analysed that deal activity was resilient, although it declined 30 percent, from 144 deals in H1 2023 to 100 deals in H1. However, globally, deal activity fell by almost 20 percent in H1.

Similarly, the global fintech sector investments declined 18 percent during the surveyed period with the average deal size on the continent declining to $4.0 million from $10.5 million. On a month-on-month basis, fintech investment in Africa fell by 75 percent to $82 million in Q2 2024 from $339 million in Q2 2023.

The number of deals was resilient year-on-year, declining only 18 percent to 58 deals in Q2 2024 from 71 in Q2 2023. In contrast, global fintech investments increased to $18.8 billion in Q2 2024 from $16.0 billion in Q2 2023.

In Q2 2024, South Africa and Egypt continued to attract most of the fintech investment in the region, accounting for 72 percent of the total, up from 51 percent in Q2 2023.

“Nigeria held firm, with its share declining to 8.2 percent in Q2 2024, from 9.2 percent in Q2 2023. Seychelles emerged as an emerging fintech player in the region, attracting 19 percent of total investments in Q2 2024,” it said.

According to a report by BDO South Africa, Nigeria is one of the “Big 3” Fintech markets in Africa. Out of 678 start-up fintech companies in 2023, 217 are from Nigeria, which equates to 32 percent.

“This is why Nigeria can be seen as Africa’s Fintech hotspot. This is up 50.1 percent on 144 in 2021, which had in turn been up from 101 in 2019 and 74 in 2017,” it said.