Global oil markets remained under intense pressure on Tuesday, with Brent crude dropping below $20 per barrel for the first time in 18 years while other major benchmarks across the world tumbled.

Brent crude, the international oil marker, slipped as low as $18.10, before recovering slightly to trade around $19.50 by mid-afternoon in Europe.

The fall suggests traders see no immediate let-up in the collapse in crude demand that sent some US oil benchmarks plunging below $0 for the first time on Monday, leaving producers paying for buyers to take their oil away. The severe drop in demand has coincided with still robust levels of production in the US with oil storage tanks just weeks away from reaching capacity.

“The car is speeding up and market forces will inflict further pain until either we hit rock bottom, or Covid clears, whichever comes first,” said Michael Tran, commodity strategist at RBC Capital Markets.

Coronavirus has sent the oil sector into a state of crisis, with lockdowns and travel bans implemented by authorities slashing global demand for crude by as much as a third this month from pre-crisis levels.

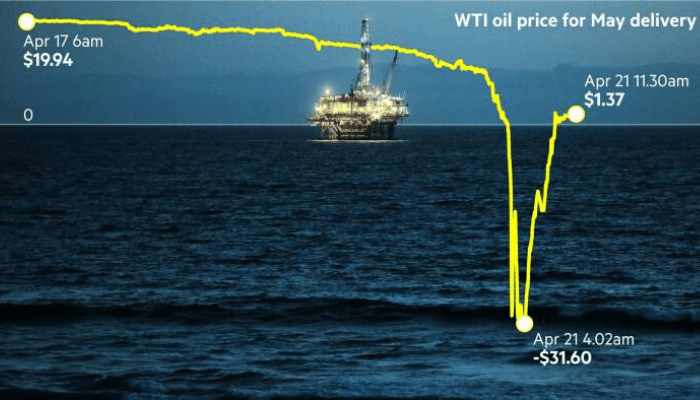

Contracts for the US benchmark West Texas Intermediate for delivery next month tumbled as low as minus $40 a barrel on Monday, marking the first time it had fallen in to negative territory, where it largely remained on Tuesday. The slide was exacerbated by traders seeking to offload any obligations to take on physical product ahead of the contract’s expiry today as storage reached capacity at its delivery point in Cushing, Oklahoma.

The June contract, which held above $20 a barrel on Monday, has also come under heavy selling pressure, dropping 30 per cent to $14.50 as trading began in New York, suggesting the blowout in the May contract was more than just a technical blip.

“The contagion has spilled over to WTI June 2020 deliveries, which could also be well on their way into the red as we move towards physical delivery dates,” said Louise Dickson at Rystad Energy.

Analysts said both Brent and the June WTI contract were likely to face further downward pressure in the coming weeks, given the supply glut shows little signs of abating.

Plans for unprecedented supply cuts by some of the world’s biggest producers such as Saudi Arabia and Russia have so far failed to offset the tumble in oil demand. This has prompted officials and Opec delegates to talk up the market in any way they can.

Saudi Arabia said on Tuesday it is prepared to take additional measures, alongside other producers that are part of the Opec+ alliance, to prop up the oil market and achieve market stability. Riyadh’s state news agency SPA cited a cabinet statement saying: “[The] Kingdom is committed with Russia to implement production cuts over next couple of years.”

For its part, Russia downplayed the collapse in crude prices, saying there was no need to view it as an “apocalyptic” event after its Ural blend, which is loosely based on Brent, fell to its lowest level since 2002 on Tuesday.

“The chaos with futures is absolutely speculative, just a trading issue,” Kremlin spokesman Dmitry Peskov said. “Of course there is no need to give this an apocalyptic hue.”

Wall Street opened lower, with the S&P 500 sliding 1.5 per cent, dragged down by a 2.1 per cent fall in energy stocks.

The oil collapse has also underscored the powerlessness of US president Donald Trump, who had pressured Saudi Arabia and Russia to agree to supply curbs in a bid to support the domestic shale industry.

On Tuesday he said on Twitter he had told the energy and Treasury secretaries to “formulate a plan” to make funds available to energy producers “so that these very important companies and jobs will be secured long into the future”.

European equities also traded lower, due in part to weakness in energy stocks, with the continent-wide Stoxx 600 down 2.4 per cent. In London the FTSE shed 2.3 per cent, while Frankfurt’s Dax slid 3 per cent.

In fixed income, the yield on the 10-year US Treasury fell 0.04 percentage points to 0.572 per cent as investors retreated to the safety of core government debt.