Parents often pray that oneŌĆÖs children should be better in all human endeavour. The path to success could be a long one if not properly planned and also if the required support a parent should lend to their kids is missing. This may result in children upon attaining adulthood having to struggle in other to make ends meet.

This can be avoided if parents take the right measure today to secure to an extent the future of their kids. The interesting thing here is that you donŌĆÖt have to wait till you bare a child before taking necessary steps to a better life for your unborn child(ren).

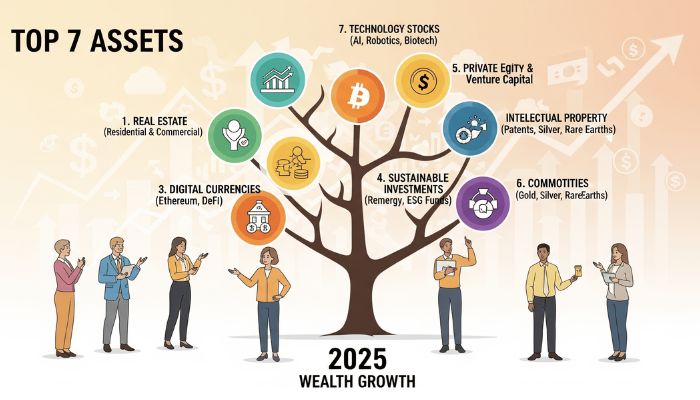

To plan for your childŌĆÖs future, you have a galore of investment avenues but planning and investing wisely is no childŌĆÖs play.

Simply, saving and investing in an ad-hoc manner may not help. You need to identify the appropriate investment avenues at an opportune time to meet your financial goals.

Moreover, you need to strike the right asset allocation balance as you progress towards each of the financial goals set for your childrenŌĆÖs better future.

Here are some tips

Family planning:┬ĀThe first step to creating a prosperous future for your children (and perhaps theirs) is in planning how many children you should have based on your financial capacity (amongst other considerations) to take care of them.

In the past, people believed having a lot of children could improve oneŌĆÖs fortune because more children meant a higher likelihood of one of them making it big in life. Today such argument is no longer convincing as having more children than one could cater for would result in depriving them of quality education, health and nutrition.

Invest on behalf of your child(ren):┬ĀIt is never too early to create investments for your child(ren). You should set aside a portion of your income that would be put into asset classes that can preserve wealth so they can be passed on to your chil(ren)

Invest in Real Estate:┬ĀOne of the best ways to invest for a long period is in real estate because property value typically goes up over time.

Imagine being handed a property located in Victoria Island that was acquired some decades back by your parents; you would agree that at the time of acquisition the property would not be valued as much as it is today. Since land is fixed in supply, the value is sure to grow over time so make plans to pass on good real estate to your offspring.

Avoid unnecessary debt, be prudent:┬ĀTo be able to pass on wealth to your child(ren) you must be financially responsible and avoid being roped in debt.

This is not to say debt is a bad thing because you would need to borrow at some point in time. You can borrow to invest in ventures with an attractive and certain return.

The important thing here is to ensure you do not leave debt instead of wealth for your children. To do this ensure you balance your debt-to-income ratio should not exceed 36 percent according to Investopedia.

Read also:┬ĀCircular flow of wealth: How to not remain poor

Plan your retirement:┬ĀTo avoid becoming financially dependent on your children endeavour to plan your retirement ahead of time.

Making provisions for life after work is beyond having a pension account and includes making investments you can fall back on eventually.

Make a will:┬ĀThe perception of a will in this part of the world is a funny one as some may imply that making a will may indicate death is around the corner ŌĆō which no one prays to experience ŌĆō hence, because we are very religious, we act by faith that we wonŌĆÖt die soon and ignore the importance of making one. LetŌĆÖs look at the bright side. According to Investopedia, a will is a legal document that sets forth your wishes regarding the distribution of your property and the care of any minor children. If you die without a will, those wishes may not be followed. Further, your heirs may be forced to spend additional time, money, and emotional energy to settle your affairs after youŌĆÖre gone.

You can consider insurance

Insurance in its purest sense is protection against a financial loss/uncertainty which includes the risk of illness, disability, damage to property, and the most final of them all ŌĆō oneŌĆÖs demise.

The value of your loved oneŌĆÖs life is a very sensitive issue as your loved ones are priceless.

But it becomes necessary to safeguard from problems caused by under-insurance.

Human Life Value (HLV) of an earning member in the family could be defined as the amount that the family would require to retain the same standard of living in the absence of the earning member. This would be the maximum amount for which a person can seek insurance protection.