The relatively attractive valuation of cement makers in Africa’s largest economy means they will benefit the most from investor’s interest.

Nigerian cement sector has a price to earnings (P/E) ratio of 12.50 times, this compares with Turkey’s P/E ratio of 36.90 times, India, (31.31 times); South Africa (S/A), (29.20 times), and Mexico, (12.90 times).

Analysts at Afrinvest Securities Ltd have issued a Buy rating on Lafarge Africa and Dangote Cement, while valuation of Cement Company of Northern Nigeria (CCNN) is currently under review due to the recent merger with Kalambiana cement.

The investment house added that it expects Lafarge Africa’s latest debt restructuring and cost containment strategies to support profitability in 2019, while for Dangote Cement it expects cost efficiency and smooth Pan African operations.

The three major producers of the building materials are intensifying strategies to take advantage of the huge infrastructure deficits and demand for housing.

President Muhammadu Buhari has presented a budget of N8.90 trillion for 2018, while federal government has raised Eurobonds to fund capital projects across the country.

Dangote Cement, controlled by Africa’s richest man, Aliko Dangote, said last year it’s looking to raise $500 million from a Eurobond sale and will also issue 300 billion naira in local-currency bonds to refinance debt and boost expansion.

Meanwhile, Lafarge Africa is seeking to raise about N100 billion through equity or debt on top of a rights issue of about N130 billion the last quarter of 2017 in order to reduce debt in its balance sheet.

The proportion of debt in the capital structure of the company is high as debt to equity ratio or leverage ratio, stood at 191.52 percent as at September 2018, higher than the 163.24 percent the previous year. Total debt in the balance sheet hit N254.18 billion as at September 2018.

Lafarge Africa has an interest coverage ratio of 0.54 times for September 2018, as operating income of N19.13 billion got swallowed by finance cost of N34.925 billion, resulting in a loss after tax of N10.37 billion in the period under review.

Dangote Cement has been taking advantage of the Nigerian rapid housing and infrastructure demand across Africa to underpin earnings and increase its share of the market.

The largest producer of the building material in the country has an excellent energy mix as it continues to spend less in generating each unit of revenue. For instance, cost of sales ratio fell to 42.53 percent in December 2018 from 43.60 percent as at December 2017.

CCNN implemented a merger with Kalambaina cement that saw its capacity hit 2 million metrics tonnes.

Both companies are owned by BUA Cement Limited, the country’s third largest producer of the building material with a capacity of 8 million metric tonnes.

Analysts at Afrinvest Securities Ltd said that after the merger, CCNN’s shares outstanding had risen to 13.10 million from 1.30 million shares, which investors priced at 9.50 times.

“We believe the new merger will result in improved efficiency for CCNN,” said Analysts at Afrinvest Securities Ltd.

Talking about efficiency, the company switched energy mix from the use of LPFO to a cheap source of energy, coal. The strategy paid as cost of sales ratio fell to 55.90 percent in September 2018 as against 61.57 percent as at September 2017.

Of the three largest producers of the building materials, CCNN has the strongest margin growth based on third quarter results. Its gross profit moved to 44.18 percent in September 2018 from 38.12 percent the previous year. Net margin increased to 20.50 percent in September 2018 from 14.90 percent the previous year.

CCNN’s shares closed at N19.95 as of 2:00 pm in Lagos, while market capitalization of N262.21 billion. It has a P/E ratio of 4.83 times earnings.

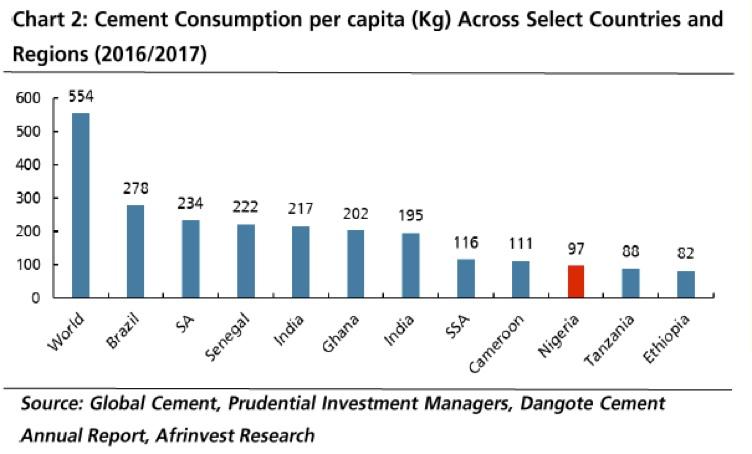

Cement makers are feeling the pinch of an economic lethargy, as lack of supportive policy fame work to drive mortgage activities, low consumer purchasing power, delay in the passage of the budget, have left the country playing catch up game with other sub Saharan peers despite its huge population that crave for consumption .

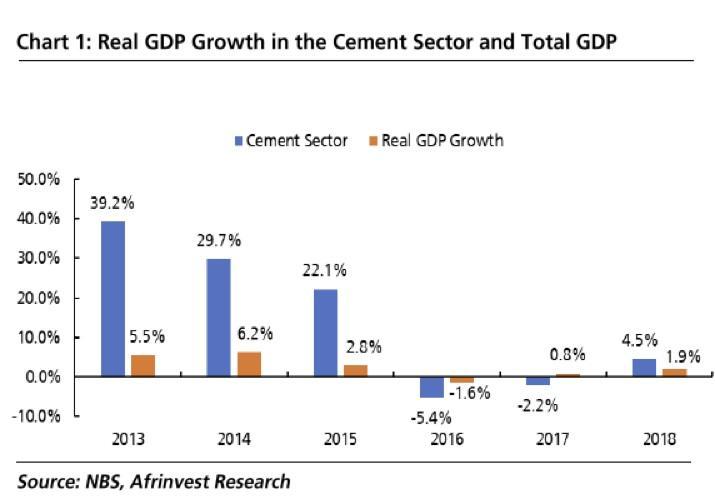

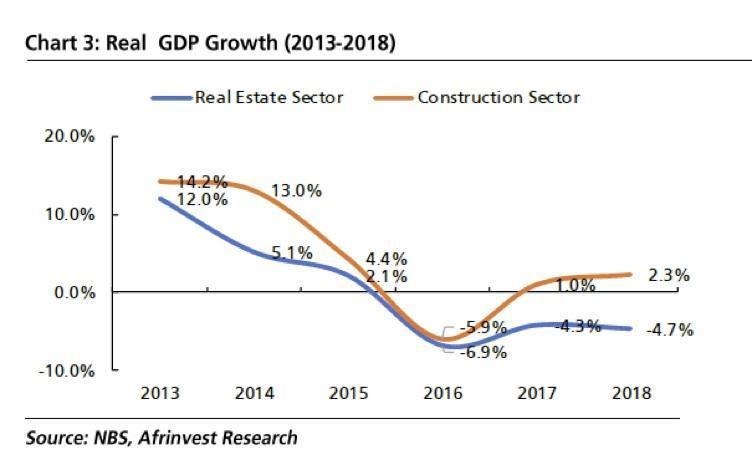

Nigeria, where the cement sector, which accounted for 0.80 percent of (N576.60 billion) of real GDP as at full year 2018, has seen growth moderate to an average of -1.0 percent in the past three years compared to 16.90 percent the preceding decade, according to a recent report by Afrinvest Securities Ltd.

Dangote Cement’s share price closed at N196.60 as of 2:00 pm Lagos time while it market capitalization was N3.35 trillion. Its shares trade at price to earnings of 8.60 times, signalling an opportunity for investors to buy the company stocks.

Lafarge Africa’s shares closed at N12.90 as of 2:00 pm Lagos time, while market capitalization stood at N118.8 billion.

BALA AUGIE