That agriculture in Nigeria has been abandoned for decades in favour of oil dollars may already be sounding like a ‘rather stale story’, but the reality remains felt in everyday life. Even when considered conservative, Nigeria’s food import bill is estimated between 5 and 7 billion US dollars, based on variations in different data sources including the Federal Ministry of Agriculture, National Bureau of Statistics, and the World Bank.

Nigeria, which prides itself as the most populous black nation on earth, is largely unable to adequately feed the growing population, despite an abundance of agricultural resources yet to be fully harnessed. Millions of smallholder farmers grapple to survive, and even agribusinesses lack access to funds and support to improve food production. Government funding initiatives have become traditional announcements; bank funds are a no-go area with crippling interest rates, while private capital has been elusive.

It has become an anthem for many people in the agric sector to recite the challenge of funding when asked of the problems confronting them; coming ahead of infrastructure and market inefficiencies. However, it is not an anthem they recite joyfully, rather, the reality they live as agribusiness owners.

“I cannot approach banks for loan at 30 percent interest rate. The Agric intervention funds at single-digit interest rate are not accessible, they are mere political statements,” said Bode Adetoyi, chairman, Poultry Association of Nigeria (PAN), in an earlier phone interview, also lamenting that the “poultry industry and feed business is already collapsing and farms, feed mills are closing every day,”

Ada Osakwe, CEO, Agrolay Ventures, also put the financial logjam in perspective, explaining that in Nigeria’s agriculture sector, securing capital through commercial banks is typically hard to access and expensive. In spite of the large financing needs of agricultural actors, the public and private sector have not devoted sufficient financial resources for impact.

The situation appears hopeless all round, yet, a ray of hope may exist in an emerging concept of ‘patient capital’, one in which private equity may solve the country’s food security challenge if the right compromises are achieved. Private equity in its pure form, as interactions with several sources showed, may not be suitable for agriculture in Nigeria as it is today.

“Patient Capital”: An impasse in finding the right mix for PE

At the risk of appearing to want an easy way out, funding agriculture through private equity does not appear to be straightforward in Nigeria. The rules that apply in structured markets are considered unrealistic in Nigeria, thereby discouraging potential investors, as many local businesses find change hard to accomplish in meeting required standards. An impasse it seems.

Rotimi Williams, an agripreneur in his 30s, owns the 45,000-hectare Kereksuk Rice farm, described as the second largest commercial rice farm in Nigeria. According to him, “there is a need to have funds that are dedicated to the development of Nigeria and Africa, and understand the challenges in developing countries, so that their criteria are better tailored to those issues. Not coming with generic funds from Kenya or South Africa where the agricultural sector is already relatively developed, and expecting that model will be adaptable here. It is not going to happen.

“They need to create funds that speak to the issues in developing countries like Nigeria,” Williams said.

Agrolay’s Osakwe, who also opined that what agriculture in Nigeria needs is “patient capital”, shares the view by Williams. However, whether or not potential investors will share these views, remains to be seen.

Williams described conditions by PE investors as tough, saying they often “request two year audited financials, and want the company to be setup in a certain way.”

“We are talking about farms, and they are not going to get that. So, limitations are already within the criteria, and also the fact that they are coming into an industry where agriculture itself has been neglected and suddenly you are looking more at Brownfield than Greenfield operations,” Williams explained.

Ade Adefeko, vice president, Corporate and Government Relations at Olam Nigeria, described agriculture as a very risky sector particularly in the area of crop production, emphasising the need for the sector to be de-risked. According to him, investors need to deploy patient capital and have a long-term view. In addition, they need to understand the economics and cycles.

“I often tell investors they need to understand the economics of every sector; Aviation economics, Telecoms economics, and Agricultural economics is no different,” said Adefeko.

The limitations in business structures, as a number of analysts have identified, may perpetually deny the Nigerian agric sector of adequate private sector funding, regardless of its excuses in terms of neglect over the years.

Taking private equity & venture capital beyond hopes

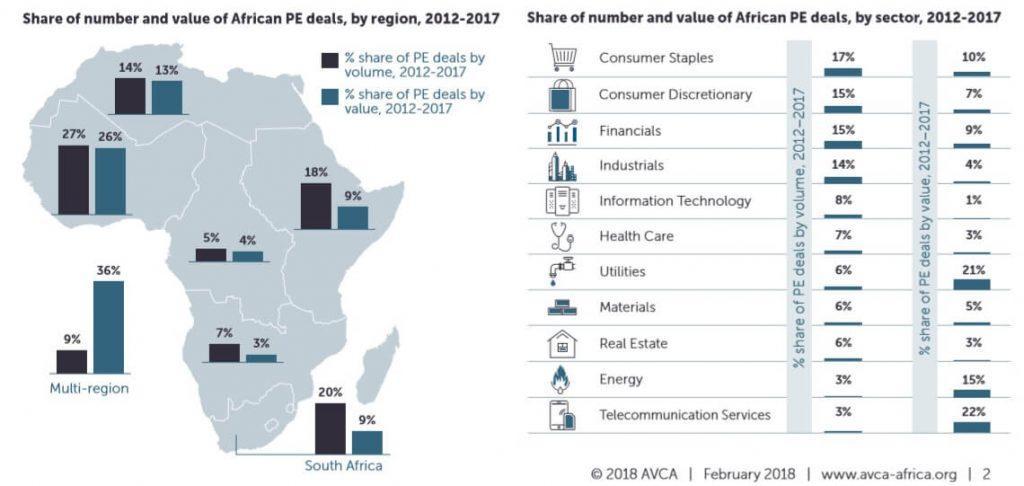

From 2012 to 2017, the African Private Equity and Venture Capital Association (AVCA) puts the total value of African PE Fundraising at $17.3 billion. In the 2017 Annual African Private Equity report, the sectors identified to have attracted these funds are Consumer Staples, Consumer Discretionary, Financials, Industrials, Information Technology, Health Care, Utilities, Materials, Real Estate, Energy, and Telecommunication Services.

Across Africa, agriculture does not feature in any way in the major sectors from 2012 to 2017, even though the World Bank has estimated the continent has an annual food import bill of $35 billion that is bound to grow, considering the expanding population.

Getting bank loans for the agric sector is a challenge, one that limits expansions and improvement of productivity. At the same time, it appears Nigeria is also faltering in adequately tapping from private equity investments in Africa.

Adefeko, Olam’s VP, remarked, “It is becoming increasingly difficult for individuals and even government to fund agricultural ventures particularly processing and production plants. Therefore, Private Equity/Venture Capital firms put in equity after proper evaluation and sell after a while or hold on depending on their risk appetite.”

Even though the possibilities for PE/VC firms to invest in Nigerian agriculture are considered to be improving, the prevailing reality now is that Nigeria’s agricultural sector is yet to attract as much private equity investments, which would be significant enough to match the country’s potentials and national aspirations.

“For a market as big as Nigeria, we have not had as much Private equity activity as we should,” said Kazim Yusuf, CEO, Kord capital, an investment advisory firm in Lagos.

As Yusuf observed, inadequate private equity activity is a problem with Nigeria generally, but moving into a sector like agriculture, it becomes even more problematic. This, he explains is because even people with experience investing in the Nigerian economy have challenges with agriculture, much less foreigners who are expected to deploy PE funds.

As noted by Osakwe, Agrolay’s CEO who also says as a Senior Advisor in government, she participated in designing the Fund for Agricultural Financing in Nigeria (FAFIN), “Agric is perceived to be unviable, as many agricultural enterprises are not considered ‘investable’ or mature enough for PE capital.

“Instead, like the commercial banks, most PE fund managers focus on the, telecoms, extractive and consumer sectors, which collectively received about 60 percent of Africa PE financing in 2016,” she said.

Osakwe offered more perspective, explaining that unfortunately, with FAFIN and other PE funds, their agriculture investments are still limited by the need to invest in deals with a minimum legitimate operating history. Most Nigerian agriculture enterprises have been unstructured, or are really only in their early-stages, and so do not meet this requirement. Furthermore, many PE funds have minimum investment sizes from between $10 million and $50 million, numbers that are far above what the majority of Nigerian agribusinesses can absorb.

As a result, PE activity is further constrained in deploying capital because they are unable to find the agribusiness transactions that fit their investment strategy. Yet, PE can help agribusinesses that meet the structural requirements in scaling their operations exponentially.

Mezuo Nwuneli, managing partner, Sahel Capital Agribusiness Managers Ltd, whose company closed $65.9 million funding for agriculture in Nigeria, emphasised the potentials for PE in Nigeria, saying “it has the ability to provide growth capital to selected high-performing companies, to enable them rapidly scale-up. Even more important than the funding is the technical and operational support that private equity firms can provide companies.”

Nigeria’s huge food and industrial needs represent potentials for revenue if local solutions are supported, particularly since the country has over 80 million hectares of arable land with less than half of it under cultivation. The potential for growth and steady flow of revenue in a consumer driven nation of 190 million people, with broad influence over the rest of the sub-region has been underutilised.

The country still holds very good prospects for investments given its large untapped resources, growth potential and substantial infrastructure requirements. What is left is for agribusinesses and private equity managers, to reach a compromise on how to leverage on available opportunities.

CALEB OJEWALE