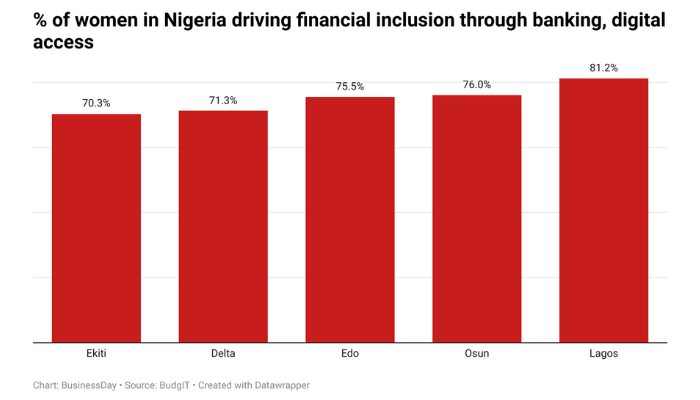

Across Nigeria’s 36 states, Lagos, Osun, Edo, Delta, and Ekiti stand out as the country’s top performers in advancing women’s financial inclusion, driven largely by higher levels of bank account ownership, according to a report by BudgIT.

The 2025 State of Women’s Economic Empowerment in Nigeria report identifies bank account ownership, awareness of financial products, and access to digital tools as the core indicators shaping women’s participation in Nigeria’s financial system.

“States with stronger financial and digital ecosystems consistently show higher levels of women’s financial inclusion,” the report said, adding that “access alone is not enough without awareness and sustained usage.”

Read also:¬ÝWhy financial inclusion is still failing the poor and what must change

Lagos State, with a female population size of 7.8 million across the age group of 15–49, leads the group in overall scale. Data from the 2021 Multiple Indicator Cluster Survey (MICS) show that 81.20 percent of women in Lagos own bank accounts, while 72.68 percent are aware of financial products and services.

However, the report cautions that inclusion in Lagos remains shallow for many women. Only 13.56 percent save in formal financial institutions, and just 23.5 percent have access to loans, despite the state’s multiple empowerment and credit programs.

“While access is high, inclusion remains uneven across income and occupational lines,” the report warns. “Many women are still engaging with the financial system only at a basic transactional level.”

To address these gaps, Lagos recently trained 1,200 women in 12 hard-to-reach communities on financial literacy. Yet the report notes that deeper engagement—through savings, credit, and insurance—remains limited.

In Osun State, women’s financial inclusion gains are closely linked to financial literacy and community-level engagement. The report highlights efforts to integrate financial awareness into social and economic programmes, particularly targeting women traders and small business owners.

According to the report, 76 percent of women in Osun have bank accounts, while 63.06 percent are aware of financial products. Access to loans stands at 42.50 percent, one of the highest figures among the leading states, although only 12.62 percent of women save formally.

“Community-based financial education has helped women better understand banking services, savings options, and digital payments,” the report notes, but adds that “formal saving remains a critical weak point.”

Read also:¬ÝDigitising government payments is a major catalyst in driving financial inclusion in Nigeria in 2025

In Edo State, women’s financial inclusion outcomes are tied to enterprise-focused programmes that connect women-led micro and small businesses to formal financial institutions. These initiatives have supported bank account opening and the adoption of digital payment tools.

The report shows that 75.5 percent of women in Edo have bank accounts, and 65.17 percent are aware of financial products. However, only 11.71 percent save formally, and just 17.30 percent have access to loans.

“There is a clear need to enhance financial inclusion for women entrepreneurs,” the report states. It calls for partnerships with financial institutions to provide mid-sized loans, small grants, and low-interest credit, alongside targeted government programmes and women-focused investment networks to improve access to capital.

Delta State’s inclusion gains are driven by improved awareness of financial products and expanding access to digital channels, particularly agent banking and mobile-enabled services. These channels have helped connect women engaged in trade, agriculture, and small-scale manufacturing to formal financial institutions.

According to the report, 71.3 percent of women in Delta own bank accounts, while 61.52 percent are aware of financial products. Yet only 11.2 percent save formally, and access to loans remains low at 13.70 percent.

“Digital channels are widening access, but depth of usage remains limited,” the report observes.

Ekiti State completes the group of leading states, with the report recognising its focus on embedding digital and financial literacy within the education system. Schools and extracurricular programmes increasingly expose girls and young women to basic financial and digital skills.

“Early exposure is critical for long-term inclusion,” the report states, urging the state to expand beyond basic computer classes into deeper financial and technology skills.

Read also:¬ÝCBN pushes new financial inclusion strategy to power economic growth

Despite these efforts, access gaps persist. Only 12.7 percent of women in Ekiti use computers, and 52.8 percent have internet access, although mobile phone ownership stands at 84.8 percent. Financial inclusion indicators show that 70.3 percent of women have bank accounts, while just 15.72 percent save formally and 18.5 percent have access to loans.

Across all five states, the report identifies a consistent pattern: bank account ownership among women is rising faster than meaningful usage of financial services.

“This gap highlights the difference between access and economic empowerment,” the report added. “Without sustained usage, financial inclusion gains may not translate into financial resilience, business growth, or long-term economic security for women.”