As 2025 drew to a close, AfricaŌĆÖs macroeconomic picture tells a story of various levels of recovery. Growth remained uneven, while inflation trajectories varied widely. Labour markets became more fragile, with currencies stabilising in select economies. Equity markets┬Ā in┬Ā particularly frontier exchanges┬Ā delivered bumper returns.

Policy credibility, commodity dynamics, and external demand became the decisive differentiators. That reality prompted the World Bank to revise its 2025 growth forecast for sub-Saharan Africa upward by 0.3 percentage points from its April AfricaŌĆÖs Pulse projection, with 30 of 47 countries seeing improved outlooks.

Read also:┬ĀNew pension rules add sophistication to capital markets

ŌĆ£The projected acceleration in growth is underpinned by improved terms of trade across much of the region, contributing to currency stabilisation and, in some cases, appreciation,ŌĆØ the World Bank said, noting that easing inflation has allowed some central banks to begin cautiously loosening monetary policy.

An analysis by BusinessDay of AfricaŌĆÖs 10 biggest economies shows which markets stood out ŌĆö and why.

GDP growth: Angola posts tentative turnaround

Among AfricaŌĆÖs biggest economies with third-quarter GDP data available, Angola stood out, recording a quarter-on-quarter improvement from contraction to expansion.

Data from Trading Economics, a global economic data and analytics platform, show that AngolaŌĆÖs economy grew by 0.05 percent in Q3, reversing a 0.1 percent contraction in the previous quarter.

Though marginal, the improvement marks a symbolic return to growth for AfricaŌĆÖs third-largest oil producer, whose GDP stood at $100.9 billion in 2024. Compared with Q3 last year, the economy also exited negative territory, reflecting stabilising oil output and modest gains from diversification efforts.

By contrast, South AfricaŌĆÖs economyŌĆöAfricaŌĆÖs most industrialised and valued at $401.1 billionŌĆöexpanded by 0.5 percent in Q3, down from 0.9 percent in the previous quarter. While growth remained positive, momentum slowed amid persistent structural constraints, including logistics bottlenecks and subdued global demand. Notably, GDP had contracted in Q3 2024, underscoring how fragile the recovery remains.

Nigeria, AfricaŌĆÖs most populous nation with a $252.2 billion economy, saw growth moderate to 3.98 percent in Q3 from 4.23 percent in Q2. Despite the deceleration, performance remained stronger than the 2.55 percent recorded in the same period of last year, supported by services and trade activity following currency reforms.

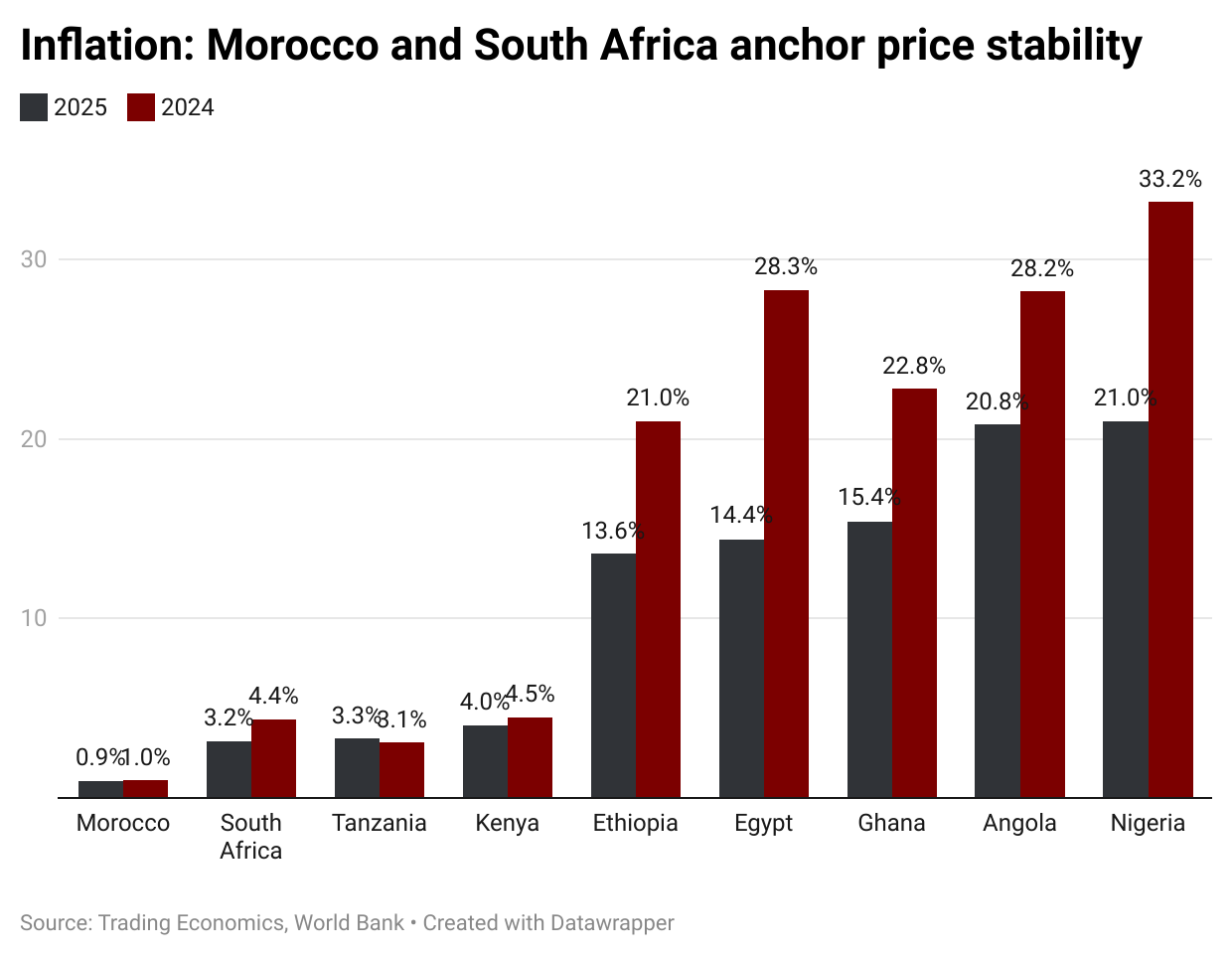

Inflation: Morocco and South Africa anchor price stability

One of AfricaŌĆÖs clearest macroeconomic successes last year was the retreat of inflation from the highs of 2023ŌĆō2024. Tighter monetary policy, stabilising food and energy prices, and calmer currency markets collectively eased price pressures across most regions.

Morocco recorded the lowest average inflation among AfricaŌĆÖs largest economies, at just 0.94 percent between January and October. South Africa followed at 3.15 percent, reflecting credible inflation targeting and easing supply constraints.

MoroccoŌĆÖs achievement was particularly striking. In November, the country recorded deflation for the first time in nearly five years, joining Algeria and Burkina Faso in negative inflation territory in 2025. While disinflation refers to slowing price increases, Morocco crossed into outright deflationŌĆömeaning prices actually fell, boosting consumersŌĆÖ purchasing power.

Elsewhere, inflation outcomes varied widely. Between January and November, average inflation stood at 3.3 percent in Tanzania, 4.04 percent in Kenya, and 13.6 percent in Ethiopia. Egypt recorded 14.4 percent, while Ghana posted 15.4 percent, with Angola reporting 20.8 percent, and Nigeria recoroding 20.96 percent.

Read also:┬ĀThe new supercycle: Why NigeriaŌĆÖs future markets will be built on digital scarcity

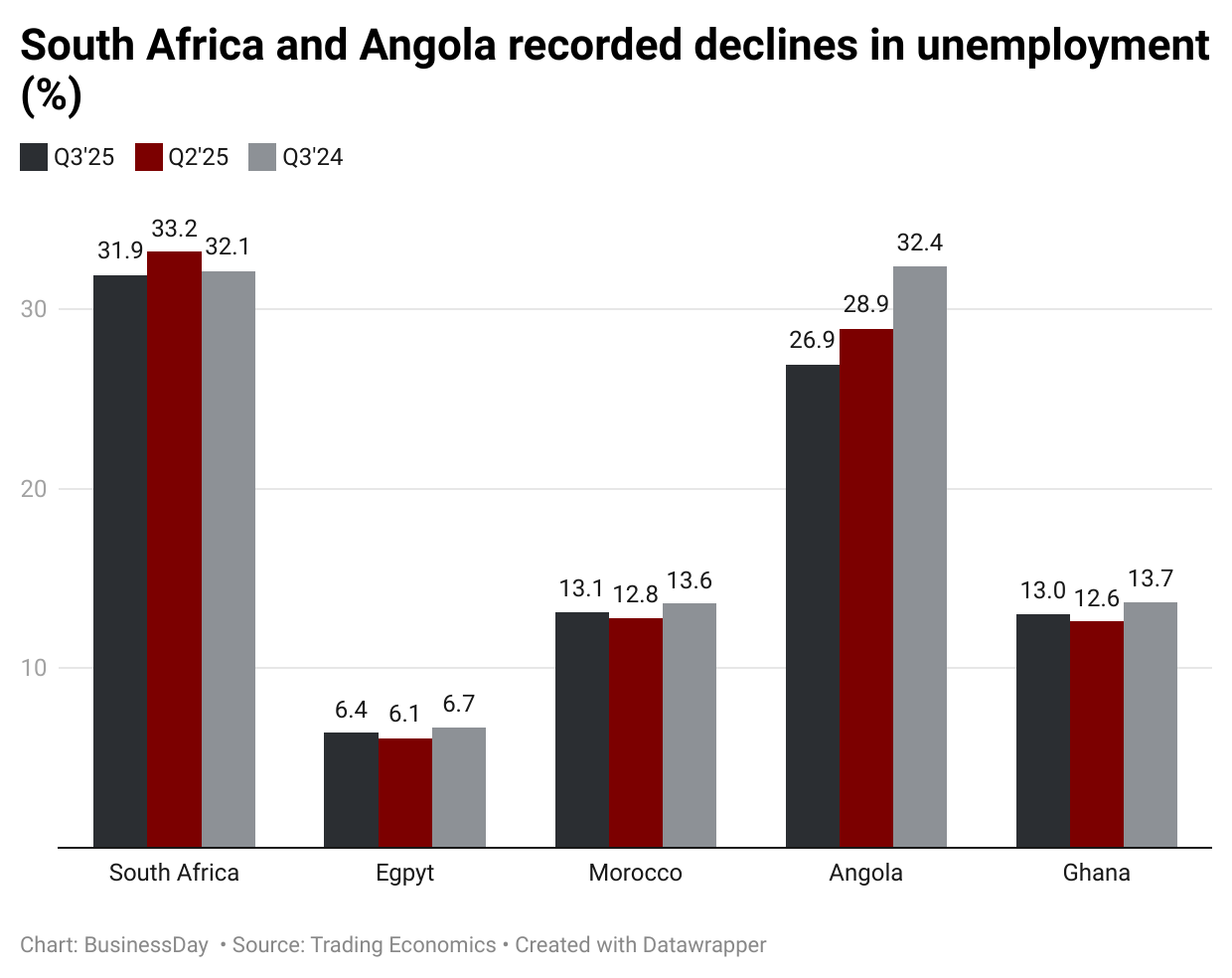

Labour markets: South Africa, Angola recorded declines in unemployment

While inflation eased, AfricaŌĆÖs labour markets told a more sobering story. The continentŌĆÖs recovery in 2025 remained largely job-poor, particularly in large economies.

South Africa recorded a rare bright spot. The unemployment rate fell to 31.9 percent in Q3 from 33.2 percent in Q2ŌĆöthe first improvement this year and the lowest since late 2024.

The rebound defied fears that the 30 percent US tariffs under President Donald Trump would trigger job losses. Gains in construction, social services, and trade, alongside improved electricity supply, supported employment.

Angola also reduced unemployment to 26.9 percent in Q3, its lowest level since Q4 2023, boosted by diversification efforts, public works programmes, and formalisation of informal activities.

However, unemployment rose in Egypt, Morocco, and Ghana. EgyptŌĆÖs jobless rate increased to 6.4 percent, MoroccoŌĆÖs to 13.1 percent, and GhanaŌĆÖs to 13.0 percent. Even MoroccoŌĆÖs impressive inflation control failed to translate into job creation.

Stock markets: Frontier exchanges steal the spotlight

AfricaŌĆÖs equity markets outperformed global peers in 2025. According to DabaFinance, the PanAfrica Index ŌĆö averaging dollar returns across 17 exchanges ŌĆö surged more than 41 percent in the first nine months, beating major developed-market indices.

While South AfricaŌĆÖs JSE remained the continentŌĆÖs largest exchange, the fastest gains came from smaller frontier markets.

The Malawi Stock Exchange led Africa with a staggering 251 percent gain in dollar terms as of December 22, according to real-time trading platform African Markets. Market capitalisation rose sharply, pushing the market cap-to-GDP ratio above 120 percent ŌĆö a rare level for African exchanges.

Ghana followed as the GSE Composite Index gained about 132 percent year-to-date, driven by strong banking stocks, lower fixed-income yields, and improved macro stability. Financial equities returned 89 percent by mid-December, reflecting renewed investor confidence.

Adding to GhanaŌĆÖs market momentum, last week First Atlantic Bank ŌĆö a 30-year-old indigenous financial institution ŌĆö listed on the GSE, becoming the first listing in over seven years. The move underscores growing investor confidence and adds depth to the local equity market.

ZambiaŌĆÖs market rose by 105 percent, Nigeria gained 55.9 percent, and South Africa advanced 55.5 percent. Botswana posted the least returns of 9.85 percent, with Mauritius seeing a negative performance.

Currency markets: Ghana and Zambia lead AfricaŌĆÖs FX turnaround

Several African currencies strengthened in 2025, supported by improved terms of trade, foreign exchange reforms, stronger export receipts, and a softer US dollar.

Ghana and Zambia emerged as the continentŌĆÖs strongest currency performers.

The Ghanaian cedi appreciated by more than 20 percent in the first eight months, reversing a 19 percent depreciation in 2024. According to the World Bank, tighter monetary and fiscal policy, higher cocoa and gold prices, and restored investor confidence following debt restructuring underpinned the rally.

Read also:┬ĀFCTA cracks down on pantaker markets over rising solar streetlight thefts

Bank of Ghana data also show that the average interbank exchange rate strengthened to 11.02 cedis per dollar in November from 14.97 in January, representing a 23.5 percent appreciation year to date.

The currencyŌĆÖs appreciation helped push inflation into single digits for the first time since 2021, easing to 9.4 percent in September. The disinflation trend deepened in November, with inflation falling further to 6.3 percent ŌĆö marking nine consecutive months of deceleration.

ŌĆ£The speed of GhanaŌĆÖs disinflation reflects a rare alignment of tight macro policy, improved FX inflows, and restored investor confidence,ŌĆØ SBM Intelligence said in a recent report, noting that the International Monetary FundŌĆÖs disbursements under the $3 billion Extended Credit Facility further boosted sentiment.

ZambiaŌĆÖs kwacha gained about 16 percent, supported by progress on debt restructuring and lower oil import costs. Inflation slowed to 10.9 percent in November, the lowest since August 2023.

But South SudanŌĆÖs pound and EthiopiaŌĆÖs birr were the weakest performers, each depreciating by more than 10 percent amid export disruptions and FX market strains.