As 2025 draws to a close, Sub-Saharan Africa (SSA) finds itself at a crossroads. The macro numbers point to modest but steady growth ŌĆö yet beneath the surface lie divergent stories: vibrant digital booms, resurgent agribusiness experiments, early wins in energy and infrastructure, and lingering structural fragilities. The winners, laggards and hidden value creators are becoming clearer. For investors, consultants and policymakers, this is a moment to choose where to back away from optimism ŌĆö and where to double down on strategy.

The landscape: Steady growth, persistent risks

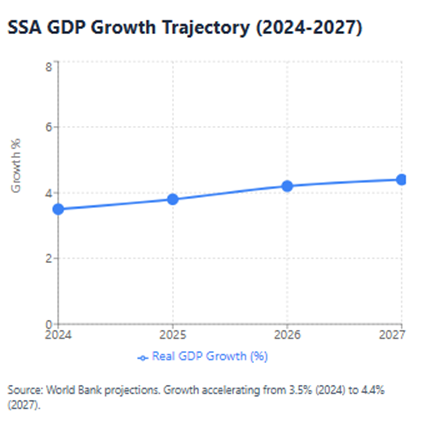

Analysts at the World Bank now project real GDP growth for SSA at about 3.8% in 2025, up from 3.5% in 2024, with forecasts pointing to further acceleration toward 4.4% in 2026ŌĆō2027. Several major economiesŌĆöincluding those covered by the European Bank for Reconstruction and DevelopmentŌĆÖs (EBRD) 2025 Regional Economic ProspectsŌĆöare expected to grow by roughly 4.7% this year. Inflation, which plagued many economies in the post-pandemic period, has eased significantly across the region; central banks are cautiously lowering policy rates to revive domestic demand. However, under the surface, the supply-side strains remain acute: poorly maintained infrastructure; high energy costs; anaemic structural transformation; persistently high informal employment; and slow job creation relative to rapidly expanding labour forces. These contradictions define the 2025 story ŌĆö and also its biggest opportunities.

Read also:┬ĀCanada reaffirms commitment to strengthen bilateral agreements with African Nations

Who is growing: Digital, agritech & infrastructure-linked sectors

1. Digital economy, fintech & tech-driven services

Perhaps the clearest success story of 2025 is AfricaŌĆÖs tech renaissance. Across fintech, agritech, AI, e-commerce and digital service firms, innovation is accelerating. The continentŌĆÖs tech ecosystem ŌĆö despite a small dip in external funding in 2024 ŌĆö remains one of the most resilient globally. The potential is vast. According to estimates presented at global industry forums this year, emerging technologies such as AI, the Internet of Things, big data analytics and digital platforms could contribute as much as US$1.5 trillion to AfricaŌĆÖs GDP by 2030. This shift is not just theoretical. Telecommunication providers are expanding capacity; satellite-internet deals are spreading broadband deeper into rural zones. For example, in late 2025, a major telecom across Southern Africa ŌĆö leveraging low-Earth orbit satellite technology ŌĆö announced expansion plans to reach underserved rural customers. For investors and strategists, this means high-conviction opportunities in digital infrastructure (data centres, fibre networks, and satellite broadband), fintech & payment rails, AI-powered agritech, cloud services, and e-commerce logistics. The risk is no longer just market demand ŌĆö itŌĆÖs delivery, execution and regulation.

2. Agribusiness & agricultural modernisation

Agriculture remains central to SSAŌĆÖs economy. In 2025, African leaders underscored agriculture as a growth engine ŌĆö especially if paired with innovation, mechanisation, better value chains and investments. The logic is simple: millions depend on farming for livelihoods, but production remains low-efficiency and fragmented. This creates massive upside for actors who can deliver mechanised farming, improved seed varieties, supply-chain linkages, storage, processing and market access. This yearŌĆÖs renewed focus on agricultureŌĆöespecially value-added agribusiness rather than raw subsistence farmingŌĆöis a signal for investors and development finance agencies: there is room for scalable models, agri-SMEs, agro-processing, cold-chain logistics, and input supply networks.

Read also:┬ĀVC investments in African startups rebound to three-year high

3. Infrastructure, energy and public investment projects

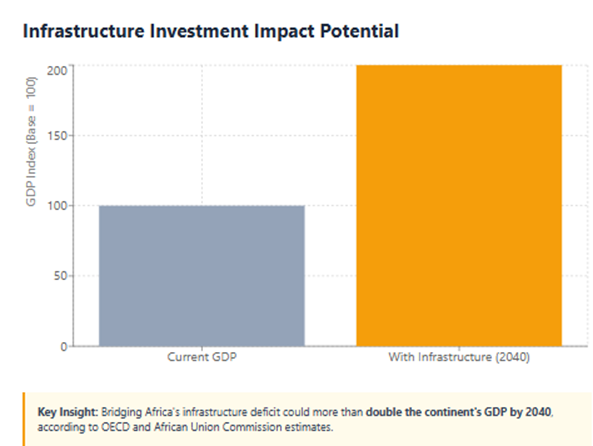

Across SSA, infrastructure remains the biggest constraint on industrialisation and long-term growth. The latest reports from the Organisation for Economic CoŌĆæoperation and Development (OECD) and the African Union Commission say that bridging AfricaŌĆÖs infrastructure deficitŌĆöfrom roads and ports to power grids, transport corridors, digital networks and logistics hubsŌĆöcould more than double the continentŌĆÖs GDP by 2040. Supporting this shift, development banks are already committing capital. For instance, the African Development Bank (AfDB) this month announced a US$1.78 billion financing package for energy, transport and water projects in a Southern African economy, setting the tone for similar deals across the region. Investors and funds willing to engage in long-term infrastructure financing, publicŌĆōprivate partnerships (PPP), renewable energy, water & sanitation, urban transport and logistics can capture valueŌĆöespecially as governments shift from aid dependence to trade and investment-led models.

4. State-owned and sovereign wealth funds: Internal capital going to work

A headline in December rang more than a bell ŌĆö it may be a signal: African state-owned institutions now manage nearly US$1 trillion in assets. Rather than relying solely on foreign aid or external equity flows, this pool of domestic capital is increasingly being directed toward infrastructure, public investment, and catalytic projects. Five new sovereign wealth funds (SWFs) launched in 2025 alone ŌĆö across Botswana, Eswatini, Kenya, DR Congo and Nigeria (states included). This shift signals that the era of reliance on foreign concessional finance may be waning; Africa is beginning to mobilise internal resources. For investors, fund managers and strategists, that means opportunities to co-invest with SWFs, target long-term infrastructure, energy or industrial deals, and benefit from privileged access to state-level mandates.

Read also:┬ĀAfrican startupsŌĆÖ corporate VC hits three-year peak with 44% jump in deals

Who is struggling ŌĆö And where smart intervention could help

1. Traditional manufacturing & industrials under stress

Despite broad-based GDP growth, many manufacturing firms remain stuck. Low capacity utilisation, unreliable power supply, high cost of raw materials (especially imported), foreign-exchange volatility and supply chain disruptions continue to throttle output and competitiveness. Recent data show many factories operating at 30ŌĆō50% capacity even in 2025. This structural weakness has consequences: low employment growth, weak job creation as economies expand, and an inability to produce at scale. The manufacturing sector ŌĆö long viewed as an engine for industrialisation ŌĆö remains fragile. The opportunity lies in turnaround strategies: captive power solutions (renewables + mini-grids), local raw-material sourcing, backward integration, supply-chain financing, and operational optimisation. Firms, investors and turnaround experts willing to invest in firm-level capabilities may find deep value here.

2. Jobs crisis despite growth

While economic activity expands, employment growth lags dangerously behind. According to the World BankŌĆÖs 2025 Africa Pulse, SSA must create wage-paying jobs at scale for a working-age population expected to grow by over 600 million over the next 25 years. Yet only a fraction of new entrants find formal-sector employment. This structural challenge ŌĆö a demographic boom without accompanying high-quality jobs ŌĆö remains the continentŌĆÖs greatest risk. Without aggressive private-sector expansion, upskilling and support for SMEs, growth risks failing the social test.

┬Ā

Where smart capital, strategic advice and policy support could make a difference

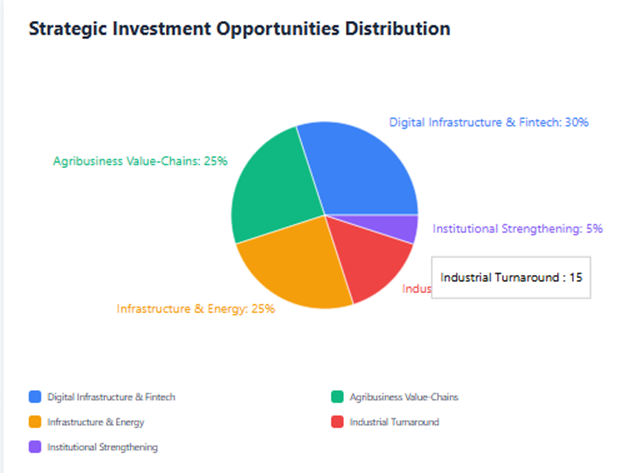

1. Digital infrastructure & fintech ecosystem build-out

Investments in fibre networks, data centres, cloud services, satellite broadband and mobile-finance rails can deliver outsized returns. Supporting rural connectivity & inclusive fintech ŌĆö especially targeting agritech, micro-entrepreneurs, cross-border remittances and digital credit ŌĆö remains a low-hanging fruit. Advisors and funds that bundle capital with execution support ŌĆö from regulatory navigation to go-to-market strategy ŌĆö stand to benefit most.

2. Agribusiness value-chain development

Agritech, mechanised agriculture, input supply networks, cold-chain logistics, agro-processing, export-oriented farming and rural service centres ŌĆö these are areas crying out for investment. Strategic capital that works beyond planting, linking farmers to markets, processing produce and enabling exports can create jobs, raise output, and build resilience. Donor agencies, development finance institutions (DFIs), private-equity firms and impact investors playing here can help transform agriculture into a reliable growth pillar rather than a subsistence activity.

3. Infrastructure & renewable energy projects

Roads, ports, water, power, broadband ŌĆö SSAŌĆÖs infrastructure deficit remains huge. But 2025ŌĆÖs renewed commitments from development banks, SWFs and governments reflect shifting priorities. Private capital ŌĆö especially via PPPs and blended finance ŌĆö can be catalytic. Clean energy (solar, hydro, mini-grids), water infrastructure, transport corridors and logistics hubs will yield long-term returns if execution is disciplined.

4. Industrial turnaround & local supply-chain integration

Manufacturing may be struggling, but there is value in rehabilitating viable firms. Opportunities exist in renewable-powered captive generation, raw-material import substitution, supply-chain finance, local sourcing, backward integration, modern management practices and export-readiness. Investors prepared to back firms (or clusters) with long-term capital and management support may unlock value that global capital often overlooks.

5. Institutional and governance strengthening and local capital mobilisation

AfricaŌĆÖs emerging sovereign wealth funds, pension funds and institutional investors now hold nearly US$1 trillion in assets. That capital needs effective deployment. Investments in governance capacity, project selection, transparent procurement, risk management, and development of pipeline-ready projects will help channel funds into high-impact, high-return ventures.

Advisors, fund managers and local financial specialists who can de-risk investments, structure deals and monitor implementation stand to play a critical role.

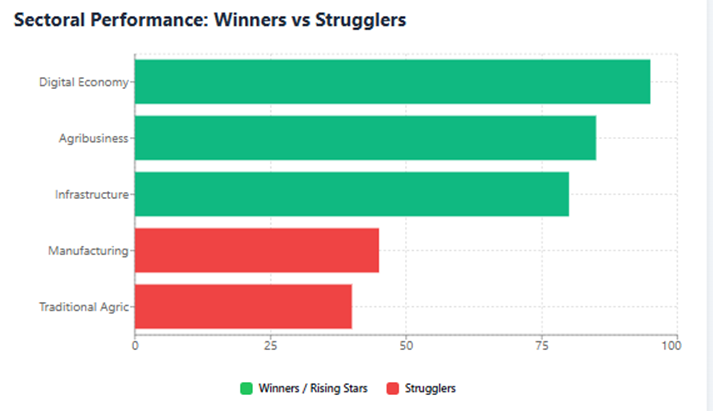

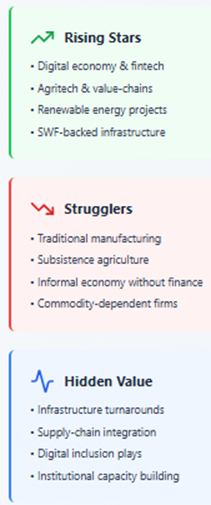

Winners, strugglers and the shape of the next decade

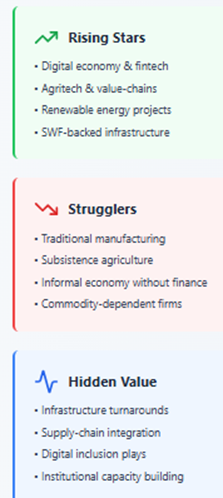

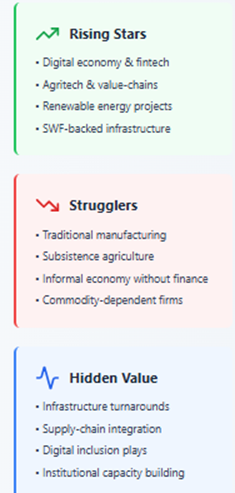

Winners / Rising stars: Digital economy (fintech, data, connectivity), agritech and agricultural value chains, renewable energy and infrastructure projects, fintech-enabled SMEs, digital services, and firms tapping SWF / pension fund capital.

Strugglers: Traditional manufacturing, conventional agriculture without value-add, many gig/informal-economy participants without access to formal finance, and countries or firms dependent on volatile commodity cycles.

Hidden value creators: Investors and operators willing to combine capital with executionŌĆöespecially in underserved sectors like infrastructure, renewable energy, agribusiness, logistics, local manufacturing, and digital inclusionŌĆöstand to capture outsized returns over the next 5ŌĆō10 years.

Read also:┬ĀWhy the 2025 MIPAD Awards set the agenda for influence in Africa and the diaspora

Conclusion: 2025 is not a rebirthŌĆöItŌĆÖs a recalibration

Sub-Saharan Africa in 2025 is neither collapsing nor surging. It is recalibrating. The macro fundamentals are stable enough to support steady growth, but structural problems remain entrenched. The path forward is not through miracles, but through strategic capital, disciplined execution, and institution-building. For those with patience, local knowledge and a willingness to invest beyond short-term gains, the region offers fertile ground for transformation. Transformative opportunities are not just in headline sectors ŌĆö they lie in repairing supply chains, building infrastructure, enabling digital inclusion, boosting agriculture, and transforming how the continent produces, trades and services itself. Smart capital should not seek shortcuts. It should seek system-wide value by investing in the people, infrastructures and institutions that will shape AfricaŌĆÖs next economic chapter. Because if 2025 has taught us one thing, itŌĆÖs that the coming decade will not be about fast booms, but sustainable rebuilds.

┬Ā

Dr. Oluyemi Adeosun, Chief Economist, BusinessDay