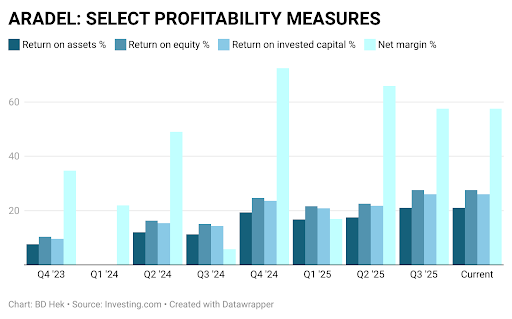

| As the trading floor of the Nigerian Exchange (NGX) bustles with deals, shares of oil and gas firms steal the limelight. In this scene, Aradel Holdings Plc (Aradel) has risen as a showpiece of the country’s developing capital markets. Thus, when six relatives of Adegbite Falade, Aradel’s managing director, bought ₦205.5 million worth of the oil firm’s shares recently disclosed in a regulatory filing with the NGX, the transactions became a litmus test for the budding corporate governance standards and regulatory enforcement capabilities in Africa’s most populous economy. The trades involving 293,600 Aradel shares worth c.₦205.5 million were not flagged as a scandal but have thrown the firm into a spotlight that fuses family allegiance with regulatory checkup. Listed on the NGX Main Board by introduction on October 14, 2024, the integrated energy company with interests in upstream exploration, midstream refining, and downstream distribution swiftly gained investor attention with its flush assets. And thus did Olanike Arinola Falade capture 175,900 shares for ₦123.1 million to lead five other kins of Adegbite in the family share purchase romp at a time when Aradel’s shares had dipped from post-listing highs and are now trading around ₦700, price still mirroring a market capitalisation above ₦3 trillion, nonetheless. |

|

| Textbook Dealings, Compelling Optics These purchases appear as your classic insider dealings on the surface – promptly notified as per the requirements of the Securities and Exchange Commission (SEC), NGX rulebook, and even Aradel’s own insider trading policy, published in October, 2024. But peeling back the layers reveal greater gaps in Nigeria’s capital market governance. With two immediate questions flowing from the filings. First, were the Aradel’s CEO kith acting entirely independently and within closed-period rules, blind to privileged information? Second, were the disclosures timely and complete enough for the market to judge that independence? The regulatory architecture already suggest two strong responses for both fronts. The issuer should provide evident and timely notification and necessary explanation. Then, the SEC should provide appropriate scrutiny. Positive Signals; Call for Caution Aradel’s shares were resolute at ₦690 in late November 2025 as crude prices topped $80 a barrel and domestic refining push under President Tinubu’s reforms gained traction. Staff purchases like HR partner Bimpe Oladerin’s 18,980 shares at ₦514 paint a scene flush with internal optimism. Yet, a market aiming at global standards cannot bargain with transparency. And as gazes at $1 trillion GDP by 2030, capital markets will be critical for infrastructure funding. Episodes like Aradel’s will test resolve. To ensure that family fortunes don’t come at the expense of fair play, SEC should probe not just compliance but also intent. Access Holdings’ N40 Billion Recharge: Tonic for Nigeria’s Banking Chaplet Valuation, Other Implications Having been afflicted by opacity, ineptitude, and political obtrusion for decades, the NNPC had worsened Nigeria’s fiscal woes. A listing would compel audited disclosures, independent board surveillance, and market discipline. Primed by the return to profitability, a listing would ride on the momentum gained and attune to the PIA’s vision of a commercial entity. A delay may blow this momentum as global energy transitions dun smart funding for renewables and refining. |

|

| However, the listing will remain illusory without a collaboration between market regulators and fiscal authorities. The Securities and Exchange Commission (SEC) has been mandated by the nascent Investments and Securities Act (ISA) 2025 to protect investors and maintain market transparency. This regulatory charter is a needed assurance for NNPC’s smooth sail to the market. Simultaneously, the fiscal authorities must show the political will to go at the established interests and political meddling that have historically tormented the firm. Executives were recently sacked in a key organisational overhaul, signalling readiness for a commercial phase. Yet, defeating decades of systemic murkiness seems the biggest government dilemma.

Ultimately, the benefits of an NNPCL listing would be transmogrifying for Nigeria’s capital market. Beyond ballooning the market size and spurring the attraction of foreign direct investment, it would enhance market liquidity, set governance benchmarks for other state firms like NLNG, encourage private sector listings, formalise businesses and support economic stability. This way, NNPCL would undergo alchemy from a fiscal drain into a market jewel. NGX chairman Umaru Kwairanga had told Nigerians in a Kano symposium in June 2025 that the Exchange has been positioned to attract oil and gas giants like NNPC and Dangote Petrochemicals, arguing that this would aid the realisation of President Bola Tinubu’s $1 trillion economy dream by 2030. Thus, the time for stalling is over. NNPCL must list now or fade into irrelevance in a competitive global arena. |