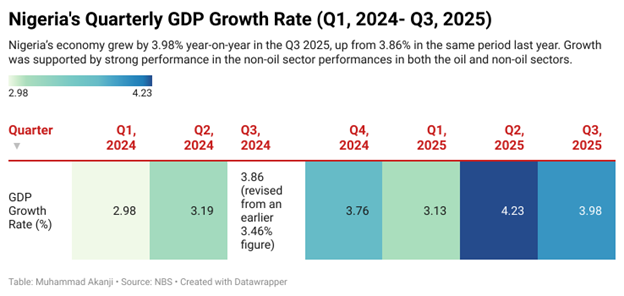

Nigeria’s Q3 2025 GDP report paints a picture of sustained rebound- albeit not comfort. With output rising 3.98% year-on-year, the growth was almost entirely borne by agriculture and industry, while services lagged. Is this GDP growth a sign of real progress- or merely an accounting victory masking a deeper crisis of unemployment, weak productivity, and widening inequality?

On paper, this seems like a rolling recovery from the doldrums of Q1, 2024. Farms expanded with season-favourable weather and crop yields, factories turned out more cement, steel, and food products for post-festival construction and consumption, and manufacturing’s modest rebound boosted headline growth.

But the gains mask troubling fragilities: non-oil sectors remain tethered to climate and global commodity cycles. In contrast, the services sector- which supports most of Nigeria’s urban workforce- shows little sign of revival. Credit remains tight, inflation sneaks on with core price pressures, and foreign-exchange volatility looms. Meanwhile, jobless youth and overstretched SMEs may find no solace in output statistics.

The billion-dollar-plus question then: Is this growth real and sustainable- or a brief bounce built on fragile foundations? And more critically: Who is this growth working for, and who is it leaving behind?

Headline readouts and growth drivers

The expansion in the economy marked one of the strongest quarterly performances since the post-pandemic rebound driven largely by the non-oil sector. On a quarter-on-quarter basis, GDP slowed by an estimated -5.9%, reflecting both seasonal agricultural strength and improving industrial utilisation. According to the NBS Q3 2025 GDP report, the non-oil sector remained the backbone of the economy, contributing over 90% of total output, with real growth of roughly 4.5%, significantly outpacing the oil sector.

Agriculture was the surprise stabiliser, expanding by around 2.2%, supported by late-season harvests, better rainfall distribution, and targeted interventions in grains and livestock. The industrial sector also strengthened, growing by 3.5–3.7%, driven by a pickup in cement, food processing, and manufacturing sub-activities. This aligns with rising energy supply consistency and improving FX liquidity for select manufacturers.

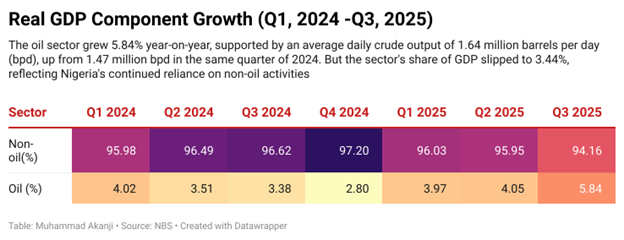

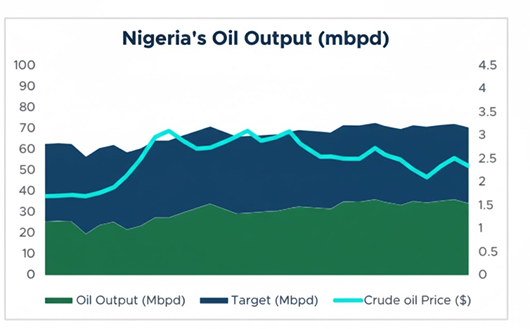

Oil GDP, though still fragile, showed mild improvement. OPEC and NNPC data indicate crude production averaged 1.62–1.68 mbpd in the quarter (including condensates), up from the sub-1.3 mbpd levels earlier in the year, providing a marginal lift to overall output.

Services retained the growth crown, expanding by over 4%, buoyed by financial services, telecoms, trade, and transport recovery. NBS also noted that agric. Grew by 3.77% in the quarter under review

Together, these short-run drivers created the headline momentum- but they also raise a bigger question: How durable is this pattern in an economy still battling inflation, FX imbalance, and weak job creation?

The labour and inclusion check

Without any gainsaying, the growth driven by agriculture, industry and services raises a critical question: is this growth job-rich, or jobless? The labour numbers suggest a troubling disconnect between output gains and meaningful employment.

According to the latest International Labour Organization (ILO) data, youth unemployment (15–24 years) stands at 6.5%, even as overall unemployment fell to 4.3%. The bulk of employed Nigerians, 93% , remain in informal, low-productivity work. Rural agriculture still hires roughly 30% of the labour force, while manufacturing absorbs just about 12.7%.

So far, the Q3 rebound appears output-rich but employment-poor. Gains in GDP are concentrated in sectors with low employment elasticity or informal labour. As a result, real wages, underemployment and youth joblessness remain problems, particularly as inflation erodes purchasing power.

Without deliberate policy to channel growth into job-creating, formal sectors, and investments in skills, credit, and formalisation, Nigeria risks sustaining growth without inclusion, where GDP rises, but living standards stagnate.

Real risks under the surface

Furthermore, the growth masks deep structural vulnerabilities. On the price front, headline inflation, albeit recently easing, still hovers around double-digit, while core inflation remains sticky well above 16%.

Credit markets are under stress: despite a rate hold, tight liquidity remains. The banking system’s high reserve requirements and previous cash-reserve-rate hikes have squeezed private-sector lending, limiting business expansion, especially among SMEs.

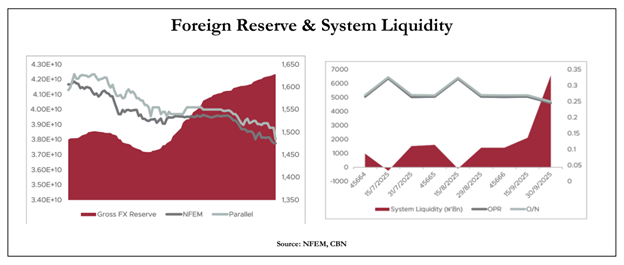

Foreign-exchange stability is fragile. FX volatility and uncertain oil receipts threaten naira value and dollar-denominated debt servicing – a growing concern as public debt edges toward 50–55% of GDP.

On the fiscal side, pressure is mounting. Tax revenues and FAAC allocations fluctuate with global oil prices and FX shocks, while debt-service obligations rise.

If oil receipts slump, subsidy reforms kick back, or climate-driven crop failures hit, the non-oil sectors that support Q3 growth will buckle. In that scenario, the fragile gains could unravel fast, exposing the economy to stagflation, credit crunch, and deeper inequality.

Policy imperative and market implication

The latest round of GDP data underscores a clear message: growth is improving, but consolidation now depends on smart, coordinated policy. With inflation still elevated and liquidity tight, stronger monetary–fiscal alignment is imperative—especially around FX management, revenue mobilisation, and targeted social transfers to cushion vulnerable households.

The data also strengthens the case for investment incentives in agriculture, manufacturing and digital services, the sectors driving over 95% of real growth. Fixing persistent data gaps- labour statistics, productivity tracking, and state-level sectoral output—will be critical for more credible policy signals.

For investors, the implications are mixed. Equities may see selective gains in banking, agribusiness, and telecoms, supported by rising non-oil activity. Fixed-income markets could remain cautious as yields stay high amid inflation uncertainty and CBN liquidity tightening. FX markets will react to policy clarity: sustained reforms could stabilise naira expectations, while hesitation may widen volatility.

Overall, the Q3 numbers offer momentum- but 2026 will reward only policies that convert growth into jobs, stability, and real investor confidence.