Fidelity Bank joined the list of banks paying interim dividends in 2022. It began with a modest N2.9 billion payout after H1 2022. By H1 2024, that figure had surged to N42.7 billion. The jump reflected the bankŌĆÖs strong earnings and rapid expansion in recent years.

That momentum paused in H1 2025. Despite posting a solid N132 billion net income, the bank did not declare an interim dividend. BusinessDay looks at why this happened.

A review of Fidelity BankŌĆÖs balance sheet provides clarity. The bankŌĆÖs retained earnings fell into negative territory, closing at -N74.2 billion as of June 2025. This decline was driven by the Central Bank of NigeriaŌĆÖs prudential guidelines on loan-loss provisioning.

Read also:┬ĀWhy Access Holdings may resume dividend payments after first pause in a decade

Section 4.4 of the guidelines is clear. When prudential provisions exceed IFRSŌĆÖ impairment charges, the difference must be moved from retained earnings to a non-distributable regulatory risk reserve. For Fidelity Bank, this rule triggered a huge transfer of N303.5 billion into the reserve. The move immediately eroded its distributable profits.

With this transfer completed, the bank cannot pay dividends for now. It will need to generate very strong profits in the coming years to rebuild its distributable reserve.

Why did this happen?

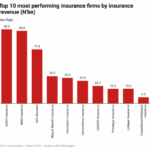

Fidelity Bank has been lending aggressively. As of H1 2025, it held a loan book of N4.85 trillion and customer deposits of N7.2 trillion. This gives it a loan-to-deposit ratio of 67.4 percent. For context, Access Holdings stands at 39 percent, GTCO at 44.1 percent, and Zenith Bank at 40.9 percent. Fidelity clearly leads in loan deployment.

This strategy accelerated between H1 2024 and H1 2025. During this period, the bank grew its loan book from N3.75 trillion to N4.85 trillion. That is a 29 percent jump, equal to N1.1 trillion in new loans. With this growth came rising credit risks.

The bankŌĆÖs loan-loss provisions reflect this pressure. Total impairments increased from N195.6 billion at the start of 2025 to N207.7 billion by June. These provisions cut across Stage 1 performing loans, Stage 2 under-performing loans, and Stage 3 impaired loans.

In summary, Fidelity BankŌĆÖs fast loan growth, rising impairments, and regulatory provisioning rules combined to push its retained earnings into the negative. This forced the temporary halt in dividend payments, even in a year of strong profits.

This situation does not exist in isolation. It also reflects the CBNŌĆÖs March 2025 directive instructing all banks to pause dividend payments until they clear their forbearance exposures. A June 2025 report by Renaissance Capital Africa shows that Fidelity BankŌĆÖs forbearance exposure stood at 10 percent of its gross loans, a sizeable position relative to its loan book.

Some peers, such as UBA, Zenith Bank, and Access Holdings, have since resolved most of their forbearance-related obligations and resumed dividend payouts. For Fidelity Bank, however, the combination of high forbearance exposure, rising impairment provisions, and the heavy transfer to regulatory reserves paints a different picture.

Read also:┬ĀNNPC remits N15.9trn to FG in royalties, dividends in 2024

Recapitalisation efforts are hit

The dividend suspension also complicates Fidelity BankŌĆÖs capital-raising efforts. Investors typically favour banks that offer consistent dividend payouts, especially in a market where returns are a major incentive for participation.

For Fidelity, this challenge is even more pronounced. The bank still needs to raise about N195 billion to meet the CBNŌĆÖs N500 billion minimum capital requirement. However, from all indications, the bank is not targeting a capital raise from the market, as it looks to issue 20 billion new shares in a private placement.