Let’s talk about money. Not just the numbers in your bank account, but the vast, flowing river of global capital—trillions of dollars moving between lenders and borrowers every day.

- Trust as Economic Capital

- How Credibility Shapes Lending Decisions

- Why Integrity Lowers Borrowing Costs

- Covenants and Behavior Signals

- The Cost of Weak Credibility

- Africa’s Credibility Gap in Capital Markets

- Steps to Strengthen Credibility

- The Role of Policymakers in Building Trust

- Rebuilding Trust after Credibility Loss

- Conclusion: Why Credibility Predicts Financial Outcomes

- About The Author:

We would like to think that this system runs purely on numbers, be it interest rates, credit scores, or collateral sum. But beneath the spreadsheets and legal documents lies something far more human: that is “trust”.

Think about the last time you lent a friend money. Your decision was not just based on their income; it was based on your belief that they would pay you back, as at when due, as promised. The Lending Ecosystem and Capital markets are the same, just on a colossal scale. The invisible asset that makes it all work is credibility. And as we will see, this integrity is not just a “nice-to-have”; it is a direct lever that lowers borrowing costs and unlocks opportunity.

Trust as Economic Capital

In finance, we record buildings, equipment, and cash on a balance sheet. But we don’t have a line item for “trust,” even though it is one of the most valuable asset a company or country can possess. This trust is a form of economic capital and determines the level of capital you can access and the costs of that capital varies, based on your perceived degree of trust and brand value.

It is the trust in your availability of capital that assures a lender that a borrower will honour their obligation, even when no one is watching. A high level of this trust capital means lower “transaction costs”—less need for expensive lawyers, stringent monitoring, and draconian contracts. The bond of trust itself becomes the most efficient enforcement mechanism. As the World Bank has pointed out, trust is a critical factor in financial development and economic growth, acting as the glue that holds complex market interactions together.

How Credibility Shapes Lending Decisions

When a bank or an institutional investor like Pension Funds considers a loan, they are doing more than analyzing financial ratios. They are conducting a deep credibility assessment, to determine the borrower’s ability to repay the loan, as at when due.

They look at a borrower’s history: Have they always made payments on time? Have they been transparent in their communications, especially during tough times? Is their governance strong, do they have an independent board that holds management accountable? This due diligence is all about measuring the intangible. A company with a spotless reputation for integrity presents a lower “model risk”—the risk that their future behavior will be unpredictably different from their past. This makes them a safer bet.

Why Integrity Lowers Borrowing Costs

So, how does integrity translate into cheaper money? It is simple, through risk and reward.

A lender facing a credible, trustworthy borrower doesn’t need to price in a high risk of default, deception, or covenant manipulation. They can offer a lower interest rate because they are confident that the loan will be repaid without a costly fight to recover it back. This credibility borders on character and that is why Character is viewed as the tenet of Credit. It is the foundation and backbone on which credit is based and a lack of it results in default. This is not just theoretical; it is a fundamental principle of debt pricing. The higher the perceived trust, the lower the risk premium demanded by the market.

Covenants and Behavior Signals

Covenants—those clauses in a loan agreement that require the borrower to do (or not do) certain things—and are often seen as restrictive. But in the context of trust, they are better understood as communication tools.

A borrower who readily agrees to reasonable covenants is signaling something; “I am so confident in my discipline and transparency that I welcome this oversight.” This principle, even though not written down, can be inferred. They are building trust. Conversely, fierce resistance to standard covenants can be a red flag, suggesting that the borrower plans to engage in risky behavior(s) they do not want the lender to see.

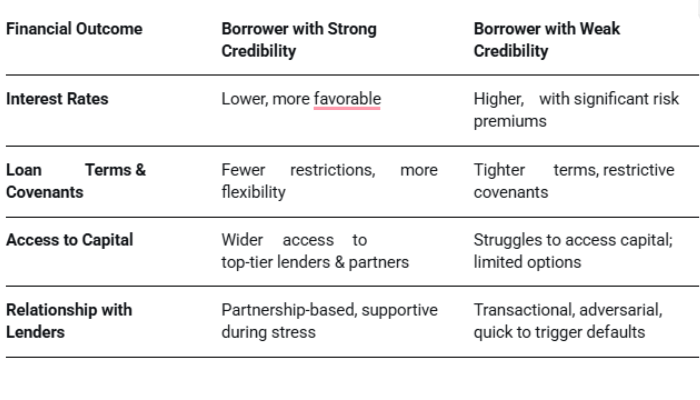

The Cost of Weak Credibility

The flip side is a harsh reality. When credibility is weak, capital becomes expensive, if available at all, as it also limits and sometimes, restricts complete access to credit, as we see in the United States, were your credit score determines your access to loans. Lenders, fearing the loss of their principal amounts, must protect themselves. They do this by charging higher interest rates, demanding more collateral, and imposing tighter, more restrictive covenants.

This phenomenon can create a vicious cycle, as the high cost of capital stifles growth and innovation. It also weakens the borrower’s financial position and ability to fund new ventures, even though laudable and innovative, and in turn further erodes credibility. It is a financial death spiral.

Let’s make this contrast clear:

Africa’s Credibility Gap in Capital Markets

This discussion hits home particularly hard in many African markets. The continent is not short of innovative entrepreneurs or viable projects. The challenge is often a credibility gap that inflates the cost of capital, making the continents cost of borrowing, in comparison to its European counterparts, extremely high.

International investors, burned by experiences of political instability, contract repudiation, or unpredictable regulatory shifts, often demand a higher risk premium. A Brookings Institution report on African sovereign debt highlights how perceptions of governance and political risk directly impact the interest rates countries pay on international bonds. This premium is not always about the inherent risk of the business project itself, but about the broader systemic trust deficit. This means that a brilliant entrepreneur in Lagos or Nairobi may pay double the interest for a loan than a comparable counterpart in a more “trusted” market, not because their idea is worse, but because the systemic credibility is not there or is perceived as very low.

Steps to Strengthen Credibility

The good news? Credibility can be built, starting today. It is a strategic and intentional investment.

- Embrace Radical Transparency: Go beyond the minimum disclosure requirements. Share both good and bad news proactively.

- Honor Small Commitments: Trust is built in small increments. Consistently meeting small obligations builds a track record that compounds over time.

- Welcome Smart Covenants: View covenants not as burdens, but as tools to demonstrate your commitment to discipline and good governance.

The Role of Policymakers in Building Trust

Trust is not just a private sector concern. Policymakers and governments are the ultimate architects of the credibility landscape. By strengthening contract enforcement, ensuring judicial independence, and promoting fiscal transparency, they can lower the “country risk” premium for its teeming populace, thus, making it easier and cheaper to access credit.

Initiatives like open public procurement and robust anti-corruption frameworks are not just moral imperatives; they are economic policies that directly lower the nation’s cost of borrowing and free up capital for development.

Rebuilding Trust after Credibility Loss

What if trust has been broken? Recovery is difficult but possible. It requires a visible, verifiable, and sustained commitment to reform.

This means openly addressing past failures, overhauling governance structures (e.g., appointing independent board members), and engaging respected third-party auditors to verify the new path. It’s a costly process, but the alternative in being locked out of affordable capital is far more expensive.

Conclusion: Why Credibility Predicts Financial Outcomes

In the end, finance is not just a science of numbers; it’s a social science. The numbers tell you what happened, but credibility tells you who you are dealing with and what they are likely to do next. A strong credibility balance sheet is the ultimate predictor of financial resilience. It is what allows businesses to weather storms, entrepreneurs to build empires, and nations to develop. It turns scarce capital into abundant opportunity and stimulates growth and access to capital.

So, whether you are a business leader, a policymaker, or an individual, remember: your most valuable financial asset isn’t just what you own, but the trust you’ve earned. Invest in it wisely.

About The Author:

Prof. Prisca Ndu who holds four doctorate degrees in Credit Management, Banking and Finance, Leadership and Management and Artificial Intelligence, is a social impact advocate, multi-sector entrepreneur and a professor of practice in management and finance. An alumnus of the University of Ibadan, Lagos Business School, Harvard Business School, London Graduate School, Institute of Management Development, INSEAD and Robert Kennedy College, Switzerland, amongst others. She sits on the Board of several companies including INDECO, KREENO Consortium, BHLA Awards, and many more. She was listed in 2017 among the most influential people of African descent by the United Nations and is passionate about Nation Building.

Email: priscan@kreenoholdings.com and WhatsApp Only: +234 902 148 8737