It is close to sunset in the protracted hustle for AfricaŌĆÖs telecoms subscribers, and this is more evident in Nigeria more than anywhere else. In AfricaŌĆÖs leading economy, MTN Nigeria and Airtel Africa now clutch more than 85 per cent of the market, with MTN commanding nearly 52 per cent and Airtel pulling 34 per cent. This leaves Globacom tucking at 12 per cent and 9mobile, now rebranded as the rebranded T2, scratching below 2 per cent. As the concentration intensifies, smaller rivals bleed subscribers. 9mobileŌĆÖs base has crashed from 22 million in 2015 to just 2.7 million in July 2025. Booming data demand and infrastructure investments may have driven the duo, but analysts are calculating the cost to AfricaŌĆÖs leading economy.

LagosŌĆÖs investors and AbujaŌĆÖs policymakers view the consolidation as double-ended blade. Telecoms contribute significantly to GDP as industry revenues jumped 33 percent over 2023 to hit Ōé”5.33 trillion in 2024. Only MTN produced Ōé”1.41 trillion in value in half-year 2025. The imperium has spurred solid capex, with MTN and Airtel flushing billions into 5G and fibre networks and fostering digital inclusion.

As the dominance dialled up investor appeal for increased valuation, MTN NigeriaŌĆÖs market capitalisation leaped to Ōé”10 trillion by mid-2025, with its shares rising 136 per cent to N472 to make it a top stock of the local bourse. Dual-listed Airtel Africa posted half-year revenue rise of 26 per cent to $3 billion, with EPS surging by 70 per cent to depict NigeriaŌĆÖs massive part in its portfolio. Both made a combined gain of Ōé”5.5 trillion in market value between January and August 2025.

But risks lurk ŌĆō regulatory scrutiny or economic downturns could constrain multiples, especially if consumer loyalty tumbles on the survival backlash. Consumers are already feeling the squash. A landmark tariff hike this year, the first in over a decade, raised average revenue per user (ARPU) by 32 per cent for MTN and Airtel in the second quarter. But Nigerians already burdened by economic headwinds paid the price amidst higher data and voice costs with fewer alternatives. While it is not all blues from the duopoly as its scale could herald better network quality and coverage, industry regulator NCC must wear its anti-thrust lens to guarantee affordability in a market where mobile is lifeline for banking and business.

So, what does the MTN-Airtel duopoly portend? For investors, it is a high-signal bet; For Hek, the grab vows efficiency but threatens stability; for Nigeria, it is a call for vigilant oversight to keep the lines open.

Ella Lakes: Betting Bold on NigeriaŌĆÖs Agribusiness Renaissance

NigeriaŌĆÖs Ella Lakes prospectus landed with a thud literal and metaphorical. Having been on a resurgence path recently, the NGX-listed oil palm and cassava company is seeking to raise N235 billion by selling 18.8 billion shares to the public at N12.50 a pop. The documents say that investors have until December 5 to snap the shares from the offer, which opened on November 10, 2025. Ella is seeking to exploit investor appetite for agribusiness as Nigeria pushes to curb tame the scourge of food imports. The offer is the companyŌĆÖs most ambitious capital raise to date, is a bet that NigeriaŌĆÖs agribusiness can be industrialised at scale.

Ella Lakes was once a floundering fish farmer. Now it has swung to high-margin crops, cashing in on NigeriaŌĆÖs massive arable land. AfricaŌĆÖs largest palm oil importer, Nigeria spends billions yearly on imports even with its domestic potential. But as the Government aims to incentivise domestic production leap from 300,000 tonnes to 700,000 by 2027, Ella Lakes is positioning itself in the middle of this bang. Money from the share sale, already approved by the Securities and Exchange Commission (SEC), will be used to expand plantations and processing facilities, doubling cassava output and integrating value chains.

The purchase of Agro-Allied Resources and Processing Nigeria Limited (ARPNL) is the pivot of this strategy, which will see a push from fragmented, low-productivity farming to an integrated model that captures additional portions of the value chain and boosts margins. This vertical play echoes successful models like Presco and Okomu Oil, which have delivered fabulous returns by gripping everything from seedlings to refined products. Funds will also be deployed to upgrade its milling technology and raise palm oil extraction capacity by 50 per cent. For a sector where smuggling and low yields run wild, this could furnish efficiencies and lift margins from the current precarious levels.

Ella Lakes is pushing a shift from restructuring to aggressive growth through this share sale, hoping to diversify revenue away from volatile commodity prices. Policy makers and investors see the offering beyond a clever balance-sheet engineering but more as a live test NigeriaŌĆÖs capacity to convert bold agrarian plans into steady production and cash flow. As such, success could attract more foreign capital to underfunded farms. A flub will serve the cautionary note that lavish capital raised on ambition can be wrecked by logistics, governance and execution failures. The offer is priced at slight a premium to its market rate, and tests market confidence in CEO Chuka MordiŌĆÖs vision.

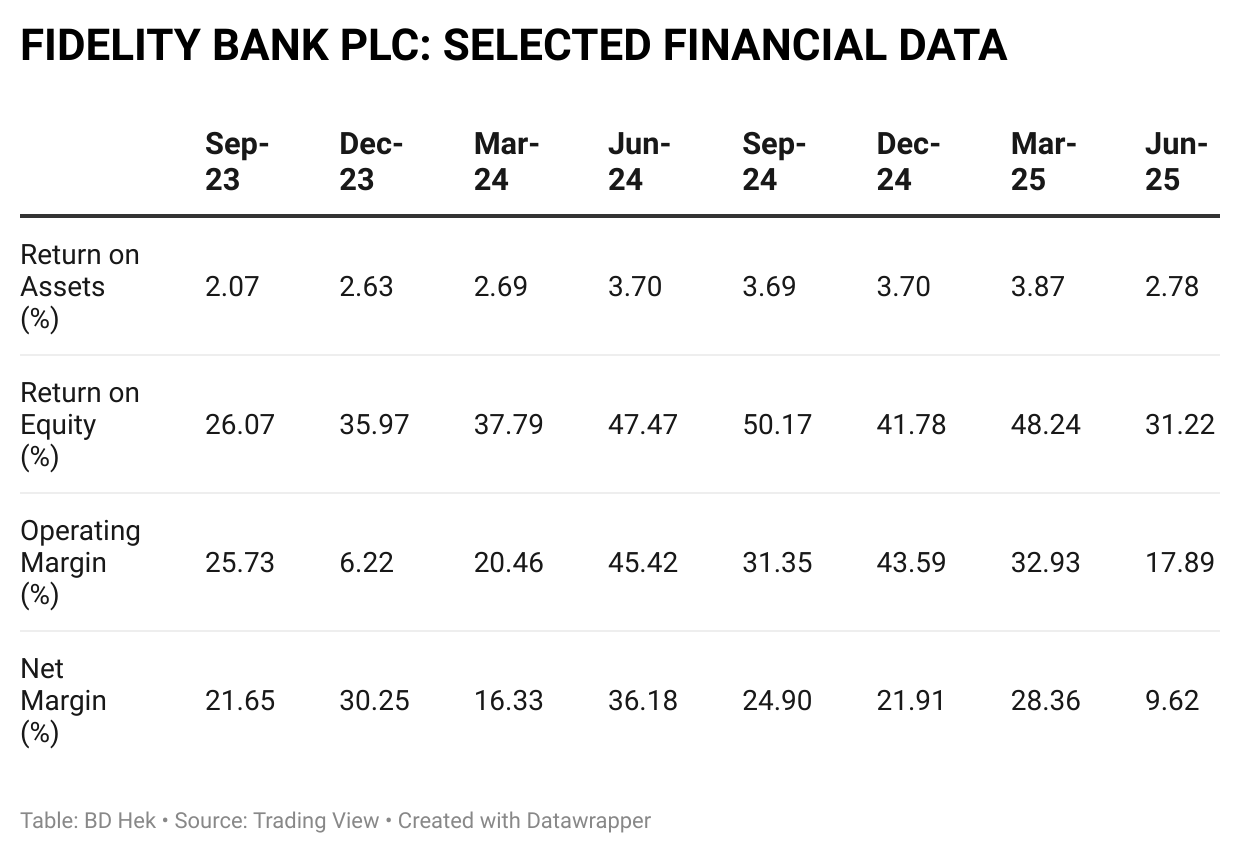

Fidelity Bank Plc: Capital Crunch, Sagecom Sting, and the Race to Recapitalise

NigeriaŌĆÖs Fidelity Bank is traversing turbulent waters as the second-tier lender battles close to Ōé”194 billion shortage under the recapitalisation rules of industry regulator, the Central Bank of Nigeria (CBN), which demand that international banks must have minimum capital of Ōé”500 billion. The timeline is first quarter of 2026, so the second-tier bankŌĆÖs boardroom is abuzz with hushed urgency, as the bank labours to touch a target that stretches even the biggest lenders in AfricaŌĆÖs most populous economy.

Mixed is the picture painted by FidelityŌĆÖs half-year results, with gross earnings jumping 46 per cent to N748.7 billion and after-tax earnings slumping 15.4 per cent to N135.1 billion. This antithetical scenario was created by the handshake among inflated rates, rising operating costs, and a windfall tax gnaw of N2.8 billion. Net interest margins were unmoved from last period, but fee income growth succumbed to batter from impairments and provisions. These have sent the jitters to investors. And why not? They have already booked a six-month loss of percent given delays in earnings release as regulatory watch breeds sector qualms.

This is a turmoil brewed by a bruising long-running legal brawl with Sagecom Concepts Limited. Analysts say that a Supreme Court judgement on this in April 2025 means that Fidelity could be forced to patch a financial hole of almost N200 billion ($138.8 million). This is almost half of the bankŌĆÖs tier-1 capital. Fidelity has since disputed this figure, pegging its exposure in the judgement at just N14 billion, but respite peeks from afar.┬Ā Realising that market does not trade on judicial nuance, Fidelity has booked N34.8 billion litigation provision in its 2025 half-year financials. Rising 1,433 per cent from previous, this spike, according to directors, will have no consequential impact. Hek sees a benignant settlement with Sagecom, or a looming overhang that will strain liquidity with full enforcement.

Now, FidelityŌĆÖs shareholders stand on a tripod of discomfort supported by rising capital needs, uncertain legal liabilities and weakening profitability. The bank is looking to the capital market to plug its N194 billion capital hole. Shareholders have already sanctioned a private placement of up to 20 billion shares, almost twice the volume of its oversubscribed N127.1 billion hybrid offer last year, to buffer tier-1 capital without significant dilution in a recapitalisation furore where peers like GTCO and Zenith have raised billions. FidelityŌĆÖs fate is now the bob of a unidirectional pendulum of capital raise.┬Ā Success will swing it to tier-1 status; failure will swing it to CBN intervention or merger talks.