A new analysis of state finances has revealed that at least ten Nigerian states are heavily exposed to foreign debt, with repayments now far exceeding what they can afford from their internally generated revenue (IGR) and monthly federal allocations.

According to data from the Debt Management Office (DMO) and the BudgIT 2025¬ÝState of States¬Ýreport, states such as Kaduna, Edo, Bauchi, Cross River, and Adamawa are among the worst hit, with their foreign debt now outweighing their entire annual revenue capacity.

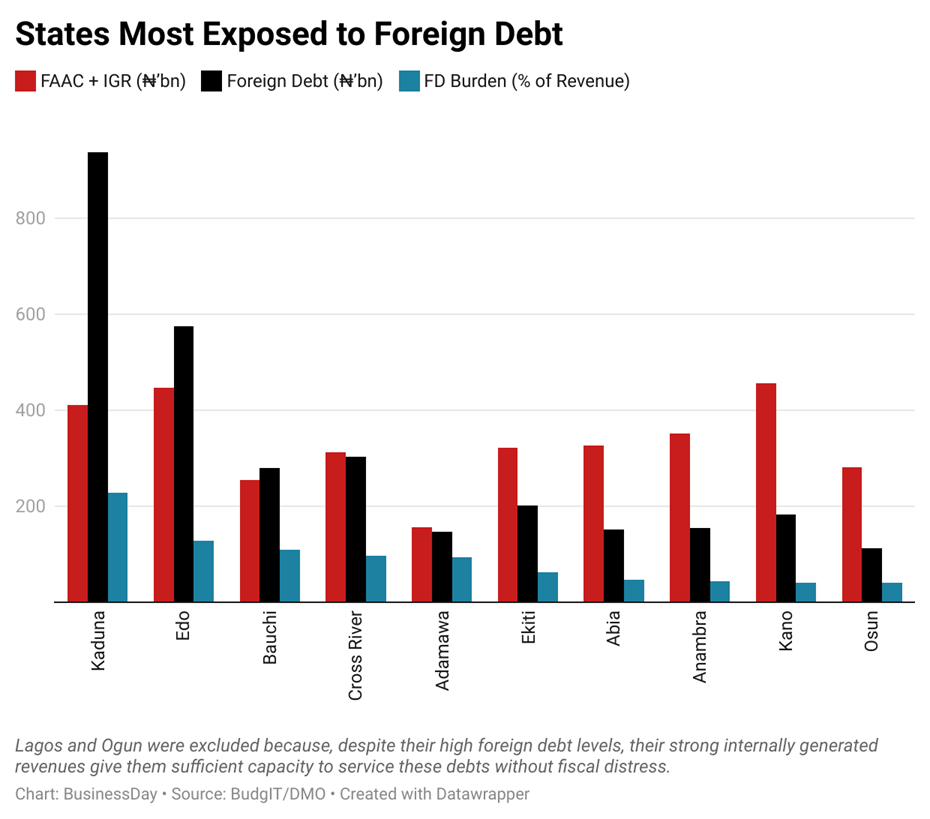

Collectively, these ten states hold foreign debts valued at over¬Ý$1.9 billion, roughly¬ÝN2.8 trillion¬Ýat the current exchange rate of¬ÝN1,500 per dollar,¬Ýan amount that dwarfs their combined 2024 IGR and FAAC receipts.

Methodology and assumptions

A BusinessDay analysis evaluated each state‚Äôs Foreign Debt Burden Ratio (FDBR), defined as the proportion of foreign debt to total annual revenue (FAAC plus IGR). Using the 2024 figures from the DMO and the BudgIT, the analysis assumed an average exchange rate of¬ÝN1,500 to $1 to convert dollar loans into naira.

The assumption also held that all states maintained stable FAAC inflows and consistent IGR performance without new borrowing. Any state whose foreign debt exceeds 50 percent of its total revenue base was classified as “high-risk,” while those above 100 percent were deemed “fiscally distressed.”

The results: 10 most exposed states

The findings are stark. Kaduna State tops the list, with foreign loans of $625.1 million (N937.6 billion) against a total annual revenue of¬ÝN411 billion. This means its external obligations are equivalent to 228 percent of its total income, more than two years‚Äô worth of FAAC and IGR combined.

Edo State follows closely with $383.05 million (N574.6 billion) in foreign debt, representing 129 percent of its¬ÝN447 billion revenue. Bauchi State also faces significant pressure, with $186.81 million (N280 billion) in loans, amounting to 110 percent of its¬ÝN255 billion income.

Other states in critical positions include Cross River (97 percent), Adamawa (94 percent), and Ekiti (63 percent), all of which carry debt loads that could wipe out future allocations if repayment pressures mount. Abia, Anambra, and Kano round out the top ten, each with ratios ranging between 40 and 50 percent.

Experts warn of looming fiscal strain

Economists say the numbers expose the widening fiscal vulnerability across Nigeria‚Äôs subnationals. Muda Yusuf, Chief Executive of the Centre for the Promotion of Private Enterprise, told¬ÝBusinessDay¬Ýthat the debt levels reflect a crisis of prioritisation and poor fiscal management.

“Many of these states borrowed in foreign currency without building export capacity or stable IGR buffers,” Yusuf said. “At today’s exchange rate, their repayment obligations have nearly tripled, leaving little room for capital expenditure.”

Uche Uwaleke of Nasarawa State University explained that the depreciation of the naira means states with heavy dollar exposure are bleeding from both ends.

“Most states took concessional loans when the exchange rate was four hundred naira to the dollar. With one thousand five hundred today, debt service has become unbearable,” he said. “Unless there is debt restructuring or a bailout, some will default on obligations by 2026.”

At fiscal-responsibility retreat, Asishana Okauru, former Director-General of the Nigeria Governors’ Forum, observed that many states lack foreign-exchange buffers or clear repayment plans and called for tighter borrowing limits and coordinated creditor engagement.

Beyond the numbers

While Lagos and Ogun are not immune to foreign debt exposure, both remain financially strong. Their IGR bases,¬ÝN1.26 trillion and¬ÝN195 billion respectively, give them a far greater ability to service foreign loans without depending on Abuja.

Lagos alone generates more revenue internally than 30 other states combined. Its diversified economy, built on ports, property, and services, provides a cushion against foreign exchange shocks. Ogun, though smaller, benefits from a strong industrial corridor along the Lagos–Ibadan axis.

“Debt alone doesn’t spell trouble; it’s about the capacity to pay,” Yusuf added. “Lagos and Ogun have what most states lack: steady inflows and a broad tax base. That’s why they can manage exposure that would cripple others.”

By contrast, smaller states such as Cross River, Ekiti, and Adamawa lack the fiscal muscle to absorb currency shocks and face rising risks as exchange rates worsen.

Outlook

As Nigeria’s debt service burden expands amid currency weakness, foreign debt exposure will likely remain a key risk factor for state governments.

Unless reforms are implemented particularly around revenue diversification, transparency, and prudent borrowing many subnationals could find themselves trapped in a new wave of fiscal distress.

For now, Kaduna, Edo, Bauchi, and Cross River remain the clearest signals that Nigeria’s debt problem has shifted from Abuja to the states.