How Africa’s startups climb the venture ladder…

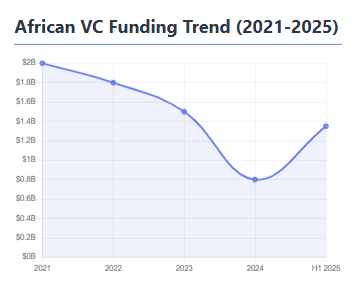

In the grand theatre of venture capital, the journey from Series A to C represents less a smooth incline than a gauntlet of increasingly demanding tests. Each funding round is a different contract with different metrics, risks and expectations. Understanding these distinctions—and learning from recent African success stories—matters profoundly for founders building scalable enterprises and for investors seeking defensible returns. The past decade has witnessed Africa’s transformation from an experimental venture market into a credible asset class. African startups raised over $2 billion in 2021, creating a cohort of unicorns and demonstrating that African companies could achieve global-scale valuations.

Yet the subsequent correction has been instructive: total venture capital funding reached just $1.2 billion in the first half of 2025, roughly half the average seen between 2022 and 2024. The market has matured, and capital now flows only to companies that demonstrate genuine unit economics and paths to profitability.

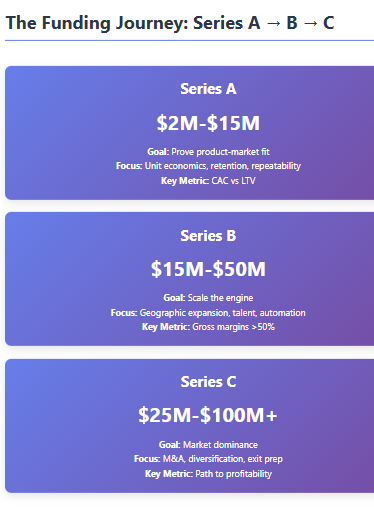

Series A: Proving product-market fit

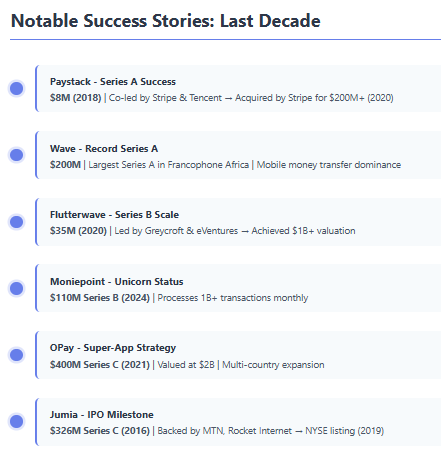

Series A, typically raising $2 million to $15 million, is where ideas graduate into businesses. Investors expect demonstrable product-market fit, repeatable revenue models and the ability to deploy capital efficiently for growth. The metrics that matter: customer acquisition cost, lifetime value, retention cohorts and gross margins. Paystack’s $8 million Series A round in 2018, co-led by Stripe and Tencent, exemplified this stage perfectly.

The Nigerian payments company had already proven significant transaction volumes and strong merchant retention—precisely the traction that justifies institutional capital. Two years later, Stripe acquired Paystack for over $200 million, validating the Series A thesis that capital would accelerate an already-working engine. More recently, Wave raised a landmark $200 million Series A from Stripe, Sequoia Heritage, Founders Fund and Ribbit Capital, the largest in Francophone Africa at the time. This outlier round demonstrated exceptional product-market fit in the mobile money transfer market, serving millions of users across Senegal and neighbouring markets with demonstrably low transaction costs.

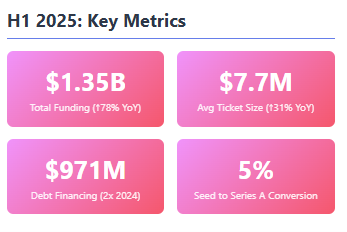

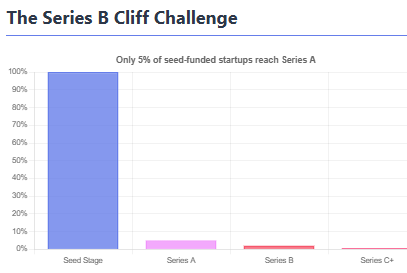

The challenge for African founders remains acute. Data suggests conversion rates from Seed to Series A hover around 5%—far below global averages. Investors now demand gross margins above 50% and clear operational efficiency before committing capital. In a market where seed-stage activity surged with 82 early deals recorded in the first half of 2025, marking a 30% increase year on year, and seed funding climbing 40% to $171 million, the real bottleneck is proving that early traction can become sustained, profitable growth.

Series B: Scaling the engine

Series B, ranging from $15 million to $50 million, shifts focus from validation to velocity. The capital fuels geographic expansion, senior talent acquisition, and process automation to sustain explosive growth. Success here requires proven unit economics at scale and clear channel repeatability. Flutterwave’s $35 million Series B in 2020, led by Greycroft and eVentures, funded aggressive expansion across Africa and new product development, propelling the company toward its eventual $1 billion-plus valuation.

Similarly, Kuda raised $55 million in Series B funding at a $500 million valuation, using the capital to scale its challenger banking model across Nigeria’s retail banking landscape. Moove secured a $100 million Series B round led by Uber, validating its revenue-based vehicle financing model for gig economy workers.

The company has now raised over $409 million, demonstrating investor confidence in scalable fintech models addressing real infrastructure gaps. Yet Series B represents what many call the “Series B Cliff”—a persistent funding gap in Africa’s ecosystem. Late-stage rounds have nearly vanished, with only one Series C recorded in Q2 2025.

For Nigerian firms especially, macroeconomic volatility and foreign exchange risk complicate large, long-term commitments from global VCs. Founders increasingly turn to Development Finance Institutions and debt financing to bridge this gap, diversifying capital sources beyond pure equity rounds.

Series C and beyond: Market dominance

Series C rounds, typically $25 million to over $100 million, fund market consolidation, product diversification and preparation for major liquidity events. At this stage, investors scrutinise governance structures, audited financials and credible exit pathways—whether through IPO, strategic acquisition or secondary sales. OPay’s $400 million Series C in 2021 valued the company at $2 billion, reflecting confidence in its super-app strategy combining payments, transport and commerce across multiple emerging markets.

Moniepoint secured over $10 million from Visa, bringing its Series C raise to over $120 million, cementing its position as Nigeria’s leading payments and banking platform for small businesses. Jumia’s $326 million Series C in 2016, backed by MTN, Rocket Internet and AXA, represented a war chest for continental dominance, funding deep logistics networks and payment infrastructure that culminated in a 2019 NYSE listing—still one of Africa’s most significant tech exits.

The exit environment remains challenging. Strategic acquisitions by global players—Stripe’s purchase of Paystack, WorldRemit’s $500 million acquisition of Sendwave—have proven more frequent than public listings. Founders and later-stage investors must build businesses attractive to strategic buyers while maintaining governance standards that support eventual public market entry.

The current landscape: Recovery and resilience

The funding environment in 2025 signals cautious optimism. African startups secured $1.35 billion in funding during the first half of 2025, marking a 78% increase from the $800 million raised in the same period in 2024. June 2025 emerged as a pivotal moment, with startups raising $365 million that month alone—the strongest monthly performance in nearly a year. Yet the recovery is uneven.

The average ticket size rose to $7.7 million, up 31% year on year, while the median deal climbed to $3.3 million. Investors are concentrating capital on proven founders with scalable business models rather than spreading risk thinly. Debt financing exploded in the first half of 2025, with $971 million raised—double last year’s total, reflecting founders’ strategic pivot toward diversified capital structures.

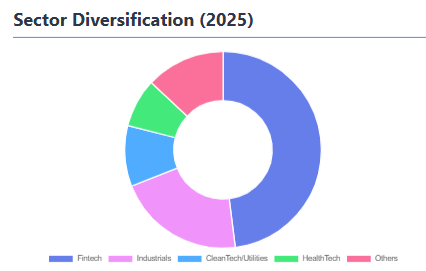

Sectorally, fintech remains dominant but the ecosystem is diversifying. Industrials accounted for 21% of deals, driven by startups tackling logistics, mobility and manufacturing inefficiencies, while utilities and CleanTech attracted 10% of total funding. This diversification reduces concentration risk and demonstrates Africa’s venture market is maturing beyond payments into infrastructure and real-economy solutions.

Insights for would-be organisations

At Series A: Quantify everything. Present retention cohorts, customer acquisition cost versus lifetime value analysis, and clear unit-economics theses. Demonstrate operational capability and a 12- to 18-month roadmap tied to specific milestones the new capital will unlock. Build board-ready metrics from day one.

At Series B: Develop robust hiring plans, market expansion playbooks and unit-economic sensitivity analyses. Show that incremental capital produces predictable returns. Be transparent about operational weaknesses you will address with capital and talent. Strategic partnerships—with banks, telcos or global platforms—have proven recurrent multipliers for African companies.

At Series C: Institutional investors demand experienced boards, audited financials meeting international standards, and multiple exit scenarios. Demonstrate resilience under adverse macroeconomic conditions and articulate why your company will command a premium in M&A or public markets.

Raise the capital you need to clear the next milestone set—not the maximum cheque you can secure. Use capital to buy predictability through systems, talent and distribution rather than vanity growth metrics. Keep governance structures and clean financial records from inception, not as an afterthought.

Lessons for would-be investors

At Series A: Underwrite the business model, not just the vision. Scrutinise gross margins and capital efficiency. Companies with margins above 50% and clear paths to profitability warrant attention. The failure rate remains high, so back founders who demonstrate early operational rigour and data discipline.

At Series B: Assess execution risk and management depth. Look for repeatable customer acquisition channels, defensible unit economics and the right leadership bench to manage complexity. In frontier markets, structure deals that support regional diversification to mitigate single-currency exposure.

At Series C: Demand crystal-clear exit pathways and governance structures that align incentives. Run scenario models under plausible macro shocks—foreign exchange volatility, regulatory changes, interest rate movements. Value strategic optionality: does this investment become more attractive if a global platform wants African distribution?

The venture capital ladder in Africa rewards teams that combine product insight with financial discipline. The market has proven generous to companies that turn scale into staying power, but the bar for later rounds is higher than ever. For founders and investors alike, the lesson is straightforward: raise smart, spend smarter, and always build the exit a buyer would welcome.