|

Getting your Trinity Audio player ready...

|

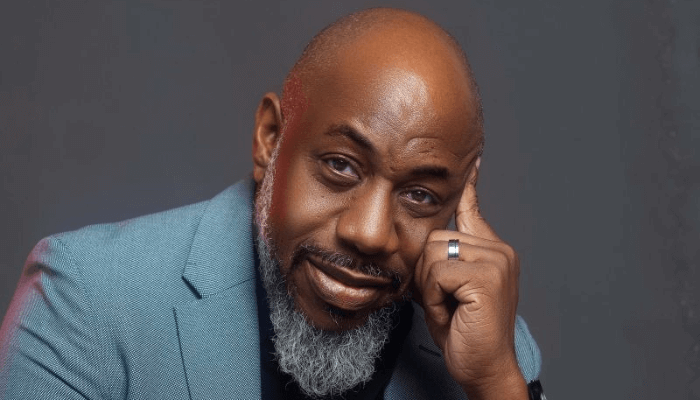

In Nigeria’s turbulent foreign exchange landscape, speed, trust, and transparency have become the new currencies of trade. For many businesses, settling cross-border payments remains a slow and uncertain journey—often exposing them to risk, inefficiency, and the opacity of informal FX channels. At the centre of this challenge is Alpha Tayo-Olugbode, Founder and Chief Executive Officer of ZitraPay, who is building a new kind of financial bridge designed to connect local businesses to global markets through smarter, compliant, and faster payment infrastructure. A seasoned risk and compliance leader with over 14 years of experience across Africa, the U.S., and global markets, Tayo-Olugbode previously served as Head of Risk & Compliance at Yala and Float (a YC-backed fintech), where he developed frameworks that balanced innovation with trust.

In this interview with Folake Balogun of BusinessDay, he discusses how ZitraPay is addressing Nigeria’s liquidity and FX challenges through transparency and structure, why trust remains the ultimate differentiator in fintech, and how the company’s long-term vision could redefine Africa’s cross-border payment infrastructure. Excerpt:

Nigeria’s FX market remains volatile and opaque. What gap did you see in the system that convinced you that ZitraPay could build a sustainable business around liquidity and treasury solutions?

Nigeria has faced an FX access problem for as long as I can remember, with banks often struggling to meet genuine business demands. Many importers I know have shared how difficult it can be to pay suppliers abroad, sometimes waiting days or even weeks after a tedious process. Some have even fallen into the hands of scammers while searching for alternatives.

The real issues come down to three things: availability of FX, trusted partners, and speed. ZitraPay was built to address these pain points by providing a more reliable, transparent, and efficient way for businesses to move money across borders without the usual friction.

Many businesses with Form M approvals still can’t access USD through banks. How does ZitraPay bridge that gap without falling into the pitfalls of informal FX channels?

We bridge that gap through strict compliance, licensed banking partners, and simplified documentation. Every transaction on ZitraPay is backed by proper documentation. After initial KYC, your Form M and invoice are enough to support your “Purpose of payment” purpose.

We only work with regulated and verified liquidity providers, ensuring that all transactions remain traceable and compliant. This structure allows us to move funds efficiently without crossing into informal or unregulated territory.

Your model charges slightly above bank rates, yet customers still prefer you. What exactly do they value most—speed, reliability, or trust—and how do you sustain that edge?

It’s a combination of all three, but trust is the foundation. Many Nigerian businesses have been burnt in the past, so trust doesn’t come easily. Once clients see consistency in payments delivered as promised, issues resolved quickly, and a human face behind the service, it increases their chances of staying.

We don’t just process payments; we build relationships. Reliability and speed sustain the trust we’ve built, and that’s what keeps businesses coming back.

With over $1 million in processed transactions within three months, how are you managing liquidity risk and ensuring compliance in such a tightly regulated environment?

The $1M+ monthly volume is quite small compared to industry peers. We’re intentionally scaling cautiously to get our risk models right.

As a team with strong risk management and compliance backgrounds, we take liquidity exposure seriously. Every trade is monitored cautiously & carefully. We constantly calibrate our payment routes to find the most secure and efficient options, and we maintain conservative exposure limits per transaction cycle. Our rule is simple: grow steadily, not recklessly.

Critics argue that fintechs like ZitraPay could amplify informal FX flows. How do you respond to that, especially given Nigeria’s sensitive monetary climate?

That’s a fair concern, but ZitraPay was actually built to make the process more transparent, not informal. Every transaction is traceable end-to-end.

We work exclusively through licensed partners across countries, follow global KYC and AML standards, and keep verifiable records for every client.

Our goal is to complement, not compete with, existing financial systems by bringing more structure and visibility to how cross-border payments are done.

Trust is a recurring theme in your messaging. How are you building verifiable transparency into your processes so that businesses and regulators can see ZitraPay as a credible partner rather than a workaround?

Transparency for us means visibility and accountability. Every transaction is documented, and clients can always verify their payment status and delivery timeline.

We also maintain proper records, follow due diligence on every client, and respond quickly to any compliance inquiry. Our goal is for both clients and regulators to see that ZitraPay is structured, not secretive.

As a risk and compliance veteran, you’ve worked at Yala and Float. What lessons from those experiences shaped your philosophy for balancing innovation with regulatory integrity at ZitraPay?

At Yala and Float, I learnt that innovation without structure doesn’t last. You can build the best technology, but if compliance isn’t part of your DNA, and if you are not leveraging networks to aid your growth, it will eventually collapse.

So at ZitraPay, we designed compliance as part of the product, not as an afterthought. Every feature we roll out is reviewed through the lens of compliance, documentation, and user experience. That’s how we have remained sustainable, and we plan to grow that way.

Beyond FX access, you’ve hinted at treasury management and fund repatriation. How do these additional services position ZitraPay as more than just a currency bridge, perhaps even as a new kind of financial infrastructure for SMEs?

ZitraPay isn’t just about moving money; it’s about managing it intelligently.

We help SMEs allocate funds across currencies and manage payables and receivables in multiple currencies. For exporters, our repatriation services help them bring funds back securely and compliantly.

In essence, we’re evolving into a financial infrastructure layer that helps businesses handle their global finances seamlessly, from payments to cash flow optimisation, without needing to build complex treasury systems themselves.

Your early traction shows strong repeat usage from sectors like tech, pharma, and auto trade. What insights are you gathering from these verticals that will shape your next phase of growth?

Each of these sectors values speed and reliability, but their needs differ.

– Tech companies focus on predictable payment cycles for international partners.

– With pharma companies, compliance and documentation are highly required because that industry is highly regulated.

– Auto traders prioritise competitive rates and fast settlements.

Our next phase is all about personalisation: building solutions that speak the language of each industry.

Looking ahead to Q1 2026 and beyond, how do you see ZitraPay evolving? Will you stay focused on Nigeria’s liquidity crisis or expand into regional markets facing similar bottlenecks?

For now, our focus is on deepening trust and efficiency for Nigerian businesses that need to pay contractors and suppliers globally. That mission continues into 2026.

However, the long-term vision is regional. Many African markets face the same liquidity and cross-border friction challenges. Once we’re confident in our model’s scalability, expansion will be a natural next step.