Across Nigeria today, from the quiet hum of church meetings to the noisy chatter of beer parlours, one topic dominates informal conversations: taxes. Since President Bola Tinubu signed the new Tax Reform Act into law on 26th June 2025, anticipation and anxiety have mingled in equal measure. For many citizens and business owners, the term “tax net” feels less like a fiscal concept and more like a looming trap.

The government aims to broaden the base, simplify compliance, and boost revenue. Yet beneath the optimism lies a paradox. The same reforms designed to make taxation more transparent and efficient could, if poorly executed, deepen the very burdens they seek to ease. This is the catch-22 of Nigeria’s new tax era – progress that risks tripping on its own ambition.

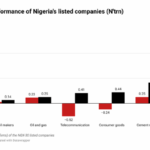

The 2025 Tax Reform consolidates more than a dozen outdated tax laws into four primary Acts: the Nigeria Tax Act (NTA), the Nigeria Tax Administration Act (NTAA), the Nigeria Revenue Service Act (NRSA), and the Joint Revenue Board Act (JRBA). It is a bold attempt to modernise the country’s tax architecture which embraces digital invoicing, real-time VAT systems, and simplified stamp duties. The intent proves to be noble but the outcome, however, will depend entirely on how the system is implemented.

Under the new law, businesses with an annual turnover below N100 million or fixed assets under N250 million are exempt from Company Income Tax (CIT), Capital Gains Tax (CGT), and the 4 percent Development Levy. On paper, this is relief. But once a business crosses these thresholds or even slightly, it becomes liable for multiple taxes, regardless of profit margins. For small and medium-sized enterprises (SMEs) such thresholds can quickly turn growth into punishment. Similarly, individuals earning below N800,000 annually are exempt from personal income tax, while those in higher brackets face a 25 percent marginal rate. While designed to promote equity, the measure could unintentionally encourage income concealment or disincentivise upward mobility.

For large businesses, the landscape grows even more complex. Capital Gains Tax has tripled from 10% to 30%, now aligning with CIT. The aim is to curb arbitrage, yet it also penalises asset-heavy companies seeking to restructure or divest. Multinationals with turnovers exceeding N50 billion must now maintain a minimum 15 percent Effective Tax Rate (ETR). Moreover, indirect offshore share transfers are now taxable, demanding tighter compliance and strategic restructuring of global holdings.

Then there is the digital challenge. All registered firms must adopt e-invoicing and real-time VAT systems, an important step toward transparency, but one that demands significant technical capacity. For many SMEs still dependent on manual bookkeeping, this transition could prove costly and cumbersome. Without proper support, these businesses risk penalties for non-compliance, not because of intent but because of technological incapacity.

The compliance burden could grow heavier still. SMEs will need to monitor turnover and asset growth carefully, invest in accounting software, and seek professional tax advice to avoid misclassification. Yet such expertise comes at a price. Ironically, reforms meant to simplify may end up squeezing the very enterprises that power local employment and innovation.

The reforms are not without opportunity. Companies maintaining qualifying thresholds can enjoy exemption from CIT and CGT, alongside a 5 percent annual tax credit on eligible capital expenditure for up to five years. The new flat N1,000 Stamp Duty, replacing the old ad-valorem system, will reduce uncertainty and cost in contract execution. Likewise, digitisation, if properly implemented, could make audits faster and less arbitrary which has been a long-standing concern for Nigerian businesses.

For individuals, however, the new system presents a mixed bag. Taxation now extends to worldwide income for Nigerian residents, including diaspora earnings. Higher tax rates for high-income earners may invite creative avoidance schemes, while the inclusion of low-value contracts under stamp duty expands the scope of potential liabilities. Compliance will require meticulous documentation and professional guidance, which also is an added pressure in an already strained economy.

Government communication will be crucial. The average Nigerian does not resist taxation; they resist opacity and harassment. The success of these reforms will depend on how transparently agencies like the Federal Inland Revenue Service, FIRS, which will become known as Nigeria Revenue Service, NRS, effective January 2026, and the Joint Revenue Board apply them. Citizens need clear guidance, not punitive surprise. Tax education through campaigns, workshops, and community outreach must be prioritised to bridge the knowledge gap.

Nigeria’s tax reform reflects a bold effort to move from a resource-dependent economy to a revenue-driven one. But reform without discipline risks futility. If executed with fairness, simplicity, and empathy, it could finally expand Nigeria’s tax base while encouraging investment. If implemented with inconsistency and bureaucracy, it may drive businesses underground and deepen distrust.

Taxation, in principle, is a social contract. Citizens fund governance, and the government guarantees transparency and service delivery. Breaking either side of that contract leads to disillusionment. For this reform to work, both sides must meet halfway with honesty, competence, and courage.

The real Catch-22, then, is not in the law itself but in Nigeria’s capacity to enforce it justly. The monk must indeed step out from under the hood, not only wearing the robe of reform but embodying its discipline, foresight, and integrity.