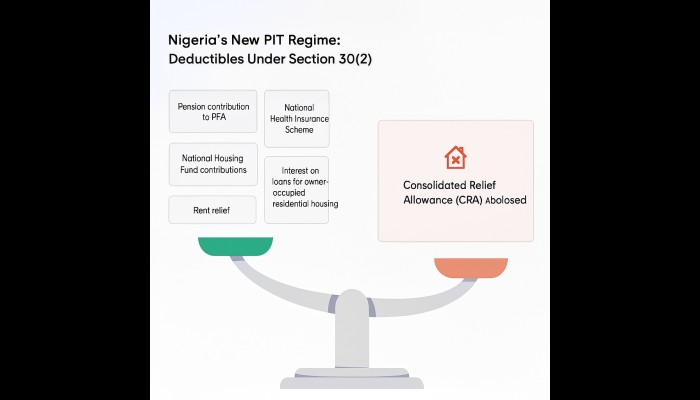

Nigeria’s personal income tax system has recently undergone significant reform. Previously, income earners benefited from a simple tax structure that offered a Consolidated Relief Allowance (CRA), automatically reducing the amount of tax payable. However, under the new Personal Income Tax (PIT) regime, that simplicity has been replaced by a more detailed and structured approach.

Rather than relying on automatic relief, workers must now pay closer attention to the specific deductions they are entitled to claim. The new framework introduces targeted allowances, such as rent relief and revised contribution deductions, making it essential for taxpayers to understand how these apply to them.

According to Section 30(2) of the Nigeria Tax Act, 2025 (Act No. 7), the following are deductible expenses that individual taxpayers can claim under the new personal income tax laws:

Contributions under the National Housing Fund (NHF)

Payments made by an individual during a year of assessment in respect of contributions to the National Housing Fund are deductible.

This deduction covers the mandatory 2.5 percent contribution of an employee’s basic salary to the NHF. By law, these contributions are tax-exempt, meaning the amount contributed is subtracted directly from gross income before tax is calculated.

Read also5 smart tax moves every Nigerian should make before 2026

The scheme is designed to pool resources to provide affordable mortgage loans to contributors.

Contributions under the National Health Insurance Scheme (NHIS)

Contributions made by an individual to the National Health Insurance Scheme are also deductible.

This provision allows taxpayers to deduct payments made toward the government’s national healthcare programme, which seeks to provide accessible and affordable health services. Just like the NHF, this deduction ensures that the portion of income allocated to mandatory public health insurance is not subject to tax.

Contributions under the Pension Reform Act

Contributions made by an individual under the Pension Reform Act qualify as deductible expenses.

This covers both the statutory minimum contribution, typically 8 percent of total emoluments by the employee, and any approved Additional Voluntary Contributions (AVCs), provided the AVCs are not withdrawn within five years.

This deduction encourages long-term retirement savings while reducing current tax liability.

Interest on loans for owner-occupied residential housing

Interest paid on loans obtained for the development of an owner-occupied residential house is deductible.

This incentive is aimed at promoting home ownership. It applies specifically to the interest portion of a loan used exclusively to purchase, build, or convert an individual’s first residential house occupied by them. Only the interest component, not the loan principal, qualifies for deduction.

Read also14 bold tax reforms set to energise Capital Market

Life insurance and deferred annuity premiums

Premiums paid for life insurance or deferred annuity contracts are deductible under the new law.

This includes annual amounts of any annuity or premium paid by an individual in respect of insurance on their own life or that of a spouse. To qualify, the premium must have been paid in the year preceding the year of assessment, and valid proof of payment (such as premium receipts) is required. The deduction supports long-term financial security planning.

Rent relief

Rent relief of up to 20 percent of annual rent paid, capped at N500,000, whichever is lower, is now deductible.

This is another addition under the new regime, offering relief for renters in place of the general CRA. Taxpayers must accurately declare the actual amount of rent paid and provide verifiable documents such as tenancy agreements and payment receipts, as tax authorities are empowered to request evidence of such claims.

The new PIT framework shifts Nigeria’s personal tax system from blanket relief to targeted deductions. To benefit fully, taxpayers must understand what qualifies as an eligible expense and maintain accurate records. In this era of claim-based relief, documentation and compliance are just as important as the deductions themselves.