Nigeria, often described as the “Giant of Africa,” once held the position as the continent’s largest and most diversified economy. Today, with a GDP of around $340 billion and a recent currency devaluation following the floating of the naira, the country faces a daunting challenge: reaching a $1 trillion economy. Achieving this milestone would not only solidify Nigeria’s influence in Africa but also enhance its global competitiveness and create meaningful economic opportunities for its citizens.

The path to this target requires moving beyond traditional economic sectors such as oil, gas, and agriculture, which alone cannot sustain the country’s growth. Over the past decade, digital transformation has emerged as a critical driver of sustainable economic development, particularly in emerging economies. Nations that effectively leverage digital technologies see more efficient industries, wider access to services, higher productivity, and stronger global competitiveness. For Nigeria, a digital-first economy demands embedding technology across all sectors, including finance, agriculture, healthcare, and education.

Key objectives for this transformation include expanding internet access and digital literacy, promoting tech-driven entrepreneurship, improving e-governance for transparency and service delivery, and investing in infrastructure such as broadband networks, data centres, and connectivity solutions. The National Digital Economy Policy and Strategy (2020–2030) acknowledges these priorities, aiming to establish Nigeria as a globally competitive digital economy while fostering innovation, attracting investment, and creating jobs.

Global and regional context

Nigeria’s ambition positions it alongside other leading African economies such as South Africa, Egypt, and Kenya, which have leveraged digital transformation to diversify and strengthen their growth.

South Africa: With a diversified economy and robust financial services sector, South Africa ranks highly in internet penetration, e-commerce, and fintech innovation. Its technology sector is valued at around $3 billion, contributing 10% of GDP in 2022, illustrating the economic weight of digital adoption.

Egypt: Egypt’s National AI Strategy, launched in 2020, aims to boost GDP by integrating AI across industries, from agriculture to manufacturing. Investment in digital infrastructure has positioned the country as a major tech player in North Africa.

Kenya: Known for M-Pesa and its mobile money revolution, Kenya has become a model of digital innovation in developing economies. Mobile financial services account for about 6% of GDP, supported by proactive policies and partnerships that have raised mobile broadband penetration to 45%.

Nigeria’s approach must adapt these lessons to its unique economic and social landscape. Effective digital integration could propel the country not only toward a $1 trillion GDP but also to renewed leadership in Africa’s technology-driven growth.

Technological infrastructure as the foundation

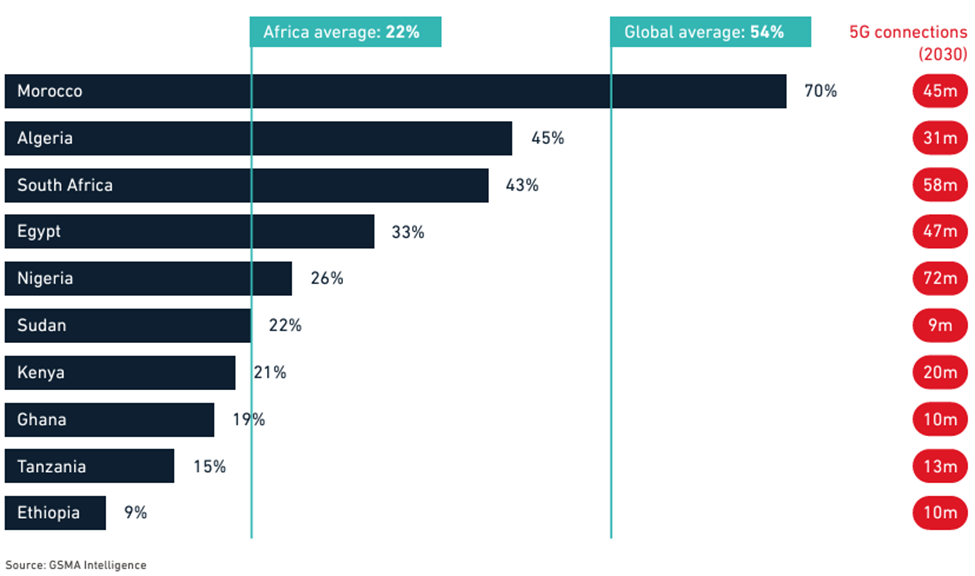

A digital-first economy depends on robust, accessible infrastructure. Expanding 5G networks and broadband is essential to support e-commerce, digital banking, healthcare, and education. Partnerships with telecom companies such as MTN, Airtel, and Globacom have enabled initial 5G rollouts, but adoption remains uneven. Beyond connectivity, 5G offers transformative potential for smart cities, telemedicine, agritech, and educational innovation. Estimates suggest 5G deployment could contribute up to 5% of GDP by 2030.

Fiber optic expansion complements this, providing the backbone for a resilient digital economy. Government programs, such as the National Broadband Plan (2020–2025), aim to increase penetration to 70% by 2025. Private sector investment, including submarine cables like MainOne’s WACS and MTN Nigeria’s fibre initiatives, has strengthened connectivity, yet continued efforts are needed to ensure broad access.

Economic impact of digital integration

Current internet penetration of roughly 40% already shows tangible effects on productivity, entrepreneurship, and service delivery. Studies by the African Development Bank and the World Bank suggest that economies integrating digital technologies grow 2–3 percentage points faster than those relying solely on traditional sectors. For Nigeria, effective fibre network expansion and digital adoption could raise GDP growth from 2–3% to 6–7% annually, with the telecom sector potentially contributing 15% of GDP.

Regional comparisons reinforce this point: Egypt’s tech ecosystem drives 5% annual growth, while South Africa’s infrastructure supports a 4.5% GDP increase. These examples highlight that technological adoption must be accompanied by policy coordination, workforce readiness, and institutional capacity.

Policy, governance, and skills

Digitalisation alone is insufficient. Nigeria must also invest in workforce skills, especially in STEM and digital literacy, to ensure infrastructure translates into productive capacity. Public-private partnerships, coherent policy enforcement, and incentives for tech entrepreneurship are necessary to create an inclusive, digitally-driven economy.

The way forward

To achieve a $1 trillion economy by 2030, Nigeria must adopt a holistic approach: invest in infrastructure, implement policy reforms, develop digital skills, and strengthen institutional governance. Strategic engagement with global technology partners, robust digital training programmes, and expansion of tech entrepreneurship will be central. Without these measures, ambition risks remaining aspirational.

A digital-first economy is not merely a vision; it is a strategic imperative for Nigeria’s growth, global competitiveness, and future prosperity. Execution, not just policy articulation, will determine whether Nigeria can translate its demographic potential and technological opportunity into meaningful economic outcomes.

Engr. Ogochukwu Friday Ikwuogu: (B.Sc., M.Sc.; Registered Engineer, Council for the Regulation of Engineering in Nigeria (COREN); Member, Nigerian Society of Engineers (NSE); Society of Petroleum Engineers (SPE) Senior Member, IEEE)