Global banks accelerate Africa retreat

Standard Chartered moved closer to a full exit from Botswana as it explores the sale of its entire local unit, underscoring a broader pullback by international lenders from smaller African markets.

The London-based bank has already scaled back or exited operations in Zimbabwe, Angola, Cameroon, Gambia, Sierra Leone, Zambia, and Tanzania, joining peers such as Société Générale, BNP Paribas, HSBC, and Atlas Mara in shrinking their African footprints.

Rising compliance costs, weaker returns, and intensifying competition from fintechs and local banks continue to reshape banking economics across the continent.

Why it matters: The withdrawal of global banks is changing Africa’s access to trade finance and dollar liquidity, accelerating the rise of regional champions but leaving gaps in smaller and frontier markets.

Nigeria, South Africa Exit EU–FATF high-risk jurisdictions list

Nigeria, South Africa, Burkina Faso, and Mozambique were removed from the European Union and Financial Action Task Force high-risk jurisdictions lists between October 2025 and January 2026, reflecting progress in anti-money laundering and counter-terrorism financing reforms.

Why it matters: The delistings reduce compliance risks for banks and investors, lower transaction costs, and could support cross-border capital flows and correspondent banking ties across affected African markets.

AGOA extension offers relief—but not clarity

While the US House of Representatives approved a three-year extension of the African Growth and Opportunity Act (AGOA) to 2028, 17 African countries—including Ethiopia, Uganda, and Zimbabwe—remain excluded from the programme. Only 32 countries currently retain duty-free access to the US market, with eligibility subject to annual review by the White House.

The African Union has urged the US Senate to pass the bill swiftly to restore certainty for exporters.

Why it matters: Persistent uncertainty around AGOA eligibility undermines long-term investment planning in export-oriented industries such as apparel, agriculture, and light manufacturing.

Angola taps markets as investors stay selective

Angola secured an additional $500 million after extending a $1 billion debt facility with JPMorgan by three years at an interest rate below 8 percent. Structured through a total return swap using sovereign bonds as collateral, the deal highlights how resource-backed African sovereigns are navigating tighter global financing conditions while trying to preserve debt sustainability.

Why it matters: Angola’s deal shows that capital remains available for African borrowers with scale and commodity backing, even as global investors grow more cautious.

Nigeria’s banking sector heads toward consolidation

With Nigeria’s recapitalisation deadline approaching, mid-tier banks are increasingly turning to mergers as rising interest rates, high inflation, and weak liquidity make standalone capital raising more difficult. While Tier-1 lenders have largely met regulatory thresholds, analysts expect multiple mergers among Tier-2 and Tier-3 banks, despite risks tied to IT integration and corporate culture.

Why it matters: A new wave of consolidation could strengthen Nigeria’s financial system, but poorly executed mergers could disrupt credit flows to businesses and households.

Morocco positions AI as a growth engine

Morocco unveiled plans to generate $10 billion in GDP from artificial intelligence by 2030 through investments in sovereign data centres, cloud infrastructure, fibre networks, and skills development. The government aims to create 50,000 AI-related jobs and train 200,000 graduates, embedding AI across public administration and industry.

Why it matters: Morocco’s strategy highlights a growing shift among African economies toward technology-driven industrial policy as a response to slowing commodity-led growth.

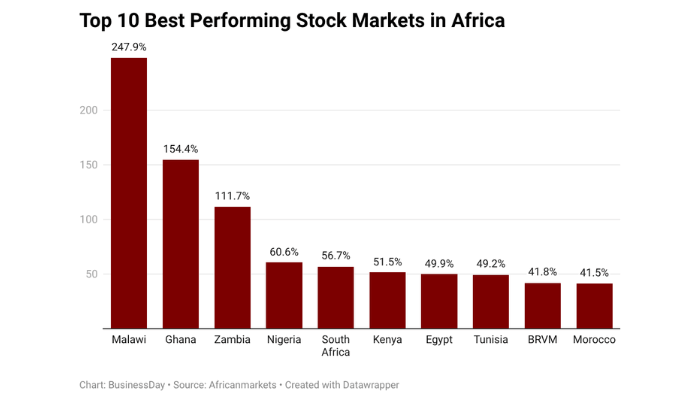

Chart of the day