From Power to Finance: Signals Beyond Otedola

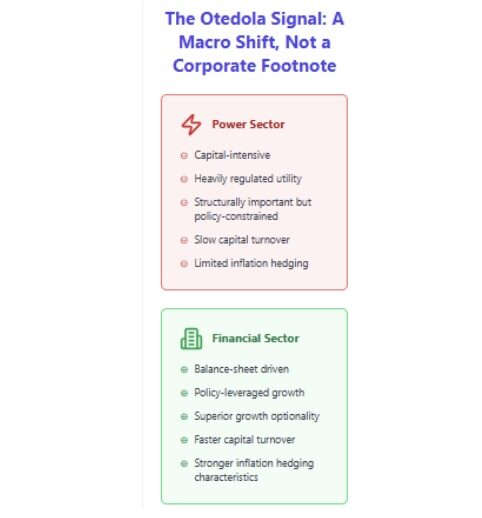

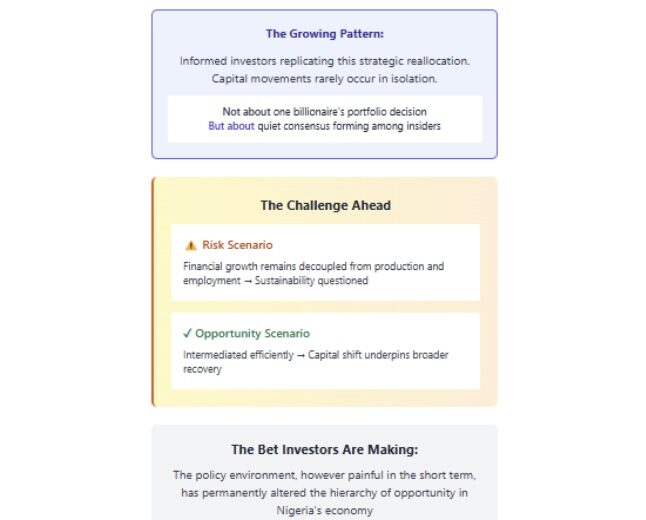

That Femi Otedola divested from Geregu Power to deepen his exposure to FBN Holdings is no longer market gossip; it is settled fact. What now deserves analytical attention is the growing list of investors replicating that strategic reallocation. Capital movements rarely occur in isolation, especially among informed market participants with access to superior data and policy insight. Otedola’s exit from a capital-intensive, regulated utility into a balance-sheet-driven financial conglomerate reflects more than personal preference; it mirrors a changing risk-reward equation in Nigeria’s economy. Power remains structurally important but policy-constrained, while finance has become increasingly policy-leveraged. The new story, therefore, is not about one billionaire’s portfolio decision, but about the quiet consensus forming among insiders that Nigeria’s financial sector now offers superior growth optionality, faster capital turnover, and stronger inflation hedging characteristics than most real-sector alternatives.

GDP Data and the New Growth Engine

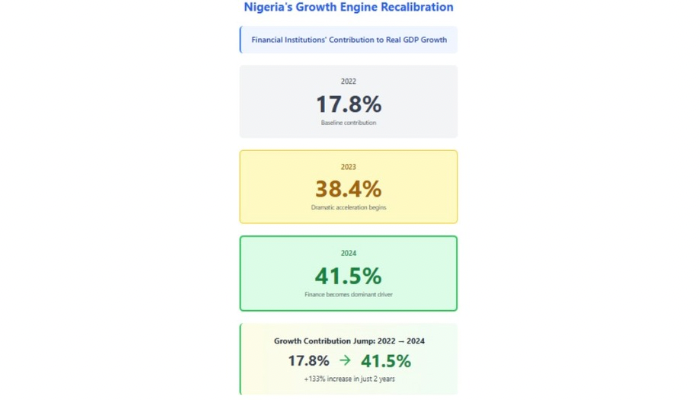

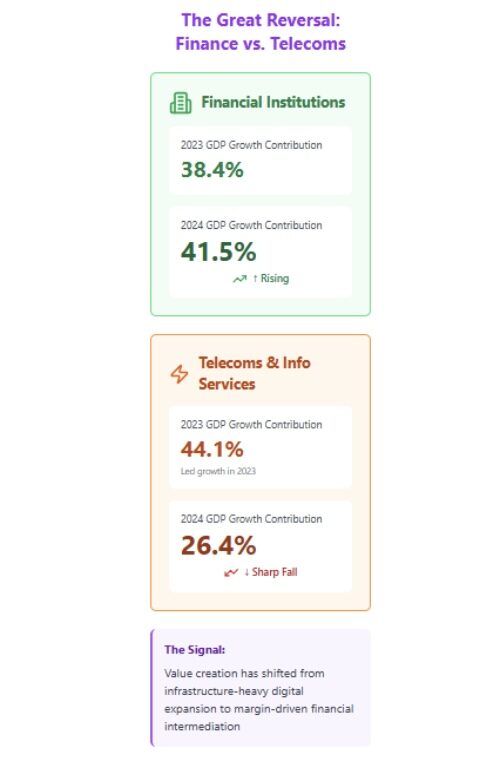

The macroeconomic justification for this capital migration is compelling. National accounts data show that financial institutions, as a standalone sector, contributed 38.4 percent of Nigeria’s real GDP growth in 2023, rising further to 41.5 percent in 2024. This represents a dramatic acceleration from the sector’s 17.8 percent contribution in 2022 and confirms finance as the dominant growth driver in the economy. Telecommunications and information services, which led growth in 2023 with a 44.1 percent contribution, fell sharply to 26.4 percent in 2024. This reversal is significant. It signals that value creation has shifted from infrastructure-heavy digital expansion to margin-driven financial intermediation. In real terms, banks and other financial institutions are now doing more to expand economic output than any other sector, reflecting deeper monetisation of risk, currency volatility, and credit demand.

Insider Trades and Informed Positioning

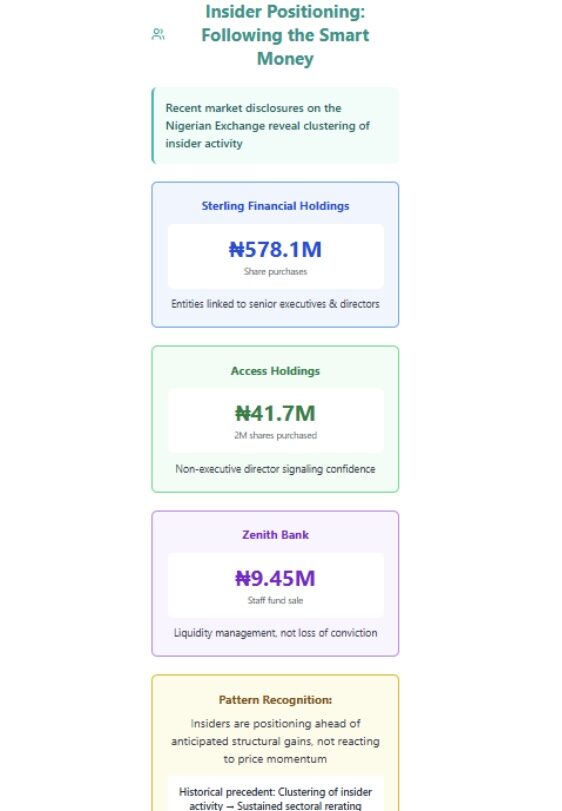

Market disclosures on the Nigerian Exchange reinforce this macro narrative. Entities linked to senior executives and directors of Sterling Financial Holdings recently acquired shares valued at about ₦578.1 million, a move difficult to dismiss as routine portfolio adjustment. At Access Holdings, a non-executive director purchased an additional two million shares worth roughly ₦41.7 million, signalling confidence in medium-term earnings prospects. Even the sale of about ₦9.45 million worth of Zenith Bank shares by a staff provident fund fits within this pattern, reflecting liquidity management rather than loss of conviction. Taken together, these transactions suggest that insiders are not merely reacting to price momentum; they are positioning ahead of anticipated structural gains. Historically, such clustering of insider activity has preceded sustained sectoral rerating rather than short-term speculation.

Policy Liberalisation and Financial Sector Elasticity

The speed of the financial sector’s ascent raises an obvious question: what changed? The timing points directly to the liberalisation agenda of the Tinubu administration, particularly foreign exchange unification and subsidy removal. These reforms have increased nominal balance sheet sizes, widened spreads, and re-priced risk across the system. Unlike manufacturing or power, financial institutions adjust almost instantaneously to macro price changes. Exchange rate liberalisation boosts trading income, revalues foreign assets, and increases naira-denominated earnings, while subsidy removal indirectly raises transaction volumes and financing needs. In effect, policy volatility has become revenue for banks. This explains why finance has responded more forcefully than other sectors to reform. Some investors appear to understand this elasticity better than others and are positioning accordingly, well before the full-cycle benefits are reflected in earnings.

An Economy Recalibrating Its Core

Otedola’s departure from Geregu Power should therefore be read as a macro signal, not a corporate footnote. Nigeria’s economic engine is recalibrating, and capital is following the highest growth transmission channel. For now, that channel is finance. The challenge ahead is ensuring that this dominance translates into real-sector credit expansion rather than balance-sheet deepening alone. If financial growth remains decoupled from production and employment, its sustainability will be questioned. But if intermediated efficiently, today’s capital shift could underpin a broader recovery. The investors buying financial stocks today appear to be betting that the policy environment, however painful in the short term, has permanently altered the hierarchy of opportunity in Nigeria’s economy.