In November 2025, Nigeria returned to the international capital markets with a $2.35 billion Eurobond issuance, one of its largest in recent years. The dual-tranche bond, maturing in 2036 and 2046, was priced at coupons of 8.63% and 9.13% respectively, attracting strong investor demand of over $13 billion.

While the oversubscription reflects confidence in Nigeria’s macroeconomic reforms, the cost of borrowing remains high by global standards — particularly for long-term capital projects. Coupons near 9% translate into substantial interest obligations and add pressure to public finances already constrained by debt servicing costs.

Sovereign Eurobonds are priced to reflect the full spectrum of country risk, including fiscal deficits, currency volatility and macroeconomic uncertainty. As a result, even well-defined infrastructure projects are financed at rates that reflect the sovereign balance sheet rather than the project’s own cash-flow strength.

An alternative approach is structured financing through a Special Purpose Vehicle (SPV) domiciled in established international financial centres such as Guernsey, Jersey or the Cayman Islands. An SPV is a legally ring-fenced entity set up to finance a specific project — such as a toll road, power plant or port — with dedicated revenue streams earmarked for debt repayment.

Under this structure, project revenues are prioritised for debt service, and commodities such as crude oil and natural gas can be used as credit enhancement. This legal isolation reduces investor risk and typically results in lower borrowing costs.

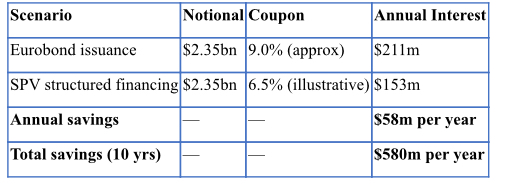

How much could Nigeria have saved?

A back-of-the-envelope comparison illustrates the potential savings:

Over a 10-year horizon, this equates to approximately $580 million in lower interest payments and savings could be higher over longer maturities or with further credit enhancements.

While Nigeria’s recent Eurobond issuance was a market success, sustainable and cost-effective infrastructure financing will increasingly depend on structured solutions that link capital directly to project revenues.

Written by Olu Omidire FCCA FRM

A Guernsey based Macroeconomist, and a USA Licensed Commodity Trading Advisor (CTA) with international experience in offshore financial centres – Guernsey, Luxembourg and the Cayman Islands –info@crvcp.com;