Shares of Nigeria’s big banks are cheaper compared to peers in South Africa and Kenya, albeit investors are willing to pay more than the equity per share of some of these foreign banks on the back of better profitability prospects.

Data tracked by BusinessDay from Bloomberg and Market Investing Database showed that Nigeria top lenders’ rank lower in valuation and profitability indicators, implying that shares of foreign lenders are more expensive than their Nigerian counterparts as investors are pricing in higher return on them.

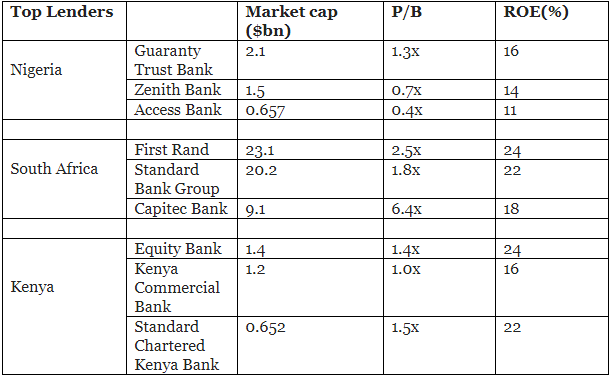

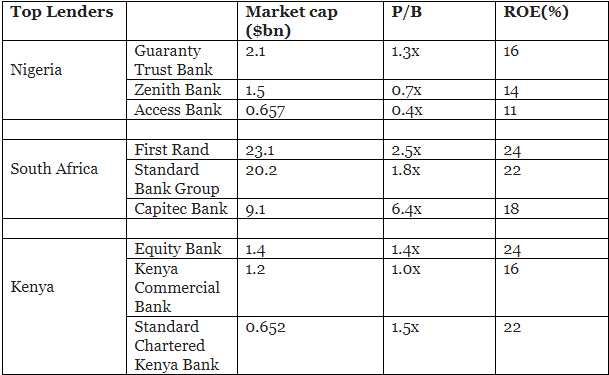

Nigeria’s three most-capitalized lenders – Guaranty Trust Bank ($2.1bn), Zenith Bank ($1.5bn) and Access Bank ($657.4m) are trading 1.3x, 0.7x and 0.4x price-to-book value respectively, indicating that these stocks are under-priced, but remain fundamentally sound with significant potentials for value appreciation.

This compares with South Africa’s top three lenders –First Rand ($23.1bn), Standard Bank ($20.2bn) and Capitec Bank ($9.1bn) trading 2.5x, 1.8x and 6.4x for each local currency unit of their net assets.

Similar trend applies for Kenya’s top lenders – Equity Bank ($1.4bn) and Kenya Commercial Bank ($1.2bn) and Standard Chartered Bank Kenya ($652.3m) trading 1.4x, 1.0x and 1.5x for each local currency unit per net assets.

“From enterprise value perspective, other banks especially South African lenders have huge capital base in excess of billion dollars,” said Taiwo Ologbon-Ori, chief research analyst at Lagos-based Cash Craft Capital.

“So these banks cannot have similar valuation with Nigerian banks, and it is expected that shares of these foreign banks will be more expensive and more attractive to investors globally.” he said.

Going by their capacity to generate earnings from shareholder funds, GTB, Zenith and Access currently boast of 16 percent, 14 percent and 11 percent return on equity.

But it’s lower compared to their Kenyan counterparts – KCB (24%), Equity bank (22%) and Standard Chartered Bank (18%) and South Africa’s First Rand (24%), Standard Bank (16%) and Capitec (22%).

Nigerian lenders are confronted with a number of headwinds from sluggish economic growth to uncertainty in the polity environment, which investors fear could drag profitability.

The licensing of telecom companies to start operating in the mobile money space is another blow that could challenge the relevance of banks.

Nigerian lenders are less efficient in utilising assets to generate profit as return on assets of the country’s top-three lenders averaged at 1.9 percent compared with Kenya’s 3.3 percent and South Africa’s 3.9 percent.