Across Africa, financial technology has become a symbol of possibility. From mobile wallets in Kenya to payment gateways in Nigeria, fintech is reshaping how people move money, access credit, and interact with financial services. In Nigeria alone, fintech transactions were projected to reach over $200 billion annually, powered by a young population eager for digital solutions.

But behind the rapid growth lies a crucial question: how reliable are these systems, and how much trust can users place in them?

The answer lies not just in innovation, but in Quality assurance. Behind every seamless digital transaction is an ecosystem that must be tested, validated, and continuously monitored for performance, compliance, and security. Quality assurance ensures that fintech applications meet the highest standards

detecting vulnerabilities, preventing downtime, and protecting sensitive data before issues reach the end user.

In Nigeria’s rapidly expanding fintech landscape where transactions are projected to exceed $200 billion annually QA is no longer a back-end process; it is a strategic necessity. Robust testing frameworks help uncover defects early, safeguard APIs, and ensure compliance with global standards such as PCI-DSS, SOC 2, and ISO 27001.

With consumer trust hinging on system reliability, fintech firms can no longer afford to treat QA as an afterthought.

However, challenges persist. Many startups still prioritize speed to market over testing depth, exposing users to glitches, transaction delays, and occasional data breaches. The push for digital inclusion must therefore be matched by a commitment to testing transparency and regulatory alignment. Continuous testing, independent audits, and public reporting of system reliability metrics are key to building and maintaining trust.

Ultimately, the future of African fintech depends on trust through quality. As the sector matures, those who embed QA and cybersecurity into every stage of their development lifecycle will not only protect users they will define the new standard for reliability in digital finance across the continent.

Why QA is essential in fintech

Unlike other industries, fintech operates in a zero-tolerance environment. A buggy e-commerce app may frustrate customers, but a faulty fintech app risks financial loss. Every transaction carries monetary value, meaning that errors can directly affect livelihoods.

We have already seen how this plays out in Nigeria. During the surge of USSD banking in 2016, millions of users depended on simple codes to transfer money, pay bills, and top up airtime. But with that surge came a rise in transaction reversals and delays, where funds were debited but not credited to the recipient. Banks had to spend weeks investigating, while customers were left stranded. Stronger QA testing of transaction reliability under heavy network congestion could have prevented many of those failures.

Similarly, when Nigeria introduced the Bank Verification Number (BVN) system in 2015, fintechs and banks had to reconfigure their platforms to integrate this national identity layer. QA teams became central to testing the security and accuracy of BVN-linked transactions. Those who invested in thorough testing rolled out seamless integrations. Those who didn’t faced repeated downtime, rejected transactions, and compliance fines.

These examples show that QA is not an abstract concept. It directly determines whether financial innovations succeed or collapse in the eyes of users.

Challenges in the African context

Fintech in Africa faces unique conditions that make QA even more critical. One is infrastructure. Unstable internet connections and inconsistent electricity supply create real-world conditions that QA teams must simulate. An app that performs well on a stable U.S. broadband connection may falter when faced with the fluctuating 3G speeds common in parts of Nigeria. Testing under these constraints ensures resilience.

Another challenge is device diversity. African fintech users access apps on everything from high-end iPhones to low-cost Android devices. Ensuring that apps run seamlessly across this spectrum requires meticulous device testing. I recall one project where an app passed all lab-based tests, but when piloted in the field, it failed repeatedly on lower-end phones. QA teams had to rebuild compatibility testing to ensure inclusivity.

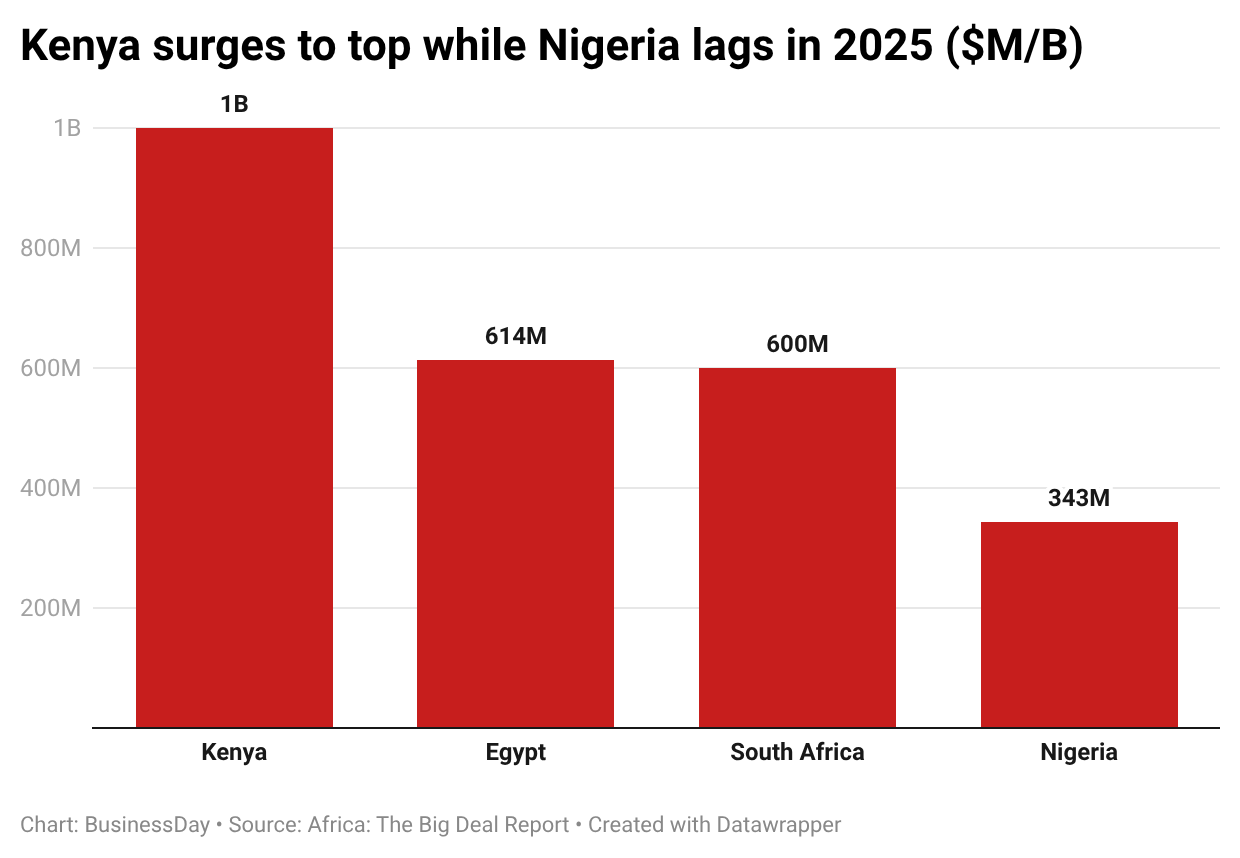

Regulatory requirements add another layer. Nigeria, South Africa, and Kenya all have emerging fintech regulations. QA must confirm not just that systems function technically, but also that they comply with evolving rules on data protection, KYC (Know Your Customer), and anti-money laundering standards. The BVN rollout in Nigeria was an example: those with structured QA processes integrated smoothly, while others stumbled.

Lessons from practice

During my QA work, I saw how fintech firms that prioritized quality outperformed their peers. In one mobile payments project, we established automated regression testing that ran after every code update. This proactive approach caught errors in transaction calculations before they reached customers. In another, we conducted stress tests by simulating peak usage, thousands of concurrent transactions, to ensure that systems would not crash on payday, when usage typically spiked.

One Nigerian bank that invested heavily in QA before launching its mobile app avoided the wave of complaints that hit its competitors during the early adoption period. By contrast, another bank rushed its app to market only to face daily downtime and bad press that took years to recover from. The lesson is clear: in fintech, a delayed but reliable launch is better than a rushed, unstable one.

Building trust in Nigeria and Africa

The future of fintech in Africa depends on trust, and QA is the mechanism that builds it. Startups, eager to launch quickly, must resist the temptation to see QA as a delay. Skipping rigorous testing to meet investor timelines often backfires when systems fail in the hands of users.

Governments and regulators also have a role to play. By introducing and enforcing minimum quality standards for fintech services, they can protect consumers while strengthening the ecosystem. Standards for transaction accuracy, downtime limits, and security compliance should become as familiar as capital adequacy ratios are in traditional banking.

Investors, too, should ask hard questions. Instead of focusing solely on user growth, they should inquire about a startup’s QA process: How do they test across devices? How do they simulate high-volume traffic? What is their recovery plan when transactions fail? These questions, though technical, go straight to the heart of business sustainability.

Recommendations for a resilient ecosystem

From my perspective, three priorities stand out for Nigeria and Africa as they continue to expand fintech. First, investment in testing infrastructure. Fintech firms should establish device labs and network simulators that reflect the realities of their user base. Second, building QA talent pipelines. Universities and training institutions must prepare professionals not only in coding but in the art of testing, governance, and compliance. Third, creating regional QA standards. Just as the African Continental Free Trade Area is harmonizing trade, harmonized fintech QA standards could enable cross-border trust in financial transactions.

The bigger picture

Fintech is often celebrated as a solution to Africa’s financial inclusion gap, but without quality assurance, that promise risks collapse. A failed transaction does not only cost money—it costs trust, and trust is the true currency of financial inclusion.

In my time as a QA Analyst, I came to understand that the unseen work of testing and validation is what makes digital finance possible. From the rollout of BVN to the explosion of USSD banking, QA has been the silent safeguard. As Nigeria and Africa continue their journey toward digital economies, prioritizing QA is not a technical choice—it is a national and continental imperative.